The past year has been brutal for PayPal (PYPL) stock. The digital payments pioneer has suffered at the hands of market rotation and has had to contend with investors turning away, as the company has been unable to sustain the huge growth seen during the height of the pandemic.

But is it time to start reassessing PayPal’s prospects? According to a digital wallet survey undertaken by investment firm Baird, analyst Colin Sebastian thinks the trend is signifying it might be time to do so.

“On a year-over-year basis,” said the 5-star analyst, “our survey indicates the number of e-commerce sites integrating with wallets, including PayPal/Venmo, Apple Pay, Google Pay and Amazon Pay, increased by more than 80%.”

Corresponding with this significant pivot toward e-commerce, numerous merchants are also adding various payment options, including alternative financing (BNPL/install pay).

It also appears merchants are eagerly seeking out new ways to improve conversion rates, given only around 50% of online shopping “sessions” in which consumers add products to their baskets ever reach the checkout pages.

As such, Sebastian believes “steady (or even accelerating) trends with respect to merchant integration with digital wallets is a key medium- and long-term positive for PayPal.”

On the other hand, given the overall positive merchant adoption trends, others are also making a dent in the ecommerce universe and are providing PayPal with competition which “continues to increase.” As noted above, Apple Pay and Google Pay’s online adoption is gaining traction, and finally Amazon Pay is making inroads too.

Nevertheless, while Sebastian heeds some caution given the current macro headwinds, slower growth and competition, given the “multiple growth drivers across commerce, payments, financial services, and merchant services,” the analyst still views PayPal as a “secular winner.”

Overall, Sebastian keeps his Outperform (i.e. Buy) rating for PYPL intact, yet “reflecting lower comparable multiples,” the analyst lowered his price target from $205 to $175. Still, there’s ~44% upside potential from current levels. (To watch Sebastian’s track record, click here)

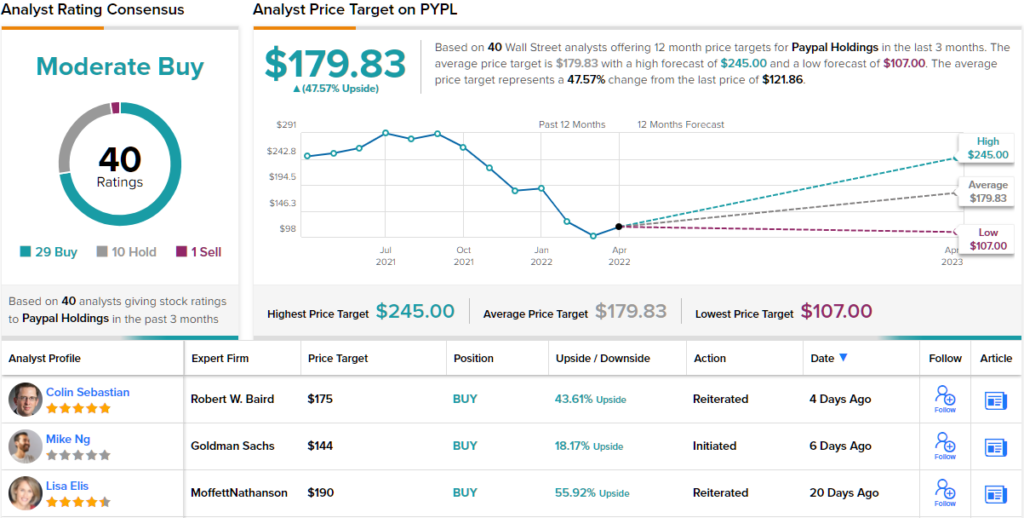

Looking at the consensus breakdown, based on 29 Buys vs. 10 Holds and a single Sell, this stock claims a Moderate Buy consensus rating. The average price target is a touch higher than Sebastian’s, and at $179.83, represents potential one-year gains of ~48%. (See PayPal stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.