In this piece, I evaluated two social media stocks, Pinterest (NYSE:PINS) and Snap (NYSE:SNAP), using TipRanks’ comparison tool to determine which is better. Pinterest is a visual discovery engine that helps users find recipes, inspirations for their home or personal styles, and more. Snap, the parent company of the messaging app Snapchat, defines itself as a technology company that believes the camera offers the best opportunity to improve the way people live and communicate.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Shares of Pinterest are up 15% year-to-date but only 6% over the past year, while Snap shares have gained 5% year-to-date but remain in the red over the last year, off 19%.

With such a significant difference in their year-to-date gains, it shouldn’t be a surprise that their valuations are quite different as well. Neither company is profitable, so we’ll compare their price-to-sales (P/S) ratios to each other and to that of their industry to gauge their valuations against those of their peers.

For comparison, the internet services and social media industry is currently trading at a P/S ratio of 6.2 versus a figure of 4.5 in Q1. On another comparative note, Facebook parent Meta Platforms (NASDAQ:META), the original poster child social media, is trading at a P/S of 6.5.

Pinterest (NYSE:PINS)

At a P/S of 6.5, Pinterest is trading in line with Meta’s valuation and at a large premium to Snap. Although the company is not profitable now, it was profitable in 2021, and it continues to generate positive free cash flow. However, because Pinterest doesn’t deserve a valuation in line with Meta’s yet, a bearish view seems appropriate.

Pinterest was a huge pandemic-era winner as people were forced to stay home, but in mid-2021, people started venturing out, and Pinterest saw a sharp decline in active user growth in the fourth quarter of 2021. However, in the most recent quarter, management told CNBC that it was the company’s best user growth quarter in over two years, with global monthly active users up 8% year-over-year to 465 million.

Meanwhile, the company has smashed adjusted earnings-per-share estimates in three of the last four quarters, including a more than threefold beat for the March quarter. Pinterest also came out slightly ahead regarding revenue estimates in three of the last four quarters.

Overall, the company’s fundamentals are trending in the right direction quarter-over-quarter as CEO Bill Ready, appointed in 2022, appears to have things well in hand. However, Pinterest doesn’t yet deserve a valuation in line with Meta’s, so it makes sense to wait for a more reasonable entry point.

What is the Price Target for PINS Stock?

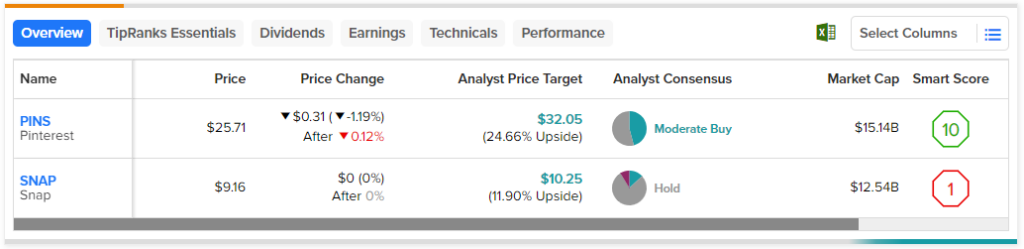

Pinterest has a Moderate Buy consensus rating based on 11 Buys, 13 Holds, and zero Sell ratings assigned over the last three months. At $32.05, the average Pinterest stock price target implies upside potential of 24.7%.

Snap (NYSE:SNAP)

At a P/S of 3.4, Snap is trading at a steep discount to its industry and Pinterest. However, a closer look reveals some issues, suggesting a bearish view may be appropriate.

An analysis of insider selling trends for Snap suggests management isn’t very optimistic about the company’s future. Insiders have unloaded $3.6 million worth of shares over the last three months, including multiple “Informative Sells.” Those sales also include many auto-sells that may have been part of the insiders’ preset trading plans, which automatically trigger a sale at certain times or prices.

Unlike Pinterest, Snap has never been profitable on an annual basis and shows no signs that profitability is imminent. The company even failed to turn a profit in 2021, when Pinterest benefited significantly from the worldwide lockdowns and recorded its first annual profit.

While Snap beat EPS estimates in the last two quarters, it has come up short of the consensus numbers for revenue in three of the last four quarters. Although it continues to put up impressive year-over-year growth in daily active users, that increasing scale hasn’t been enough to move the needle on profitability, as evidenced by Snap’s net income margins of -31% in 2022 and -30% for the last 12 months. In fact, one analyst warned in December that Snap may generate any earnings until 2027.

What is the Price Target for SNAP Stock?

Snap has a Hold consensus rating based on three Buys, 18 Holds, and two Sell ratings assigned over the last three months. At $10.25, the average Snap stock price target implies upside potential of 12.45%.

Conclusion: Bearish on PINS and SNAP

Social media stocks have long been Wall Street darlings, but the time of reckoning has come. Investors now have less patience for unprofitable tech names — as they should. However, the good news is that Pinterest is on the right track, although it doesn’t deserve a valuation equal to Meta’s yet. On the other hand, it doesn’t look like Snap has any chance of becoming profitable anytime soon — or perhaps ever. Thus, Pinterest is the winner of this pair, although I’m bearish on both names.