The Fed bumped rates 75bp on Wednesday, and sent the stock market onto a roller coaster. What spooked investors were the comments by Federal Reserve Chairman Jerome Powell, who quickly dashed any prospect for a pause in the Fed’s tightening policy, and went on to snuff out hopes for an easy end to the current economic headwinds.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

“It is very premature to be thinking about pausing. People when they hear ‘lags’ think about a pause. It is very premature, in my view, to think about or be talking about pausing our rate hikes. We have a ways to go,” Powell said.

He went on to talk about the longer term, and that’s when investors got really nervous. On the path forward, toward a potential ‘soft landing’ for the economy, Powell said, “We’ve always said it was going to be difficult, but to the extent rates have to go higher and stay higher for longer it becomes harder to see the path. It’s narrowed. I would say the path has narrowed over the course of the last year.”

Powell’s words have helped solidify fears of a recession early next year – and have also strengthened the case for a defensive investment portfolio. Using the TipRanks database, we’ve looked up two stocks that fit the bill: high-yield dividend payers, one with a yield above 8%, offering investors some protection from inflation. And even better, analysts are forecasting double-digit upside potential for each. Let’s take a closer look.

Ladder Capital Corporation (LADR)

If you talk about dividends, you almost certainly have to talk about real estate investment trusts (REITs), since these are among the most reliable high-yield div payers in the markets. REITs buy, own, manage, and lease a wide range of real properties and mortgage assets and securities in both the commercial and residential markets. Ladder is a specialist in commercial mortgages, currently holding over $5.9 billion in assets. The company provides capital and financing to underwrite commercial real estate; in addition to its portfolio of mortgage assets, Ladder also owns properties in the net lease commercial market.

Coming off the COVID restrictions, Ladder saw its revenues peak in Q2 of this year – but while the recently reported Q3 results were down from that peak, they are still elevated year-over-year. In the third quarter, Ladder reported a top line of $118 million, up 23% from the year-ago period, and net income came in at $28.7 million, or 23 cents per diluted share. This compares favorably to the $18 million in net income reported, and 14-cent EPS, reported for 3Q21. The company did even better in distributable earnings, which came in at 27 cents per share.

Ladder finished 3Q22 with over $328 million in cash and liquid assets. The company’s deep pockets and high distributable earnings have, in recent quarters, made it possible for Ladder to bump up its common share dividend.

The new dividend payment is set at 23 cents per common share, or 92 cents annualized, and yields a high 8.5%. Investors should note that this dividend yield actually exceeds the last official inflation print (8.2% for September), meaning LADR shares are still bringing in a real rate of return for dividend-minded stock traders.

Ladder’s attractive return potential has caught the eye of 5-star analyst Stephen Laws, from Raymond James, who says: “Given the strong 3Q results and outlook for higher rates, we are increasing our 2022 and 2023 estimates. Our Strong Buy rating is based on the attractive portfolio characteristics, our portfolio return estimates, the internal management structure, high insider ownership, and attractive valuation…”

That Strong Buy rating comes with a $13.50 price target, implying a one-year upside potential of ~30%. (To watch Laws’ track record, click here)

Overall, this small-cap REIT has picked up 4 recent analyst reviews, which break down 3 to 1 in favor of Buys over Holds (i.e. Neutral) for a Strong Buy consensus rating. The shares are selling for $10.40, and the $12.63 average price target suggests an upside of ~21% from that level. (See LADR stock analytsis on TipRanks)

Algonquin Power & Utilities (AQN)

Now will shift our attention to the utility sector, an other sector that is frequently seen as ‘recession proof,’ and has a reputation for offering solid dividends – both attributes that will likely be in high demand going forward.

Algonquin Power & Utility is, as its name tells, a player in the North American utility sector. The Canadian-based company controls over $16 billion in assets, and provides electricity, water, and natural gas utility services to more than 1 million customers. Algonquin is also developing a portfolio of wind, solar, hydro, and thermal power generation, for clean, renewable electricity production. The company’s renewable generation capacity, at full build-out, is currently planned for 4 gigawatts.

The fourth and first quarters are Algonquin’s peak period, so the last quarter reported, 2Q22, shows the expected sequential slip. At the same time, the top line of $624.3 million was up 18% year-over-year. The company’s total adjusted net earnings hit $109.7 million, for a 19.6% y/y gain. The earnings increase was narrow on a per-share basis, but still substantial at 7% y/y; 2Q adjusted EPS was reported at 16 cents. The company will report its Q3 results on this coming November 11.

Algonquin has made several important announcements recently. In September, the company agreed to a ‘path forward’ on its acquisition of Kentucky Power, a transaction that is priced at $2.646 billion, including Algonquin’s assumption of $1.221 billion in debt. Pending regulatory approval, the purchase is expected to close in January, 2023.

In early October, Algonquin announced the inauguration of its asset recycling transactions, a program under which the company will begin selling ownership interests in its renewable energy production projects. The first transaction is the sale of 49% ownership of three operational wind farms in the US with a total of 551 megawatts capacity, and an 80% interest in a 175 megawatt facility in Canada. Algonquin is expected to realize cash proceeds of US$227 million and C$107 million from the sales.

And on the dividend front, Algonquin has declared its 3Q22 dividend, paid out to holders of common shares on October 14. The dividend was set at 18 cents per share in US currency. At that rate, the payment annualizes to 72 cents per common share, and yields 6.6%. While below the rate of inflation, the yield is still more than triple the average found among the market’s dividend stocks – and it is reliable, as the company has been keeping up its payments steadily since 2012.

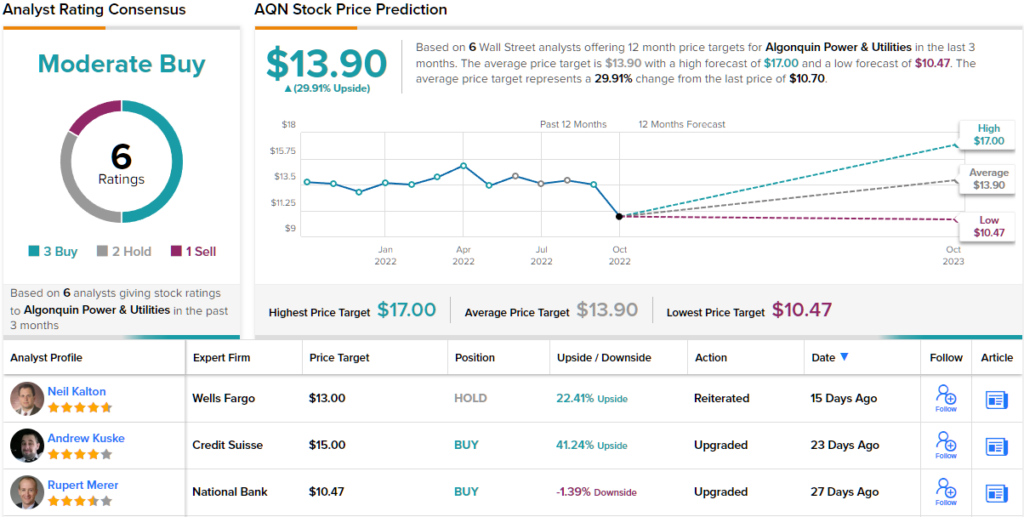

This stock is covered by Credit Suisse, where analyst Andrew Kuske sees ‘plenty of positives.’ He writes, “Recently, AQN benefitted from two events: (a) a downward price revision for the Kentucky deal; and, (b) the firm’s first major capital recycling announcement (Ramping up the Recycling) with the potential for more to follow. On the horizon, benefits from the Inflation Reduction Act and the investor day (usually December) could provide positive incremental news flow…”

Considering the positives, Kuske rates AQN shares an Outperform (i.e. Buy) with a $15 price target to indicates a potential upside of ~41% in the months ahead. (To watch Kuske’s track record click here)

What does the rest of the Street think? Looking at the consensus breakdown, opinions from other analysts are more spread out. 3 Buys, 2 Holds and 1 Sell add up to a Moderate Buy consensus. In addition, the $13.90 average price target indicates ~30% upside potential. (See AQN stock analysis on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.