One of the mercurial winners of the post-pandemic new normal, streaming platform provider Roku (NASDAQ:ROKU) once traded for well over $400 on a per-share basis. However, in 2022, the bubble deflated, sending the company gasping for air. To rectify the situation, management announced a company first – building in-house television sets rather than relying on third-party manufacturers. Still, competition and economic risks cloud the narrative for ROKU stock.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

At the technology industry’s biggest tradeshow CES, Roku announced the launch of Roku Select and Roku Plus Series TVs. Per the company’s press release, “[t]hese Roku-branded HD and 4K TVs are the first ever to be both designed and made by Roku, underlining the company’s commitment to delivering a best-in-class streaming experience at an accessible price.”

Along with a newly developed Roku TV Wireless Soundbar, these products will be available in the U.S. this spring. In addition, the streaming platform specialist announced a new OLED TV reference design for third-party partners. Here, the ambition centers on delivering OLED attributes – such as color vibrancy – to a broader audience. In theory, these fresh developments should bolster ROKU stock.

After all, the point of bringing production elements in-house is profitability. With fewer partners involved (at least for the Select and Plus Series), Roku can accrue greater rewards from sales. However, with fewer partners comes less space to which to distribute risk, and that’s one of the main concerns for ROKU stock.

It’s not possible to cherry-pick the rewards of a strategic decision without accepting the potential risks. Moving forward, investors should be cautious about ROKU stock and the possibility of a bull trap.

ROKU Stock Faces Two Serious Headwinds

To be sure, no one should disrespect the incredible momentum that ROKU stock generated recently. In the business week that ended Jan. 6, shares gained 10.35%. That’s well above the nearly 2% that the benchmark equities index posted during the same period. Nevertheless, longer term, it’s difficult to gloss over Roku’s fundamental risks.

First and foremost, the company’s dilemma does not necessarily center on its Player business unit, which focuses on streaming players and audio products. In the third quarter of 2022, Player revenue only accounted for 12% of total net revenue. Rather, 88% of revenue stems from the company’s Platform unit. This involves, in large part, the sale of digital advertising and related services.

Here’s the problem for ROKU stock: digital advertising revenue cratered in 2022. Further, this crisis doesn’t just impact one particular technology firm but the whole industry.

To be fair, Roku intends to mitigate the pain by boosting revenue from its Player segment with in-house TVs. However, the challenge here centers on competition. Though possible, it’s difficult to imagine how Roku – as the new kid on the block – will disrupt deeply entrenched competitors.

Another headwind for ROKU stock comes from the consumer economy. After enjoying the bounty of government stimulus checks, American consumers woke up to a harsh reality check. A few months ago, total household debt grew to a record $16.5 trillion. At a time when layoffs have become a growing concern, spending money on TVs isn’t exactly smart.

In this context, it’s even more difficult to imagine hard-hit consumers buying OLED TVs, which are way more expensive than “regular” TVs.

Is ROKU Stock a Buy?

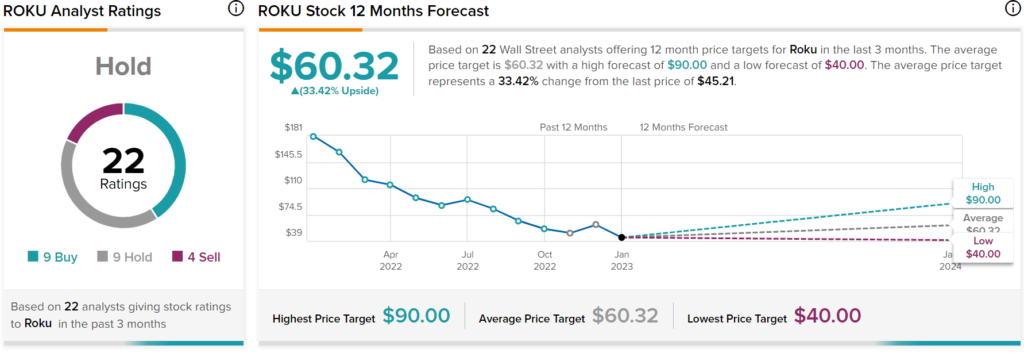

Turning to Wall Street, ROKU stock has a Hold consensus rating based on nine Buys, nine Holds, and four Sells assigned in the past three months. The average ROKU price target is $60.32, implying 33.42% upside potential.

Roku Might be a Value Trap

Following a staggering loss of 76% of equity value in the trailing year, it’s easy to appreciate the speculative appeal of ROKU stock. As well, the underlying financials appear legitimately enticing. However, these signs may instead point to a value trap rather than a true upside opportunity.

For instance, Roku’s three-year revenue growth rate (on a per-share basis) stands at 40.1%. This stat beats out nearly 95% of competitors in the diversified media industry. As well, the market prices ROKU stock at 1.93 times sales, which might seem cheap on paper.

However, moving forward, it’s not clear whether Roku’s prior upside catalysts will be in play in 2023 and beyond. Obviously, ROKU stock benefitted from the COVID-19 pandemic, which temporarily forced people to shelter in place. Recently, though, COVID fears faded, and they might not resuscitate. As well, questionable economic conditions mean consumers aren’t gung-ho about buying TVs.

Understandably, management had to do something. From this angle, the move to build in-house TVs is respectable. Sadly, the TV-manufacturing market may not be the viable solution ROKU stock needs.