Driving curiosity in the market recently is downstream hydrocarbon energy specialist Phillips 66 (NYSE:PSX). Specifically, hedge fund Elliott Management – founded by activist investor Paul Singer – acquired a stake of about $1 billion in the energy enterprise. In exchange for the support, Elliott seeks big changes in the company. However, a second catalyst involving favorable options dynamics may catapult sentiment. In turn, I am bullish on PSX stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

A Proven Case That May Benefit PSX Stock

At face value, Elliott Management’s interest in PSX stock may be enough to sustain optimistic sentiment toward the business. Much of the argument centers on the hedge fund’s proven success story with Phillips 66 rival Marathon Petroleum (NYSE:MPC). In Elliott’s letter to the former enterprise, the activist emphasized its plans with Marathon in 2019, which ultimately led to improved operating performances.

What’s more, it’s difficult to argue with the results. Over the trailing five years, MPC shares gained nearly 146%. During the same period, PSX – inclusive of its recent rally – only moved up around 44%. What’s more, as TipRanks contributor Steve Anderson pointed out, Phillips 66 CEO Mark Lashier enjoys the support of Elliott regarding plans to turn the company around.

Still, as Anderson is quick to note, Elliott’s endorsement is modestly backhanded. While it’s behind the turnaround plan, the activist also expects to see “meaningful progress” in the next year. Otherwise, the hedge fund could pull support. Stated differently, the clock is on Lashier to make good. Ultimately, that’s a strong case for PSX stock.

Keep in mind that Marathon isn’t the only entity outperforming Phillips 66. Elliott’s letter also mentioned downstream peer Valero Energy (NYSE:VLO). Over the trailing five years, VLO gained more than 66%, less than MPC but superior to PSX stock. It’s difficult to argue against basic math, particularly when the targeted company acknowledges its shortcomings.

Options Dynamics the Likely ‘Real’ Catalyst for Phillips 66

While activists sometimes light up a fire under their targeted enterprises, their involvement is also not a surefire catalyst. Research into activist investor campaigns reveals that success rates are mixed. While performance may improve in the near term, returns typically become negative after a half-year period. So, it’s quite possible that PSX stock could be responding to another catalyst: favorable options dynamics.

Specifically, it appears that bearish traders were caught off guard by Elliott’s stake in Phillips 66 and the subsequent rise in its shares. Looking at options flow data – which exclusively filters for big block transactions likely made by institutions – a major entity bought 695 contracts of the Jan 19 ’24 115.00 put on November 17, paying a premium of $294,540.

At the time of the above transaction, PSX stock traded hands at $115. At writing, shares trade at roughly $128. Even more compelling, in July, another major player sold 1,245 contracts of the Jun 21 ’24 110.00 call. That’s incredibly problematic for the call writer because this option is in the money (ITM) for countervailing call holders.

What’s more, the open interest for this option stands at 1,284 contracts. Thus, it’s quite possible that whoever bought these calls never sold them, waiting for the day that PSX stock would come good. That day is right now, adding to the anxieties of bearish investors.

If the price of PSX continues to rise, the losses that the call writer may incur in covering the position will likewise accelerate, and financially, it’s well within reason that Phillips 66 could attract new investors.

A Good Deal Yet

Despite the rising value of PSX stock, it’s still relatively underappreciated. Currently, the price/earnings (PE) ratio of PSX lands at 7.74x, 45% lower than its 10-year average. Also, the downstream component of the hydrocarbon energy value chain (that is, refining and marketing) features a PE ratio of 8.38x.

Looking forward, if Phillips 66 implements the actions requested – which include improving refining operations and possibly selling the company’s Speedway retail operation – the value of PSX stock may potentially skyrocket. Thus, daring investors may want to secure this deal now before it no longer offers a discount.

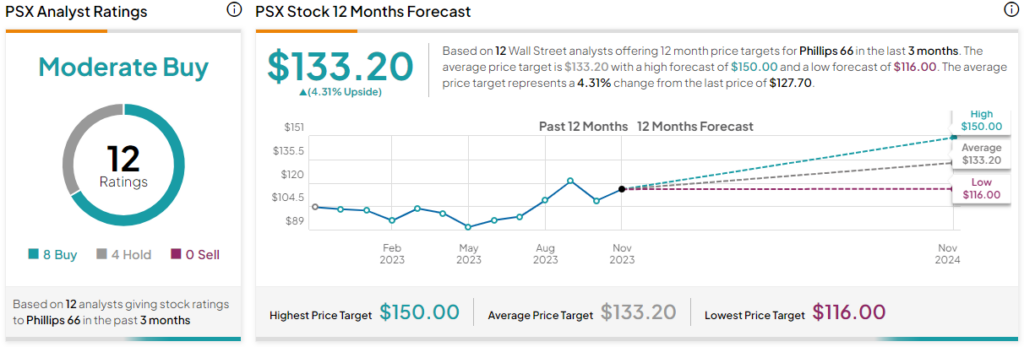

Is PSX Stock a Buy, According to Analysts?

Turning to Wall Street, PSX stock has a Moderate Buy consensus rating based on eight Buys, four Holds, and zero Sell ratings. The average PSX stock price target is $133.20, implying 4.3% upside potential.

The Takeaway: PSX Stock Has Enough Legs for More Upside

With activist investor Elliott Management lighting a fire under the seat of Phillips 66, it put pressure on management to make good for stakeholders. That alone may be enough to justify a speculative position. However, it’s also quite possible that bullish options dynamics may be the true catalyst for PSX stock. Either way, circumstances look quite favorable for the optimists.