Dividend stocks are the Swiss army knives of the stock market.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

When dividend stocks go up, you make money. When they don’t go up — you still make money (from the dividend). Heck, even when a dividend stock goes down in price, it’s not all bad news, because the dividend yield (the absolute dividend amount, divided by the stock price) gets richer the more the stock falls in price.

Knowing all this, wouldn’t you like to find great dividend stocks? Of course you would.

Wall Street analysts have chimed in – and they are recommending two high-yield dividend stocks for investors looking to find protection for their portfolio. These are stocks with a specific set of clear attributes: a dividend yield of at least 9% and Buy ratings. Let’s take a closer look.

Blackstone Secured Lending (BXSL)

We’ll start with Blackstone Secured Lending, a business development company (BDC) that is under the aegis of the larger Blackstone asset management firm. BXSL operates in the financial services sector, providing capital and credit access to US private companies. BXSL’s portfolio is comprised mainly – nearly 98% – of first lien senior secured loans; most of the remainder is in equity investments. In all, the portfolio was valued at $9.6 billion as of December 31, 2022, and more than 99% of the debt investments are at floating rates.

The general quality of the company’s portfolio can be seen in its 4Q22 financial results. Blackstone Secured Lending showed a net investment income of 90 cents per share, up 13% quarter-over-quarter, and an even stronger 34% year-over-year. The Q4 result came in above the 88-cent forecast and marked the third consecutive quarterly earnings beat in a row.

Dividend investors, however, will be more interested in the company’s February 27 payment declaration. BXSL raised its common share regular dividend by 17%, to a new payment of 70 cents. This was the third quarter in a row that the dividend was increased. The 70-cent div is scheduled to be paid out this coming April 27; at the annualized rate of $2.80, the dividend yields a powerful 11.3%. This is more than 5x the average dividend yield found among S&P-listed companies, and, at 5.3 points higher than inflation.

Among the bulls is Compass Point’s 5-star analyst Casey Alexander, who notes that the company’s strategy is well-adapted to the current interest rate regime, and that it is well-positioned to return capital to shareholders.

“We have made the point that in our view BXSL has the best combination of characteristics for investing in a BDC in the current economic climate. BXSL is among those BDCs where the NII is most leveraged to higher interest rates… we calculate that the BDC generated a 9.5% return based on YE2021 NAV in 2022. Given the volatility of the private debt markets and rapidly changing interest rates, this is an excellent performance,” Alexander opined.

“Also,” the analyst added, “we saw BXSL buy back more than $250M in shares over the course of 2022 and announce an additional $250M share repurchase program. We have always said, in order to earn the right to take capital from the market, you have to be willing to give it back when your stock is trading at a discount, and BXSL filled that requirement in spades.”

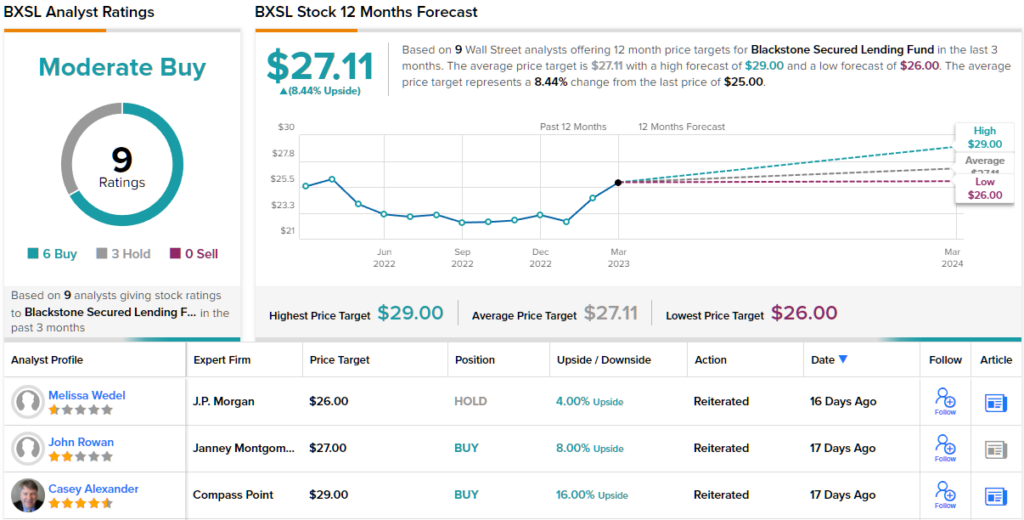

Following from his upbeat commentary, Alexander rates BXSL a Buy, and his $29 price target implies a 16% one-year upside potential for the stock. Based on the current dividend yield and the expected price appreciation, the stock has ~27% potential total return profile. (To watch Alexander’s track record, click here)

Overall, BXSL shares have a Moderate Buy consensus rating from the Wall Street analysts, based on 9 recent analyst reviews that include 6 Buys and 3 Holds. (See BXSL stock forecast)

Westlake Chemical Partners (WLKP)

Next up, Westlake Chemical Partners, is a limited partnership that was formed by Westlake Chemical Corporation in 2014 to operate its ethylene business. The company’s operations include the production and sale of ethylene and co-products such as propylene, butadiene, and hydrogen, which are primarily used in the production of various plastics and other chemical products.

WLKP’s production facilities are located in Calvert City, Kentucky and Lake Charles, Louisiana. In addition to these facilities, the company also operates a 200-mile ethylene pipeline system that connects its production facilities to major markets in the Gulf Coast region, including Houston, Texas. The company has an annual production capacity of 3.7 billion pounds.

The company’s results at the end of last year – 4Q22 – were mixed disappointing. The $3.29 billion in revenue was down 6.3% year-over-year, while missing the consensus estimate of $3.41 billion. Furthermore, the company’s GAAP EPS figure, at $1.79, was down 64% y/y, and missed the consensus estimate of $2.38. The company attributed the lower 4Q22 income in part to higher interest expenses.

Despite lukewarm revenue and income, WLKP has shown a solid increase in cash flow over the past year. Total cash flow from operations in 4Q22 came to $122.6 million, for a highly favorable comparison to the year-ago quarter’s total of $21.9 million. And of particular interest to dividend investors, the 4Q22 distributable cash flow was listed at $20.3 million – up $5 million from the $15.3 million reported in the year-ago period.

The distributable cash flow supports the company’s dividend payment, which was last declared for 47 cents per common share. The payment went out on February 16 of this year. Westlake has held the dividend at this level since the beginning of 2020, and has maintained a reliable quarterly dividend payment going back to 2014. The annualized rate of the current payment, $1.88 per common share, gives a yield of 9%.

This stock has caught the eye of Deutsche Bank’s 5-star analyst David Begleiter, who lays out a case for going bullish here based on the potential for future capital return increases and on current risk mitigation.

“We remain confident that WLKP will continue to offer a distinctive investment opportunity different from other MLPs due to its: i) stable cash flow insulated from commodity price risks; ii) strong balance sheet underpinned by prudent management of cash and leverage metrics; and iii) strategic alignment with its investment grade parent,” Begleiter explained.

To this end, the Deutsche Bank analyst rates WKLP shares a Buy, along with a $28 price target, suggesting an upside of 31% on the one-year time horizon. (To watch Begleiter’s track record, click here)

WKLP appears to be flying under the Street’s radar and currently Deutsche Bank’s is the sole recent review on record. (See WLKP stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.