We’re facing an uncertain market environment. A heavy surge in large-cap tech stocks in Q1 powered a 17% year-to-date gain in the NASDAQ index – but that boost came even despite the persistently high inflation, rising interest rates, and the failure of Silicon Valley Bank. In those circumstances, the tech giants were seen as a ‘fallout shelter,’ offering some protection for investors.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

At least one market expert, however, isn’t following this bullish line. Weighing in from Morgan Stanley, chief investment officer Mike Wilson says, “We see little evidence that a new bull market has begun and believe the bear still has unfinished business… Investors should continue to position portfolios more defensively and focus on companies that exhibit high operational efficiency and high quality of earnings (high cash flow relative to reported earnings and stable accruals).”

A defensive focus, such as Wilson recommends, will naturally lead us into high-yield dividend stocks, the classic defensive play.

Using the TipRanks platform, we’ve looked up two stocks that are offering dividends of at least 10% yield – that’s almost 6x higher the average yield found in the markets today. Each of these is Buy-rated, with some positive analyst reviews on record. Let’s take a closer look.

Pioneer Natural Resources (PXD)

We’ll start with an energy firm, Pioneer Natural Resources. This company is based and operates in Texas, with headquarters in Irving and active hydrocarbon exploration and production operations in the Permian basin oil patch. Pioneer is a pure-play producer in the Permian, focusing all of its active extraction operations in the basin that brought Texas back into the global ranks of top oil and gas producers.

In a unique point of interest to investors, Pioneer offers a fully private route toward oil and gas extraction and royalties. The company’s holdings are entirely on privately owned lands, and Pioneer has avoided drilling or working on federally owned acreage. While the Permian Basin is a large geographical area with plenty of land of both types to go around, by avoiding operations on public lands, Pioneer has also avoided exposure to the current administration’s antipathy toward the fossil fuel economy. While the federal government has reduced permitting for oil companies on public lands, Pioneer remains free to act.

Freedom of action may be an attractive point, but investors should also note that Pioneer is a solidly profitable company. At the bottom line, the company’s non-GAAP EPS in the last reported quarter, 4Q22, came in at $5.91, for a 29% year-over-year gain, while beating the forecast of $5.76.

At the top line, the company’s revenue was $5.17 billion, for an 18% increase year-over-year. We should note that the top line missed the forecast, however – by $490 million.

The company had $1.7 billion in 4Q free cash flow, capping a year that saw FCF hit $8.4 billion. The strong free cash flow helped to support the company’s dividend payment, which bears a closer look.

In its last declaration, Pioneer laid out a base-plus-variable dividend of $5.58 per common share. This was paid out on March 17, and marked the 7th quarter out of the last 8 in which the company has added a significant variable dividend to the base payment. At the current payment of $5.58, the dividend annualizes to $22.32 per common share and yields 10.6%.

These facts lie behind analyst Derrick Whitfield’s optimistic view of the company. In his coverage for Stifel, Whitfield writes: “In our view, PXD offers investors a yield-oriented investment with thematic exposure to our return of capital and M&A themes. The company’s combination of low-cost inventory depth, balance sheet, and shareholder-friendly return of capital strategy is unmatched in our bellwether universe. Qualitatively, PXD… produces a high-quality Permian barrel… and has no federal acreage exposure. Net-net, the stock offers investors a yield-oriented investment proposition with an unmatched depth of low-cost inventory…”

To this end, Whitfield recommends PXD stock as a Buy, with a target price of $293 implying ~39% upside for the coming year. Based on the current dividend yield and the expected price appreciation, the stock has ~50% potential total return profile. (To watch Whitfield’s track record, click here)

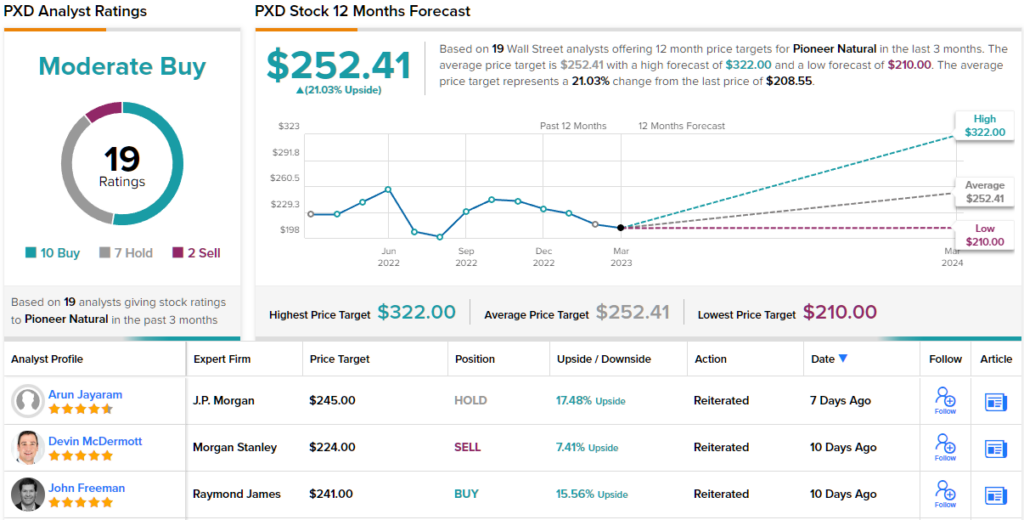

Overall, the analyst consensus rating here is a Moderate Buy, based on 19 reviews that include 10 Buys, 7 Holds, and 2 Sells. Pioneer’s shares are selling for $208.55, and their $252.41 average price target suggests a 21% upside on the one-year horizon. (See PXD stock forecast)

Franklin BSP Realty Trust (FBRT)

The next high-yield dividend stock we’re looking at is Franklin BSP Realty, a real estate investment trust (REIT). This class of companies has long been known as true champs among dividend stocks; they are required by tax code regulations to return a high percentage of profits directly to shareholders, and dividends make a convenient vehicle for compliance. As a result, REIT’s are frequently found among the market’s higher-yielding dividend payers.

Franklin is a typical company in its niche. The firm holds a portfolio focused mainly on commercial real estate; Franklin both originates and acquired commercial real estate debt, which it then underwrites and manages. The company has a wide footprint, and lends against all types of commercial properties, with the aim of generating attractive returns.

We can look at the last quarterly report (4Q22) to put some numbers on those returns. The company’s quarterly revenue in Q4 was $201.65 million, up 25% year-over-year. At the bottom line, Franklin had a non-GAAP quarterly EPS of $1.17, and distributable earnings of 37 cents per diluted share. This last is of considerable importance to dividend investors, as it directly supports the payout. The distributable EPS in Q4 just edged over the 36-cent forecast, and more than covered the last declared dividend of 35.5 cents per common share.

That common share dividend, declared last month and due to go out on April 10, annualizes to $1.42 per share and gives a forward yield of 11.7%.

Covering this stock for Raymond James, 5-star analyst Stephen Laws charts a path forward based on the positive impact of rising interest rates to Franklin’s model. Laws writes: “The loan portfolio is 76% multifamily loans and only 8% office loans, a favorable mix versus sector averages of 39% and 26%, respectively. Portfolio returns are positively correlated to higher interest rates, and we expect 1H earnings to benefit from LIBOR increases YTD… Our estimates assume interest rates peak in 2Q and decline gradually in 2H and 2024. We assume modest near-term portfolio growth, with new investment activity increasing in 2H.”

Adding to this, the analyst gives Franklin stock an Outperform (i.e. Buy) rating, with a $13.50 price target to imply a one-year upside potential of 10%. (To watch Laws’ track record, click here)

“Our Outperform rating reflects the attractive portfolio characteristics, such as high mix of multifamily loans, minimal office exposure, benefits of increasing interest rates, and high mix of non-mark-to market financing, as well as the attractive risk-reward with shares trading at ~70% of book value,” Laws summed up.

So, that’s Raymond James’ view, let’s turn our attention now to rest of the Street: FBRT’s 3 Buys and 1 Hold coalesce into a Strong Buy rating. The average price target is higher than Laws’, at $15.17, and implies a stronger upside potential of 24% from the $12.23 share price. (See FBRT stock forecast)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.