The headwinds have piled up for the US economy, and today’s producer price index, coming in well above the forecasts, was just the latest blow. As the PPI reminds us, inflation is stubbornly high, and compounding on last year’s elevated numbers. In addition, we’re facing a 1H GDP contraction, a nosedive in consumer confidence, shaky supplies chains, and the Federal Reserve’s rapid shift to hiking interest rates.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

And all of that may just be the tip of the iceberg. Billionaire investor Ray Dalio sees a ‘perfect storm’ of challenges that are barreling toward a head-on collision with the US economy. In his view, the unprecedented cash and debt on American books, the irreconcilable political conflicts between the Democratic and Republican parties, and the ongoing Russian war against Ukraine are the chief reasons for concern.

As Dalio also notes, the Federal Reserve’s only tool to fight this downward pressure, especially the high inflation, is to raise interest rates – and that’s a blunt-force object that’s going to cause serious pain. In Dalio’s words, “They will raise interest rates to the point that there’s enough economic pain and financial market pain to deal with that. They’re putting on the brakes, so we’re going to create a giant lurch backward.”

In conditions like these, investors will naturally turn toward defensive stocks, and high-yield dividend payers are the classic defensive play – with the added benefit that a high enough dividend yield can help to offset inflation losses.

With this in mind, we’ve used the TipRanks database to pinpoint two stocks that are showing high dividend yields, on the order of 8% or better. That’s more than enough, on its own, to assure a positive real rate of return, but each of these stocks also brings a double-digit upside potential to the table. Let’s take a closer look.

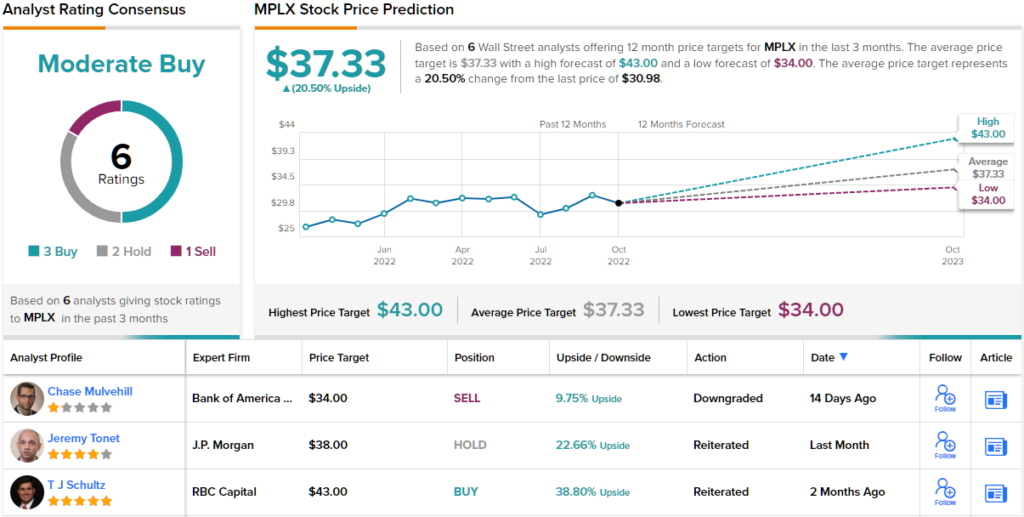

MPLX LP (MPLX)

We’ll start with one of North America’s largest midstream firms, MPLX. This company got its start as a spin-off from Marathon Petroleum, taking the parent company’s midstream transport assets public as a separate entity. Today, MPLX boasts a wide range of transport, terminal, and storage assets, including crude oil and light product pipelines, an inland marine business dedicated to shipping on North America’s great navigable rivers, marine terminals on the coast for the export of both crude oil and light refined products, refiners, tank farms, and other storage facilities, as well as docks, loading racks, and associated transfer piping equipment. MPLX also owns and operates gathering systems and transfer pipelines for crude oil, natural gas, and natural gas liquids.

All in all, MPLX is a midstream giant, with a market cap exceeding $30 billion and total revenues last year of $9.7 billion. The company is on track this year to beat that total, as 1H22 revenues were up 20% from 1H21. The most recent quarter reported, 2Q22, showed a top line of $2.94 billion, up 26% year-over-year. Given this revenue performance, it should come as no surprise that MPLX shares are up 12% so far this year, as opposed to the 25% loss on the S&P 500.

Earnings also have been rising steadily over the past couple of years. Diluted EPS came in at 83 cents in Q2, well above the 66 cents reported in 1Q21. The company also generated $1.5 billion in cash from operations during the quarter, of which $1.23 billion was classed as distributable cash flow.

That last metric supports the company’s dividend, which was last paid out in August at a rate of $0.705 per common share. This dividend annualizes to $2.82 per common share, and yields a robust 9.1%, more than 4x the average yield found among S&P-listed firms. MPLX has kept up a reliable dividend payment since it entered the public markets in 2012. Q2’s dividend declaration was part of a major commitment to returning capital to shareholders; in line with that, MPLX returned $750 million to shareholders in Q2, through both dividends and share repurchases, and in August announce a $1 billion incremental increase to the share repurchase authorization.

All of these factors caught the attention of RBC Capital’s 5-star analyst TJ Schultz, who wrote, “We continue to like MPLX for its steady cash flow stream given its relationship supporting MPC, growth projects in the pipeline, and commitment to capital returns with a new $1B unit repurchase authorization as well as its steady (and likely growing) distribution.”

Schultz goes on to give MPLX shares an Outperform (i.e. Buy) rating, and a price target of $43 to suggest ~39% upside for the coming year. Based on the current dividend yield and the expected price appreciation, the stock has ~48% potential total return profile. (To watch Schultz’s track record, click here)

What does the rest of the Street think? Looking at the consensus breakdown, opinions from other analysts are more spread out. 3 Buys, 2 Holds and 1 Sell add up to a Moderate Buy consensus. In addition, the $37.33 average price target indicates ~20% upside potential from current levels. (See MPLX stock forecast on TipRanks)

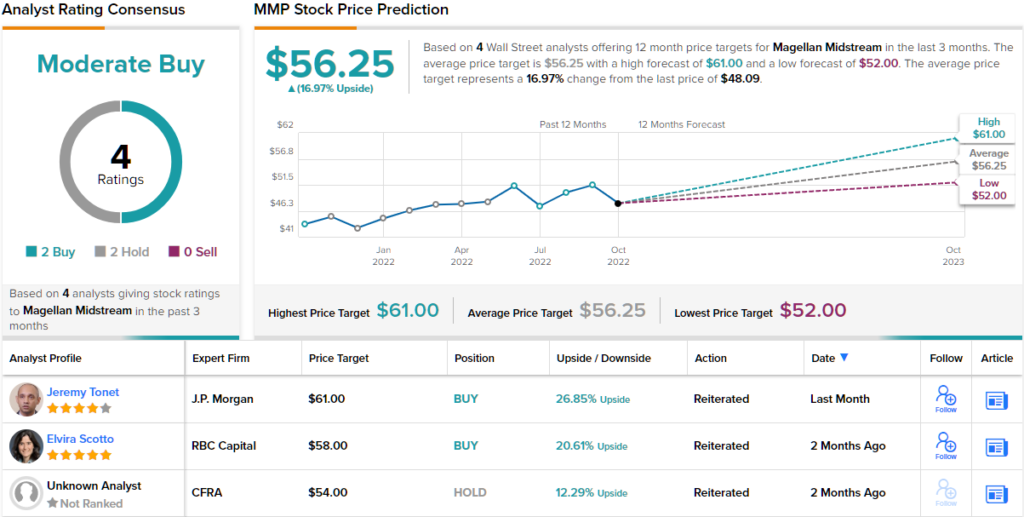

Magellan Midstream (MMP)

Let’s stick with the energy midstream sector, and look at Magellan, another midstream company working in North America. Magellan has a network of assets, including 12,000 miles of pipelines stretching from the Great Lakes and Rocky Mountains to the Mississippi Valley and thence down to Texas and the Gulf Coast. Magellan works with both refined products and crude oil, and its network includes storage facilities and tank farms, and marine terminals on the Gulf of Mexico.

All of this adds up to big business, and Magellan Midstream reported $2.9 billion in 2021 revenues. Looking at the first half of 2022, the company has already seen $1.67 billion, more than half of the previous year’s total. Zooming in a bit further, the 2Q22 report showed a top line of $877.6 million, for a 26% year-over-year increase. The company’s net income also surged in Q2, jumping 26% and reaching $354 million.

That net income translated into a diluted EPS of $1.67, comparing favorably to the $1.26 reported in the year-ago quarter. Magellan also reported substantial cash flows during Q2, with $228 million in distributable cash flow and $649 million in free cash flow for the quarter. The first of those was down 14% y/y, while the second was up 28%. Magellan boasted that it was able to deploy $190 million in its share buyback program during Q2. For investors, we should note that MMP stock has gained about 9% year-to-date.

The company also declared a Q2 dividend, in July, of $1.0375 per common share. This payment gives an annualized common share dividend of $4.15, which in turn makes the yield 8.6%, or just enough to beat August’s inflation numbers.

Wall Street analyst Eduardo Seda covers this stock for Jones Research, and he notes how MMP has successfully expanded its business, increased revenues, and supported its share price in a difficult environment.

“Despite the global GDP growth continuing to moderate more than expected, MMP’s operating results continue to improve across its two operating segments… Overall performance benefitted from higher transportation volumes (up 2.9% to 142.9 million barrels shipped from 138.9 million barrels shipped in 2Q21, and up 8.9% from 131.2 million barrels shipped in 1Q22), driven by continued demand recovery from pandemic levels, additional contributions from MMP’s Texas pipeline expansion projects, and higher shipments on MMPs South Texas pipeline segment,” Seda wrote.

To this end, Seda rates MMP shares a Buy, with a $64 price target that indicates a 33% one-year upside potential. (To watch Seda’s track record, click here)

Turning now to the rest of the Street, opinions are split evenly down the middle. 2 Buys and 2 Holds assigned in the last three months add up to a Moderate Buy analyst consensus. The shares are selling for $48.09 and their $56.25 average price target suggests ~17% upside on the one-year horizon. (See MMP stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.