With a new year right around the corner, just over a month away, analysts and investors alike are pulling out the crystal balls and tarot cards, reading the tea leaves, and trying to pull back the curtain on tomorrow – all to get an idea of just where the markets are going.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Some seek insights from major investment banks like RBC, one of Canada’s largest financial firms. And RBC, in a recent research note, is seeing room for the bulls to run in the coming year.

The bank’s analysts are predicting that the S&P 500 index will hit 5,000 before the end of 2024, a gain of ~10% from current levels and ~5% above the previous record reach in January 2022. Hitting that record will certainly give investor sentiment a boost.

“While the November rally has likely pulled forward some of 2024’s gains, we remain constructive on the S&P 500 in the year ahead,” the RBC team wrote and went on to point out that the S&P index typically gains 7.5% in a Presidential election year – lower than average, but in the ballpark for the firm’s prediction.

So let’s give RBC’s future-telling a run and take a closer look at some of the firm’s stock picks. The RBC analysts have been busy and have found some stocks likely to play the bounce in a bullish year. Here are the details on 2 of them, drawn from the TipRanks platform.

Don’t miss

- TipRanks’ ‘Perfect 10’ List: These 3 Top-Rated Stocks Hit All the Right Marks

- Buy these 2 solar stocks, analyst says, forecasting at least 90% upside potential

- ‘Time to Upgrade,’ Says Oppenheimer About These 2 AI Stocks

Brookdale Senior Living (BKD)

The first RBC pick is a major operator of senior housing facilities across the US. Brookdale, headquartered in Tennessee, operates a chain of assisted living centers, continuing care retirement centers, dementia-care facilities, and independent living housing facilities, all aimed at senior citizens. The company is a national leader in its niche and provides its residents with care, connections, and services in an environment where they can feel at home.

Brookdale manages its properties through its combined expertise in multiple related fields, including healthcare, hospitality, and real estate. The company has more than 670 communities in its network, located across 41 states.

Shares in Brookdale have strongly outperformed over the past year, and in 2023, the stock is up an impressive 91% year-to-date. Some of these gains can be attributed to the company’s latest 3Q22 report.

In that quarter, Brookdale’s top line reached $757.3 million, surpassing estimates by $4.2 million. The company reported a bottom-line EPS loss of 22 cents per share. This loss was deeper than the 15-cent loss reported in the year-ago period and fell a penny below the forecasted 21-cent loss. The company published RevPAR (revenue per available unit) growth of 9.5% to 10% for Q4, offering an optimistic outlook that suggests a path toward pre-pandemic profitability.

The biggest story, however, does not get reflected in the quarterly numbers – and that is national demographic numbers. The US population is aging, as the birthrate has fallen well below the replacement rate. While this is a controversial topic, the aging population does present a potential ‘boom time’ for Brookdale.

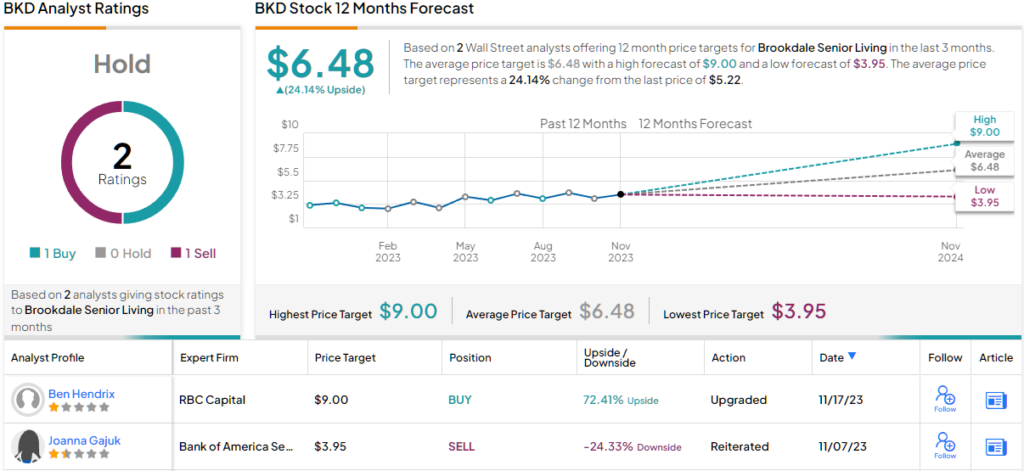

That’s the thesis behind RBC’s Ben Hendrix, who rates BKD stock an Outperform (i.e. Buy) rating, with a $9 price target to suggest a 72% gain in the next 12 months. (To watch Hendrix’s track record, click here)

Backing his bullish stance, Hendrix wrote, “We believe BKD is well positioned to outperform over the next few years given several favorable dynamics. Demand should continue to grow given the aging US population as the US Census Bureau estimates that the number of seniors will increase by over 1 million each year through 2030, with BKD’s age 75+ target population expected to increase by 58% over the next five years to 4.1MM. Meanwhile, strong home values and household income within BKD’s core markets should help ease transition to senior living and provide a competitive advantage. Senior housing construction starts are 52% off peak levels seen prepandemic amid high construction and capital costs, which should support a favorable supply/demand dynamics over the next several years.”

BKD has slipped under the radar a bit and only has 2 recent analyst reviews: 1 to Buy and 1 to Sell, resulting in a Hold consensus rating. The shares are currently trading at $5.22, and the $6.48 average price target implies a 24% one-year upside potential. (See BKD stock forecast)

GoDaddy (GDDY)

The second RBC stock pick we’ll look at is the popular web domain and hosting company GoDaddy. This firm, based in Tempe, Arizona, works in web hosting, domain registration, and as a domain registrar, and is one of the top 5 such web host companies by market share. The company boasts more than 21 million customers who trust it with over 84 million registered domains.

GoDaddy’s service allows customers to build their own website, create and register a domain name, create personalized email addresses, and secure data on or collected by their sites. The company’s customers can buy the standard .com or .co domain names, or even pay extra for boutique domains such as .ai.

GoDaddy has recently introduced a suite of website building tools designed to let website builders and managers automate or streamline the creative process of several vital site functions. The tools are targeted at small business owners and entrepreneurs.

Shares in GoDaddy showed fairly stable trading through most of this year but began to take off in November – realizing an increase of 29% since November 1 and now showing a 27% year-to-date net gain. The surge in the shares was supported by a 3Q beat that caught Wall Street’s attention.

Looking at the Q3 report, we see the firm had $1.07 billion in total revenue, surpassing the forecast by nearly $10 million. GoDaddy’s bottom line reached 89 cents per share, a strong gain from the 63 cents reported in 3Q22 and 17 cents per share better than the Street had predicted.

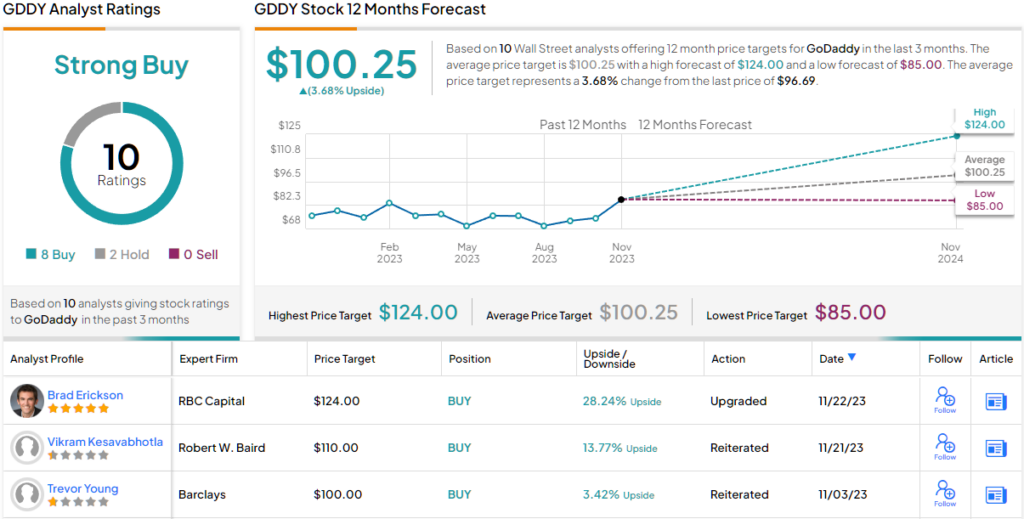

What this means for RBC is simple: GoDaddy is a stock to buy. Analyst Brad Erickson, rated 5-stars by TipRanks, is particularly impressed by the company’s ability to gain new customers – and he points out the customer funnel in his recent note on the shares, writing: “While 2023 web design industry top-of-funnel trends have somewhat underperformed our expectations due to persistent churn post COVID, looking forward, given the state of macro uncertainty, we like GDDY’s uniquely hedged customer acquisition channel where it harvests from the 84M domains and could also gain outsized benefit as AI tools reduce customer acquisition friction. While ratings across our coverage assume a stable macro, there are very few companies in our universe that could actually hit ’24 estimates under incremental macro duress – we believe GDDY would be one.”

Erickson’s Outperform (i.e. Buy) rating on GDDY comes along with a $124 price target that points toward a 28% upside potential for the year ahead. (To watch Erickson’s track record, click here)

Overall, GoDaddy has attracted 10 recent Wall Street analyst reviews, with an 8 to 2 breakdown favoring Buy over Hold to support a Strong Buy consensus rating. The shares are currently priced at $96.69 and their $100.25 average price target suggests a modest one-year increase of ~4%. (See GoDaddy’s stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.