The COVID-19 pandemic resulted in the biggest blowback the hospitality industry has arguably ever seen in such a short period of time. With global restrictions suspending international travel and various types of activities and the working-from-home economy taking over, whether we are talking about tourism or business trips, the industry suffered dramatically.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Accordingly, shares of hotel giants like Hyatt Hotels (NYSE: H), Hilton Worldwide (NYSE: HLT), airlines like United Airlines (NASDAQ: UAL) and Delta Air Lines (NYSE: DAL), as well as booking services like Booking Holdings (NASDAQ: BKNG) and Expedia Group (NASDAQ: EXPE), plummeted at the time.

While most of these companies have seen their shares recover from the pandemic lows, it’s clear that the industry has taken a different turn. In this article, I want to focus more on how travelers’ needs and preferences have changed in a post-COVID world and which company appears the most well-positioned to enjoy the upside from these effects.

Who Benefits the Most from Consumers’ Shifting Habits

As I mentioned, the travel industry as a whole was eventually set to make a full recovery. Traveling volumes would eventually reach their past highs and even exceed them. Thus, airlines, for instance, would eventually recover (save for rising fueling costs, but that’s another topic). However, the biggest shift, in my view, was where travelers chose to stay.

Historically, hotels have been the go-to place when it comes to traveling, either for business or leisure. With the rise of Airbnb (NASDAQ: ABNB) over the past decade, travelers were given the option to experience unique stays in distinctive locations, resulting in hotels starting to face headwinds.

The COVID-19 pandemic gave Airbnb the final boost it needed to power this trend for real. Sure, Airbnb’s revenues also suffered during the pandemic, but the underlying trend of choosing unique stays over bland hotels, though, was cemented.

Don’t be fooled by the recovery in shares of companies like Hilton, Marriot, and Hyatt. Their revenues have yet to reach their pre-pandemic levels. On the contrary, the revenues of Airbnb have skyrocketed since, exhibiting the shift in staying preferences. Over the past 12 months, the company’s revenues reached new records, at $7.38 billion compared to the pre-pandemic Fiscal 2019’s levels of $4.81 billion.

There are many catalysts behind this shift, and the best part is that these catalysts are still in place. For instance, while the working-from-home trend has softened, remote working appears to be here to stay. The rise of digital nomads globally is a testament to that. Entrepreneurs running small businesses via their laptops leave behind expensive metropolia and move to villas in Bali for 1/4 of their small NYC apartment.

The comments of Airbnb’s CEO Brian Chesky during the company’s latest earnings call verify that this movement is even accelerating.

“Guests continue to stay longer on Airbnb. They’re not just traveling Airbnb; they’re now living on Airbnb. We saw long-term stays of 28 days or more remain our fastest-growing category by trip nights compared to 2019. The long-term stays have increased nearly 25% from a year ago. And actually, long-term stays have increased almost 90% since Q2 2019.”

However, even when it comes to traveling for leisure, with Airbnb’s popularity skyrocketing and travelers having the option to stay anywhere from cheap Bungalows to literally a castle, soulless hotels have become a hard Sell.

Why Airbnb is Your Best Bet in a Post-COVID World

In my view, Airbnb is investors’ best bet in a post-COVID-19 world due to its lean, high-margin business model, combined with the ongoing shifting trend in stays. The rest of the travel industry is going to continue to face powerful challenges, moving forward. Airlines, for instance, are being greatly impacted by elevated fuel costs, while the ever-escalating war in Ukraine could long sustain this.

Hotel operators lack any meaningful growth prospects as well. Additionally, they trade at rather ridiculous multiples. Hyatt trades at nearly 29x its projected Fiscal 2024 earnings. Hilton trades at 18.4x its projected Fiscal 2024 earnings. Who is paying this much in the current environment on such a forward-looking basis?

When it comes to Airbnb’s industry peers like Booking and Expedia, I am not bearish. They also feature lean operations and high margins. Still, they lack the current growth catalysts Airbnb is experiencing.

The company is snowballing its top and bottom line, gradually becoming a free-cash-flow machine. In its latest Q2-2022 earnings report, Airbnb generated nearly $800 million of free cash flow out of just $2.1 billion in revenues, and its margins have only now started to expand.

Consequently, during the ongoing market decline, I have been loading the truck with shares of Airbnb and avoiding most of its industry peers.

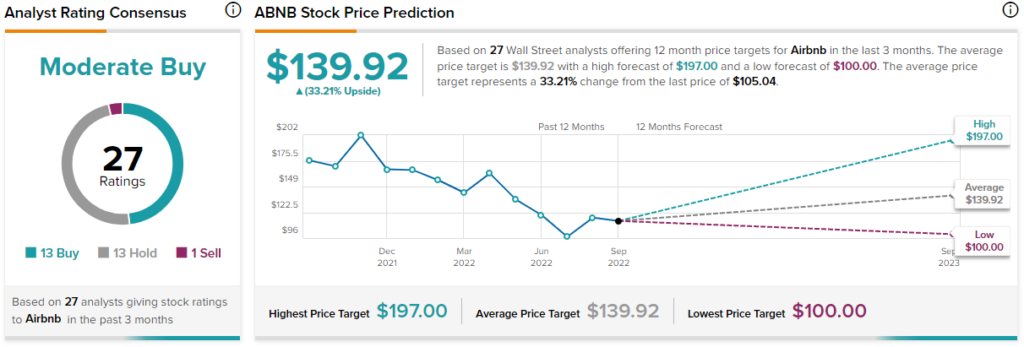

What is the Target Price for ABNB Stock?

With Airbnb’s profitability proliferating, Wall Street analysts have become increasingly bullish on the stock. The stock has a Moderate Buy consensus rating based on 13 Buys, 13 Holds, and only one Sell assigned in the past three months. At $139.92, the average Airbnb stock projection implies 33.2% upside potential.