I consider SBA Communications (NASDAQ:SBAC) to be a pinnacle performer in the realm of REITs. Despite the challenges posed by heightened interest rates in the real estate sector, SBA continues to achieve growth in its funds from operations. Managing approximately 48,000 communication towers for telecom giants, the company mitigates most of the risks tied to traditional retail, commercial, or industrial REITs. With shares currently trading at a 40% discount from their 2021 high, I am bullish on the stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Why is SBA Still Trading 40% Below Its High?

Despite overall market indices showing significant recovery, SBA Communications stock continues to trade approximately 40% below its 2021 peak of about $391. This situation arises from the fact that all REITs generally find themselves in a considerably more challenging position today compared to about two years ago. This is because the swift rise in interest rates during this period has had a detrimental impact on the very foundation of their business models.

To delve deeper into this issue, it’s crucial to understand that REITs are obligated to distribute the majority of their taxable income to shareholders in the form of dividends. To support property acquisitions and expansions, REITs frequently turn to debt and equity issuance, as they typically retain minimal income.

However, when interest rates are elevated, the cost of issuing debt rises, constraining a REIT’s capacity to expand through new investments. Simultaneously, the increased interest expenses on existing debt adversely affect current profitability.

SBA Communications mirrors this trend, as evidenced by the company’s total debt ballooning from $5.65 billion to $14.77 billion over the past decade as it pursued its tower portfolio expansion. This should explain why investors remain wary about SBA’s investment case relative to the rest of the rest of the market.

SBA’s Performace Continues to Impress, Nonetheless

As I just highlighted, elevated interest rates impact all REITs, including SBA. Nonetheless, SBA stands out due to its distinctive strategy centered around telecommunication towers, giving it unique attributes that underpin a resilient performance. Unlike residential REITs grappling with soaring mortgages and commercial REITs contending with low occupancy rates, the telecom towers sub-industry demonstrates remarkable durability.

This resilience is attributed to the mission-critical nature of telecommunication towers, which serve as indispensable assets for industry giants like AT&T (NYSE:T), Verizon (NYSE:VZ), and T-Mobile (NASDAQ:TMUS). Thus, telecom giants prioritize meeting their lease obligations to ensure seamless network coverage. This results in a dependable cash flow stream for SBA with comparatively lower risks compared to other REITs specializing in more conventional asset classes.

SBA once again showcased its robust performance in the latest Q3 results, revealing an increase of 8.5% in leasing revenues. This growth can be attributed to an expanded tower portfolio and enhanced leasing activities. In particular, gross same-tower recurring cash leasing revenue experienced a substantial uptick of 8.8%. Domestically, the figures remain impressive, with a gross basis growth of 8.6% and a net basis growth of 4.7%, inclusive of a mere 3.9% churn.

As you can see, even during such a tough macroeconomic environment, SBA’s churn rate is remarkably low, underscoring the resilience of telecom towers. Continual escalations in contractual rent and a steady rise in tenancies per tower consistently surpass any instances of relocations or vacancies. This recurrent industry trend guarantees a sustained increase in leasing revenues.

Of course, grappling with the substantial impact of escalating interest rates, SBA has witnessed a notable deceleration in tower acquisitions and developments. Moreover, the company is paying notably higher interest expenses on its existing debt portfolio, which rose by about 14% year-over-year to reach $99.3 million in Q3.

Despite these challenges, SBA has demonstrated resilience through prudent cost management and impressive top-line performance, enabling the company to maintain robust profitability. Notably, adjusted funds from operations (AFFO) experienced a 7.3% year-over-year increase, totaling $364.1 million. On a per-share basis, AFFO increased by 7.7%, further amplified by strategic share buybacks.

With a robust Q3 performance from SBA, coupled with a strong first half of the year, the company’s management has elevated its FY2023 outlook. SBA is poised for growth, anticipating site leasing revenues between $2.510 billion and $2.520 billion (an increase from the previous range of $2.502 billion to $2.522 billion) and AFFO/share ranging from $12.91 to $13.13 (up from the previous forecast of $12.80 to $13.16).

Significantly, the midpoint of management’s projected guidance, standing at $13.02, hints at a noteworthy year-over-year surge of 6.9%. This figure might not immediately strike as remarkable. However, achieving robust high-single AFFO/share growth in a market where the majority of REITs are grappling with double-digit declines in profits is truly commendable.

Is SBA Stock a Buy, According to Analysts?

Regarding Wall Street’s view on SBA Communications, the stock has gathered a Strong Buy consensus rating based on nine Buys and two Holds assigned in the past three months. At $252.27, the average SBA Communications stock price target implies 7.3% upside potential.

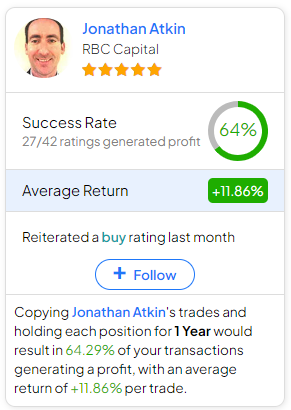

If you’re wondering which analyst you should follow if you want to buy and sell SBA stock, the most profitable analyst covering the stock (on a one-year timeframe) is Jonathan Atkin from RBC Capital, with an average return of 11.86% per rating and a 64% success rate. Click on the image below to learn more.

The Takeaway

SBA Communications emerges as a standout performer in the current challenging landscape for REITs. Despite facing headwinds from elevated interest rates, the company’s unique focus on telecommunication towers sets it apart, ensuring a resilient performance. Its Q3 results verify this theme, with impressive leasing revenue growth and a low churn rate.

While the effects of increasing interest rates found their way into SBA’s income statement, the company’s adept cost management and robust top-line performance have artfully set the stage for another year of record AFFO/share. However, despite outperforming its sector peers, SBA’s stock remains notably lower than its previous highs. This discrepancy suggests that it might be an opportune moment for investors to reevaluate SBA’s bullish case, which, in my perspective, presents a compelling opportunity.