The Russian war on Ukraine has sparked a slew of sanctions as the Western powers seek to convince Russia to desist – and counter-sanctions, as Russia seeks to push back against the West. Russia and NATO both are reluctant to shoot at each other. But Russia has a powerful sanction weapon to fall back on, to support its war policy.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Germany, and much of Western Europe, imports most of its natural gas from Russia – and the Russian government is turning off that tap. Russian gas exports on the chief pipeline are already down to 40%, and the Russian government will be dropping it further to 20%. Ironically, Western sanctions on Russia are contributing to the cutback, as they have made it more difficult for Russia to maintain and service the pipeline.

The immediate result of this sanctions battle over gas is a surge in natural gas prices – globally. Against this backdrop, we’ve used the TipRanks database to locate two natural gas stocks that are poised to ride those price increases straight to share gains. Both are Strong Buy options, and according to Wall Street’s 5-star analysts, each has considerable upside potential. Let’s take a closer look.

ConocoPhillips (COP)

The first stock we’ll look at, ConocoPhillips, is one of the biggest names in the energy sector. This $116 billion company operates in 13 countries, employs more than 9,400 people, and last year produced more than 1.5 million barrels of oil equivalent every day, leading to annual revenues of $46 billion. This year, the company is continuing to show high revenues and earnings, and is shifting its focus more toward natural gas.

On the matter of natural gas, in June, ConocoPhillips announced that it had won a stake – totaling 12.5% – in the North Field LNG expansion by QatarEnergy. The move makes ConocoPhillips the third partner in the project, and gives the company a foot in Qatar’s natural gas production, which is being ramped up as a potential substitute for Russian fuel exports to Europe.

And earlier this month, ConocoPhillips followed that announcement with the news that it had signed an HOA with Sempra Infrastructure, which will allow for expansion of COP’s liquified natural gas (LNG) business. The agreement involves large-scale investment in new LNG facilities through a multi-phase project.

Turning to financials, ConocoPhillips reported a net income in the first quarter of this year of $5.76 billion, or $3.27 per share in adjusted terms. This marked a dramatic increase from the 69-cent EPS reported in the year ago quarter. At the top line, the company brought in over $18 billion in revenue, up 79% year-over-year.

Of interest to defensive investors, COP also announced in its Q1 financial release that it will be increasing its capital returns to shareholders this year, with a target total of $10 billion for 2022. This will include both share repurchases and common stock dividend payments. ConocoPhillips has plenty of cash available to makes these returns, having reported $7 billion in first quarter cash from operations.

Covering ConocoPhillips for Piper Sandler, 5-star analyst Ryan Todd sees the new gas projects as the key to this stock going forward. Listing several of the company’s natural gas initiatives, Todd writes, “ConocoPhillips has signaled a shift towards a more proactive stance on global gas opportunities. Given the structural changes in global gas markets in the aftermath of Russia’s invasion of Ukraine, and COP’s focus on efficient, low cost-of-supply assets, we view the addition of low-decline, FCF-generating assets as a perfect fit in COP’s long-term portfolio, while the required capital should have limited impact on the company’s FCF outlook over the next five years.”

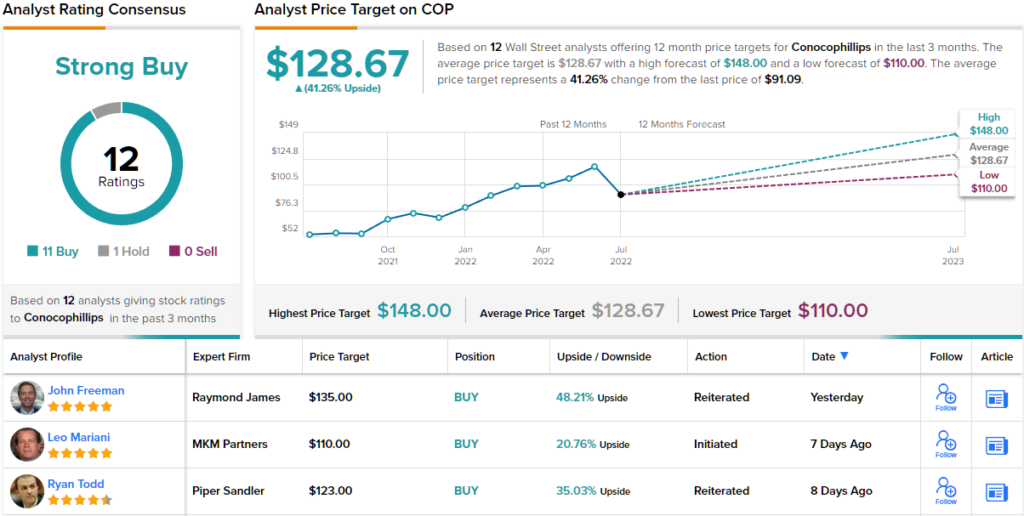

In line with these comments, Todd rates ConocoPhillips shares an Overweight (i.e. Buy), and his price target, set at $123, suggests a one-year gain of 35%. (To watch Todd’s track record, click here)

The market’s giant corporations have always picked up plenty of Wall Street attention, and ConocoPhillips, with 12 recent analyst reviews on record, is no exception. These reviews break down 11 to 1 in favor of the Buys over the Hold, and support the Strong Buy consensus rating on the stock. The shares are trading for $91.09 and their $128.67 average price target implies a one-year upside potential of 41%. (See COP stock forecast on TipRanks)

Chesapeake Energy (CHK)

Based in Oklahoma, with easy access to the Texas oil patch, Chesapeake Energy is an $11.7 billion hydrocarbon explorer and developer with assets in some of the richest production areas of Texas, Louisiana, and Pennsylvania. The company’s leases cover some 1.6 million acres, primarily in natural gas plays.

While Chesapeake Energy doesn’t bring in the high revenue levels of the larger companies, it has brought solid cash flows from its operations. In 1Q22, the most recent reported, CHK reported an adjusted net income of $436 million, or $3.09 per share, which was up 14% year-over-year. The company’s cash flow generated net cash of $853 million, of which $532 million was free cash flow. This FCF was a quarterly record for Chesapeake.

The solid earnings and cash flow supported a strong dividend, a boon for investors. Chesapeake declared a Q1 payment of 50 cents per common share, plus a variable dividend of $1.84, making the total payment $2.34. The regular dividend alone gives a yield of 2.1%, which is in line with market averages; with the variable added in, the div payment yielded 4.1%.

These financials were in their turn supported by solid production and rising gas prices. Chesapeake drills in rich oil and gas plays, but natural gas is the company’s main product. Q1 saw a net production rate of ~620,000 barrels of oil equivalent per day, with 87% of this total being natural gas. The remainder was composed of both gas liquids and crude oil. The company developed this production from 13 rigs operating 41 active wells on its leased acres.

In his coverage of Chesapeake, Wells Fargo’s 5-star analyst Nitin Kumar writes: “CHK has meaningfully underperformed gassy peers YTD, up ~18% vs gas group up ~42%, despite a peer leading cash return framework. We favor CHK’s strong balance sheet, deep drilling inventory, and proximity to Gulf Coast LNG export corridor, which should continue to drive peer leading sustainable FCF yields in the gas sector.”

Kumar adds an Overweight (i.e. Buy) rating to his commentary, and completes his stance with a $130 price target, indicating his confidence in an upside of 41% for the next 12 months. (To watch Kumar’s track record, click here)

Overall, CHK has attracted the eyes of Wall Street’s stock pros – 7 so far have reviewed CHK shares, giving it 6 buys and 1 Hold for a Strong Buy consensus rating. The stock’s $120.29 average price target and $92.19 trading price combine to imply ~30% one-year upside potential to the shares. (See CHK stock forecast on TipRanks)

To find good ideas for energy stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.