Following a run of disappointing earnings results, PayPal (PYPL) delivered the goods in Q2, with the company beating Street expectations for the quarter. With the digital payments titan readying to deliver Q3’s financial statement once today’s trading comes to a close, might a repeat be in the offing?

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

For Deutsche Bank analyst Bryan Keane, Q3 beats are certainly not out of the question. “We see potential EPS upside in the quarter led by strong cost control and operating leverage which should continue into FY23,” the analyst said ahead of the print.

The signs also bode well for the revenue haul. Against a backdrop of growing macro concerns, as comps start to ease and ticket sizes “remain high” on account of inflation, various ecommerce data points suggest “acceleration” compared to 1H22’s growth figures.

Despite apprehension around discretionary consumer spending, according to Signifyd, worldwide ecommerce rose by low-double-digits in the quarter, compared to the low-single-digits uptick of 1H22.

More specifically for PayPal, increasing engagement via the “super app” could also play its part.

“We estimate that PYPL will need to increase its engagement ~18% Y/Y in order to reach its FY22 guidance,” the 5-star analyst explained, “followed by ~14% and 13% in FY23 and FY24.”

A look at PayPal’s website traffic on TipRanks also paints a promising picture. Sequentially, unique visitors (UVs) are up by 11%, and by a more impressive 52% from the same period last year.

While beats are certainly on the menu for Q3, the revenue guidance might disappoint, with Keane noting some “some projections for slowing eComm growth in 4Q22.”

All told, the analyst is calling for revenue growth of ~9% year-over-year (~12.0% cc) to $6.74 billion, and EPS to reach $0.94.

So, what does it all mean for investors? Keane reiterated a Buy rating on PYPL shares along with a $140 price target. Should the figure be met, investors will be sitting on returns of 81% in a year’s time. (To watch Keane’s track record, click here)

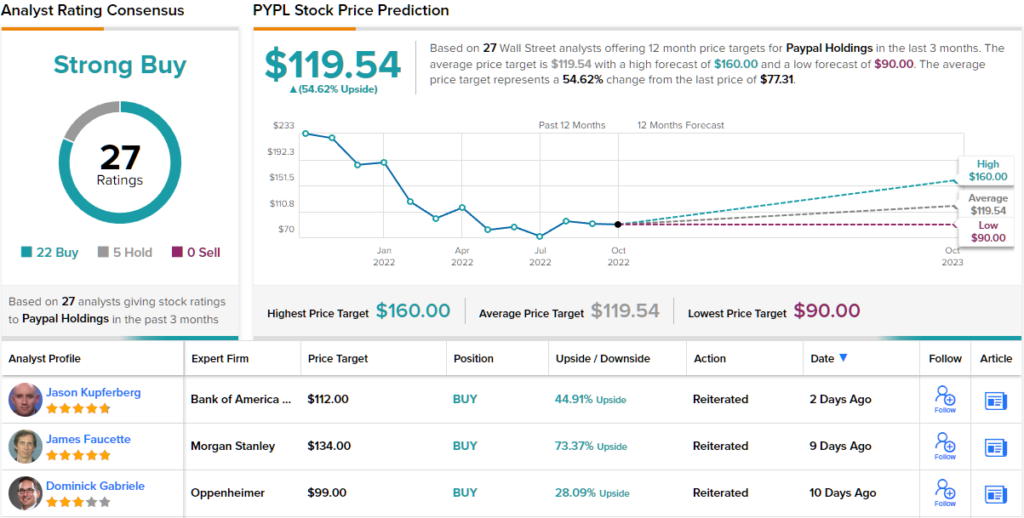

Most on Wall Street back Keane’s thesis. The stock garners a Strong Buy consensus rating, based on 22 Buys vs. 5 Holds (i.e. Neutral). There’s decent upside projected too; at $119.54, the average target makes room for 12-month growth of ~55%. (See PayPal stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.