Stock market investors want returns, which naturally draws them to the realm of global capital markets. These are drivers of the economic engine, the banks and other financial services companies that provide entrepreneurs and businesses of all stripes with access to the capital and credit that supports their own activities.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Within this sector, the private market firms stand out, and for good reason. They have a history of delivering solid risk-adjusted returns to their own investors, and they typically take a long-term approach to their own investing activities. The combination creates a segment within the financial services industry that offers potential investors the unbeatable combination of stability and a steady income stream.

Nicholas Watts, of Redburn Atlantic, has cast his eye on the opportunities in the private market segment, and writes of the macro-picture, “We expect private markets to remain the highest-growth segment of global financial services, benefiting from a range of ongoing (e.g. companies remaining private for longer) and emerging (e.g. fixed income replacement) trends. The industry’s scale players are benefiting from: (1) institutions consolidating their supplier relationships; (2) brand recognition and the resources to support growth in the largely untapped wealth channel; and (3) investment capacity to seed product and asset class expansion.”

Getting down to the brass tacks, Watts goes on to recommend two alternative asset stocks for investors to consider. We’ve used the TipRanks platform to look up the broader Wall Street view on Watts’ picks. Here are the details, and Watts’ comments.

Carlyle Group (CG)

Realtors will tell you that everything boils down to ‘location, location, location,’ but the Carlyle Group, today’s first stock, already knows this. Based in Washington, DC, on Pennsylvania Avenue just a short walk from the Treasury Building and the White House, this firm specializes in providing private equity, alternative asset management, and other financial services. The company had $435 billion in assets under management as of June 30 this year and had its hands in 606 investment vehicles. The firm’s location in Washington serves it in good stead, as it operates globally; Carlyle Group has 29 offices on four continents and employs some 2,200 professionals to serve its customers.

The company’s operations are split among three main business segments: global investment solutions, global credit, and global private equity. The first of these is the smallest, with $80 billion in AUM; the second, global credit, is the largest, with $190 billion in AUM, based on relationships with some 1,000 borrower entities. Finally, the company’s global private equity segment has $164 billion in AUM and is managed out of 20 offices around the world that oversee more than 285 active portfolio investments.

That all said, Carlyle’s latest quarterly earnings, covering 2Q24, were a bit of a disappointment. Distributable earnings, which indicate the amount of cash available to be returned to shareholders, fell to $343 million from $389 million the previous year. That resulted in after-tax distributable earnings of 78 cents per share, a figure which missed the forecast by 5 cents per share. There were, however, some bright spots elsewhere, including a strong gain in the company’s global credit business. AUM in that segment was up 25% from the prior year.

For Watts, initiating coverage of CG for Redburn, the strong credit growth and recent internal changes deserve a closer look, and he writes of the company, “The company has seen strong growth in its Credit business, which achieved a c18% CAGR from 2013 to 2023. Following a template used by other US private market names, Carlyle has made material changes to its compensation structure, shifting a greater proportion of FRE towards shareholders and giving employees a greater proportion of performance-related earnings.”

Recommending the stock to investors, Watts, adds, “We are mindful of certain pressures around the business, especially the need to improve investment performance in the core PE business. However, the valuation appeal of Carlyle is powerful and we acknowledge the groundwork being done for future improvement.”

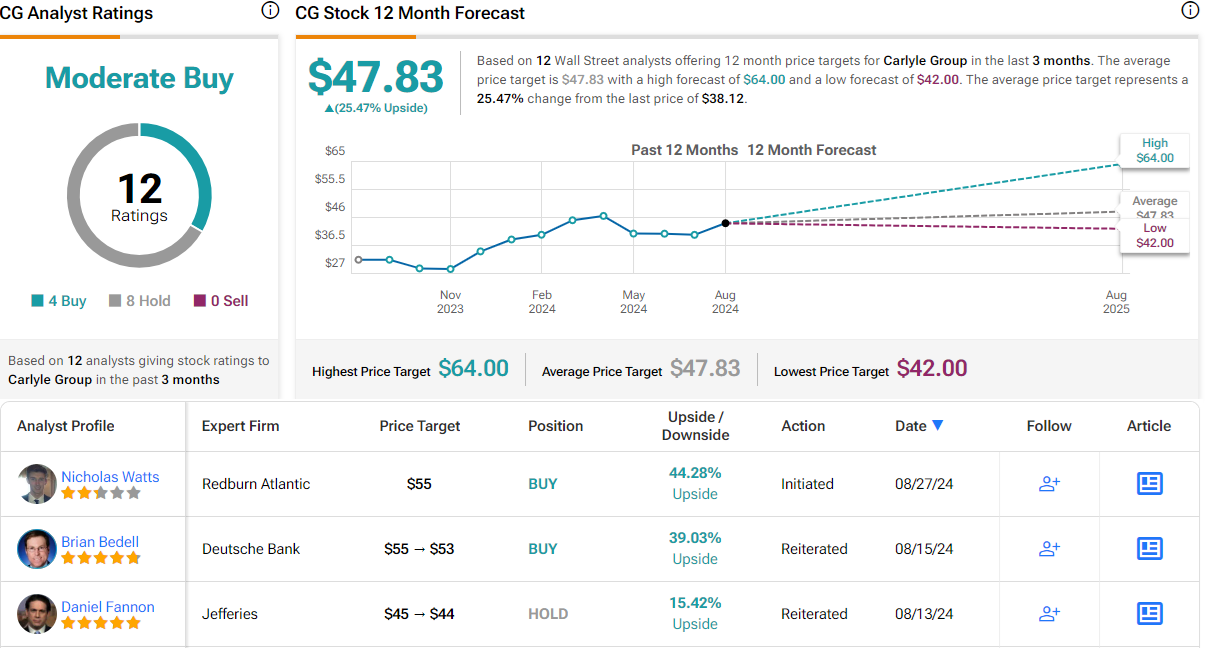

These comments back up the analyst’s Buy rating on the shares, and his $55 price target suggests a one-year gain of 44%. (To watch Watts’ track record, click here)

Overall, Carlyle Group’s shares have a Moderate Buy rating from the analyst consensus, based on 12 recent analyst reviews that include 4 Buys and 8 Holds. The stock has a current trading price of $38.12, and its $47.83 average price target implies a one-year upside potential of 25.5%. (See CG stock forecast)

Apollo Global Management (APO)

Next up is Apollo Global Management, a large-scale alternative asset manager with a market cap of more than $62 billion and 34 years of experience in the capital markets. The company serves both individual and institutional investors through its global network of offices, employing more than 780 investment experts. The company expects its total AUM to reach as high as $1 trillion by 2026.

Like Carlyle Group above, Apollo operates primarily through three main segments. Of these, the smallest is the real assets segment, which was holding $88.2 billion in AUM as of this past June 30. The next largest segment is Apollo’s equity business, with $105 billion in AUM overseen by more than 250 experienced investment professionals. The equity segment has seen investments in more than 300 portfolio companies since Apollo’s inception in 1990.

By far the largest part of the company’s business, however, is the credit segment. This segment has a total of $502 billion in assets under management, based on some 3,000 issuer relationships. These are monitored by more than 380 of Apollo’s professional investment staff, across the company’s global office network.

In addition to these segments, Apollo also has considerable interest in the insurance industry. The company is the owner of the global insurance giant Athene, with which it had a strategic partnership until 2022 – the year that the two companies completed a merger that saw Athene come fully under Apollo’s name. The insurance/financial services segment of Apollo’s business had $354 billion in AUM at the end of December last year and has more than 30 regulatory relationships in the global insurance industry.

In its Q2 earnings report, despite record fee-related earnings (FRE) of $516 million and a strong performance in the asset management unit, the decline in profits from the Athene insurance unit outweighed these gains. Overall, adjusted EPS for Q2 reached $1.64, falling short of the $1.75 consensus estimate, and declining from $1.72 in the prior quarter and $1.70 a year ago.

Nevertheless, Watts, opening up new coverage of this stock, is impressed by the solid AUM growth, among other growth factors. He says of Apollo, “Since 2016, Apollo has grown both AuM and FRE by 19%. Relative to its 2026 targets, Apollo is tracking in line from an AuM and FRE perspective, but well ahead of its target for SRE (spread related earnings), which has more than offset the more challenging environment for principal investment income (PII).”

The analyst believes that this company has more to offer investors than is generally accepted, and explains why, writing, “The market has proven reluctant to grant the company full credit for this performance. Since acquiring Athene (its primary insurance business), the stock has traded at a material discount relative to the sector. This discount reflects the business’ balance sheet-intensive approach (compared with peers) and implicit concerns around the credit exposure Apollo carries in the event of a broader economic and credit quality deterioration. We argue that the market is overweighting these risks and has given the company insufficient credit for the unique ecosystem it has constructed and its track record of execution.”

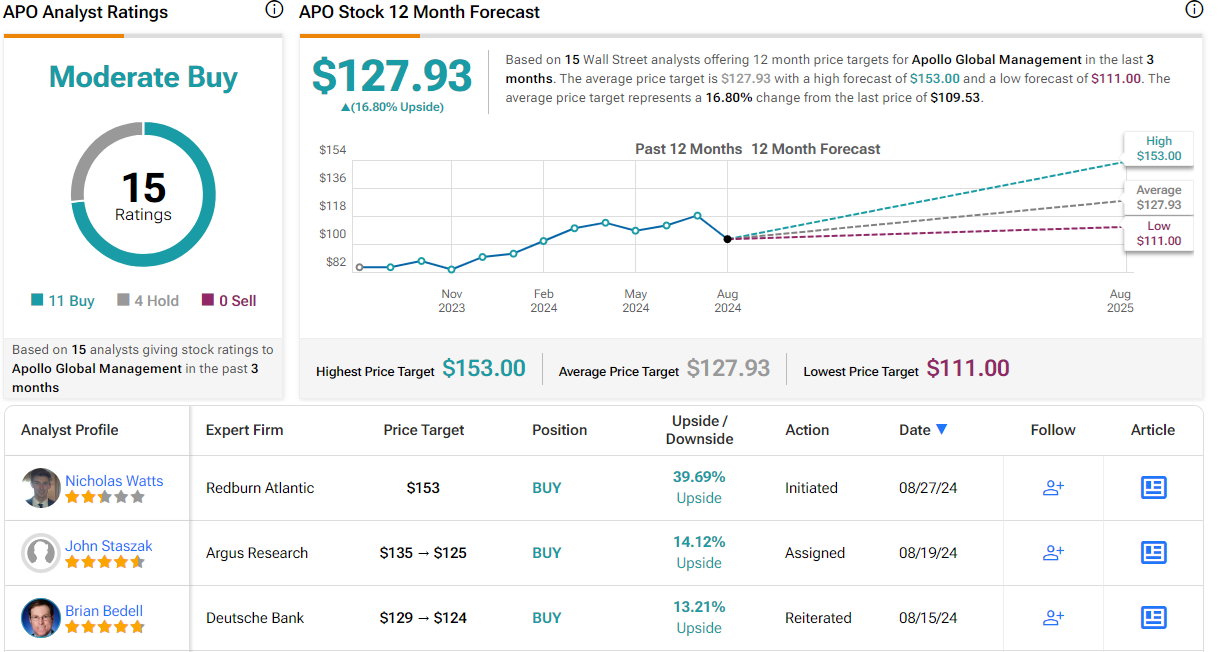

Summing up, Watts rates APO stock as a Buy, a rating that he backs up with a $153 price target that points toward an upside of 37% in the next 12 months.

Apollo’s analyst consensus rating is a Moderate Buy, derived from 15 reviews with a breakdown of 11 Buys and 4 Holds. The stock’s $127.93 average target price and $109.53 current trading price together suggest a 17% gain on the one-year horizon. (See APO stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.