A few days ago, Philip Morris (NYSE:PM) announced another dividend hike (now yielding 5.4%). The international tobacco giant behind Marlboro, IQOS, and SHIRO, among other iconic smoke and smoke-free brands, remains a resilient option for investors seeking growing income with little volatility involved. In fact, I believe that the dividend prospects for Philip Morris will improve further. Hence, I am bullish on the stock.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Was Philip Morris’ Dividend Increase Meaningful?

After Philip Morris announced its dividend increase last Wednesday, some investors raised concerns about its perceived lackluster impact. To be fair, it’s understandable why they might feel that way. The quarterly dividend rate was bumped up by a mere 2.4% to reach $1.30, a rate that admittedly falls short of exciting.

This sentiment is particularly poignant, considering that Philip Morris primarily attracts income-oriented investors. Given that this increase failed to outpace inflation, it’s no surprise that many were left disappointed.

Nevertheless, I see Philip Morris’ decision to incrementally grow the dividend as a strategic one. It positions the company to expedite its deleveraging process, a crucial step following the acquisition of Swedish Match, which necessitated taking on additional debt. To put things in perspective, the company’s total debt ballooned to nearly $48 billion by the end of Q2 (from around $28 billion.

Management’s choice to prioritize debt reduction in an environment of rising interest rates, given this financial burden, is a prudent and logical decision. Once a substantial portion of the debt is paid down, I anticipate that management will feel more at ease in accelerating the pace of its dividend growth.

In the meantime, Philip Morris shareholders have compelling reasons to hold onto their positions. The stock continues to offer an exceptional yield, well-timed albeit modest dividend increases, and maintains stable, low-volatility trading performance. Notably, the company has consistently increased its dividend payout every year, a tradition dating back to its affiliation with Altria (NYSE:MO). As a result, both entities can proudly claim an impressive 54-year streak of consecutive annual dividend increases.

This remarkable track record speaks volumes about Philip Morris’ robust business model and the unwavering dedication of its management team to enhance shareholder value.

How Safe is Philip Morris 5.4%-Yielding Dividend?

The fact that Philip Morris only marginally increased its dividend may suggest to some that the company is struggling to afford it. However, this is hardly the case. As I mentioned, the main reason behind the modest hike is for the company to prioritize deleveraging. Besides, its financial results and guidance support this argument.

Specifically, in the second quarter, Philip Morris delivered a standout performance, hinting at the possibility of a record-breaking year. PM’s net revenues surged to an impressive $9.0 billion, boasting a substantial 14.5% year-over-year increase (or a robust 14.9% on a currency-neutral basis), firmly establishing this quarter as a historic zenith in the company’s sales history. Notably, these figures include the added revenues from the Swedish Match acquisition.

If we set aside Swedish Match’s numbers, Philip Morris achieved an admirable 10.5% organic growth in net revenues. This remarkable feat can be attributed to several key factors:

- A 3.3% uptick in total cigarette and heated tobacco unit (HTU) shipments (with HTUs seeing a remarkable 26.6% growth rate while cigarettes experienced a modest 0.4% dip)

- A favorable shift in the product mix toward smoke-free alternatives within its portfolio

- An impressive 9% increase in combustible tobacco prices

Beyond its noteworthy Q2 revenue growth, Philip Morris also caught investors’ attention by surpassing Wall Street’s EPS estimates. The company’s adjusted EPS soared to a remarkable $1.60, exceeding consensus expectations by $0.10 and signaling an impressive year-over-year growth rate of 16.9%. Looking ahead after a strong first half of the year, Philip Morris’ management confidently projects an adjusted EPS range of $6.46 to $6.55 for Fiscal 2023.

This forecast suggests a year-over-year growth rate ranging from 8.0% to 9.5%, setting the stage for yet another year of all-time-high profits. Importantly, the midpoint of management’s guidance suggests a payout ratio of 79.8%, which is actually below the company’s historical average. I also support the case for a re-acceleration in dividend growth, assuming the necessary deleveraging takes place.

Is PM Stock a Buy, According to Analysts?

As far as Wall Street’s view on the stock goes, Philip Morris boasts a Strong Buy consensus rating based on seven unanimous Buy recommendations assigned in the past three months. At $116.71, the average Philip Morris stock price target suggests 21.8% upside potential.

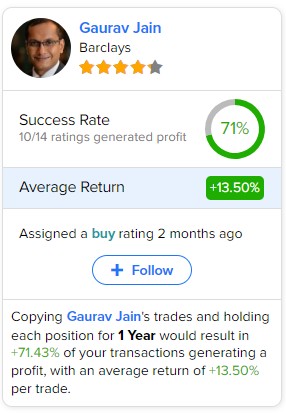

If you’re wondering which analyst you should follow if you want to buy and sell PM stock, the most profitable analyst covering the stock (on a one-year timeframe) is Gaurav Jain from Barclays, with an average return of 13.5% per rating and a 71% success rate.

The Takeaway

Overall, while some may view Philip Morris’ recent dividend increase as modest, it reflects a strategic move to prioritize debt reduction following the acquisition of Swedish Match. Management’s prudent financial approach, combined with the company’s rock-solid Q2 results, signals a promising outlook. Further, with a track record of consistent dividend increases and strong financial results, I believe that Philip Morris remains an attractive choice for income-oriented investors.

As the company continues to deleverage and expand its profitability, we can anticipate brighter days ahead for its dividend growth.