Back in 2021, few would have thought that PayPal (NASDAQ:PYPL), a fintech titan, would have lost about 80% of its value over the span of two-and-a-half years. Despite the Nasdaq Composite’s remarkable recovery from last autumn’s lows, PayPal stock has not only failed to recover from its historic slump, but it’s proceeded to sink even lower than last year’s lows. Given mounting competitive headwinds, I’m inclined to believe PayPal isn’t as great a bargain as it seems.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Indeed, the pain struck many of the fintech darlings months before the broader market rolled over to start 2022. There may be a new bull market in the S&P 500 (SPX) and Nasdaq (NDX), but the battered fintech heavyweights still seem to be sinking under their own weight. For now, I have to be bearish on PayPal, as I do not see an easy way out for the former fintech top dog as competitors chip away at its moat.

PayPal’s Ecosystem is Becoming Less Moat-Worthy as Big Tech Targets Payments

Looking back, it’s clear many investors overestimated the growth potential for PayPal. Despite operating in one of the most compelling areas of the tech sector (financial technology), PayPal’s share price has succumbed to macro headwinds hitting payments and competitive pressures. Undoubtedly, there is value in the PayPal ecosystem.

However, as more competitors, most notably FAANG/big-tech companies, spread their wings across the realm of digital (and even point-of-sales) payments, PayPal needs to put its “innovation hat” on to prevent users from doing business with rivals that have superior service ecosystems encompassing more than just digital payments.

For instance, a tech titan like Apple (NASDAQ:AAPL) has an ecosystem that’s the envy of the tech scene. The company offers impressive services, including cloud storage, entertainment (video, music, and gaming), and, of course, payments and other financial services.

Regarding financial services, Apple seems to be doing something unique — it’s tilting the tables in favor of users while helping them improve their financial “hygiene.”

Indeed, the financial services business typically entails skimming fees off the top of transactions, collecting large sums of interest on loans, and charging rates on deposits well below market rates. Late to repay your outstanding credit card balance? The banks are completely fine if you pay the minimum balance and rack up the interest.

What Apple does differently is it’s able to offer financial services that are more attractive than what currently exists. With the Apple Card, the company is fully transparent about how much interest a user would have to pay on outstanding balances, and with the Apple Savings Account, the company is doing what no big banks would dream of doing — offering competitive interest rates at or around market rates.

Why is Apple sacrificing potential profit for the financial health of its users? It wants to beckon new users in a market that’s ripe for disruption.

Undoubtedly, Apple is reinventing how everyday people think about financial services. As the company continues to grow its offerings, like Savings, Apple Tap to Pay, Apple Pay Later, Apple Pay, and Apple Wallet, the fintech pioneers (PayPal included) do not seem to have much of an answer as FAANG firms cover more bases in financial services.

PayPal Stock is Historically Cheap, Though

PayPal stock is trading at a historically cheap multiple at 17.7 times trailing price-to-earnings, well below its five-year historical average of 54.64 times. The stock’s historically depressed multiple suggests the growth days are probably not coming back. In the latest quarter, PayPal saw revenue growth of just 7%, a far cry away from the double-digit top-line growth it used to command a few years ago.

While PayPal’s foray into cryptocurrencies represents a potential wild card, I just do not see a way that a PayPal-branded digital token can return the stock to its former glory and its former growth multiple. It’s ugly out there for the fintech darlings as numerous tech companies set their crosshairs on digital payments.

Despite the low price of admission, I think the only way PayPal can grow is if it takes a margin hit straight to the chin. Investors won’t be happy with such a move in a rising-rate environment. Unfortunately, I don’t think there are many options if PayPal is to stay competitive in this new era of fintech.

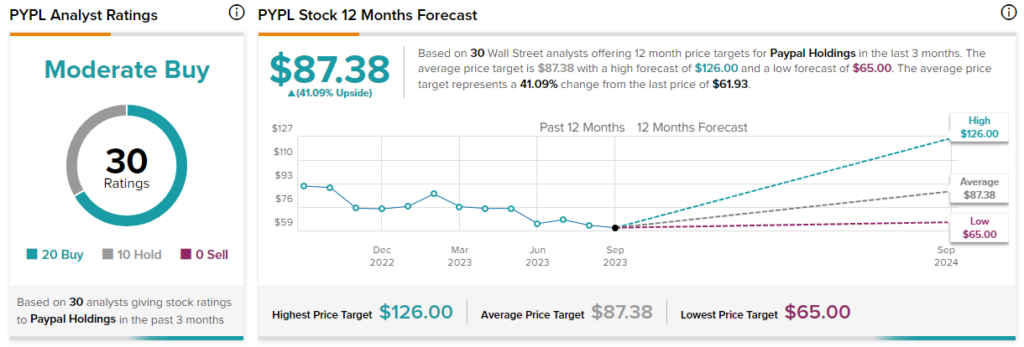

Is PayPal Stock a Buy, According to Analysts?

On TipRanks, PYPL stock comes in as a Moderate Buy. Out of 30 analyst ratings, there are 20 Buys and 10 Holds. The average PayPal stock price target is $87.38, implying an upside of 41.1%. Analyst price targets range from a low of $65.00 per share to a high of $126.00 per share.

The Bottom Line

It’s hard to love PayPal, even with its P/E in the teens — not when tech giants are getting so aggressive with their expansions into digital payments. Unfortunately, I think there’s a real risk that PayPal could lose meaningful ground to rivals in the near future. Further, investment firm Elliot Management’s recent exit from its PayPal stake also does not give me a vote of confidence.