Leading tobacco giant Philip Morris International (NYSE:PM) is scheduled to announce its second-quarter results on July 20. While forex headwinds and the continued weakness in cigarette volumes seem concerning, robust pricing and the demand for smoke-free products are expected to drive Q2 earnings.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Philip Morris sells cigarettes, smoke-free products, associated electronic devices, and other nicotine-containing products in over 180 markets outside the U.S. The company aims to increase the proportion of the revenue derived from its smoke-free products to at least 50% by 2025 compared to 35% in 2022, with the ultimate aim of phasing out cigarettes completely.

Analysts’ Q2 Earnings Estimates

Philip Morris delivered mixed results for Q1 2023. Adjusted EPS declined 13% year-over-year to $1.38 but exceeded estimates. The Marlboro maker’s revenue grew 3.5% to $8 billion but lagged the Street’s expectations. PM lowered the full-year outlook, citing supply chain issues and higher tobacco leaf prices, energy, and labor costs.

The company guided for Q2 adjusted EPS in the range of $1.42 to $1.47, driven by high single-digit organic top-line growth. Meanwhile, analysts expect the company’s Q2 adjusted EPS to increase to $1.50 from $1.48 ($1.32 excluding Russia and Ukraine operations) in the prior-year quarter. Revenue is expected to rise about 12% to $8.76 billion.

Ahead of the Q1 print, Goldman Sachs analyst Bonnie Herzog reiterated a Buy rating on Philip Morris with a price target of $120, saying PM remains one of her top stock picks.

Herzog sees the possibility of the company beating Q2 estimates and raising its full-year outlook, fueled by the strength of its iQOS (heated tobacco device) offering. That said, the analyst cautioned that currency fluctuations remain a wildcard. The analyst expects earnings visibility to improve as the year progresses, backed by the accelerated rollout of ILUMA (latest generation heated tobacco product), continued innovation, and increased penetration of iQOS.

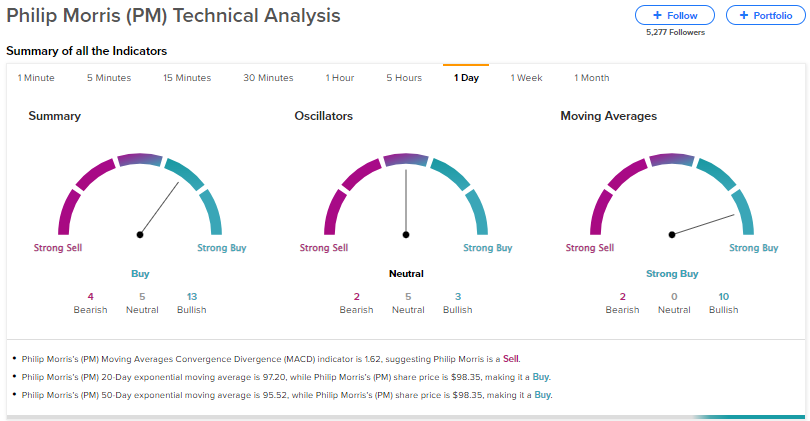

Technical Indicators Ahead of PM’s Q2 Earnings

Ahead of the Q2 earnings release, technical indicators reveal that PM is a Buy. According to TipRanks’s easy-to-understand technical tool, PM’s 50-Day EMA (exponential moving average) is 95.52, while its price is $98.35, making it a Buy. Further, PM’s shorter duration EMA (20-day) also signals an uptrend.

Is PM a Buy or Sell?

With eight Buys and one Hold rating, Wall Street has a Strong Buy consensus rating on Philip Morris stock. The average price target of $115.25 implies 17.2% upside potential. Shares are down 3% year-to-date. PM offers an attractive dividend yield of 5.1%.

Conclusion

Despite cost-related challenges and forex headwinds, Wall Street’s sentiment on Philip Morris’ Q2 results appears to be positive. The company’s pricing power and momentum in the smoke-free products are expected to favorably impact its performance.