Investors looking for a guiding hand to steer them safely through the current hazardous stock market landscape could do worse than listen to what billionaire Ken Fisher has to say.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

The Fisher Investments founder famously started his independent money management firm with $250 in 1979, a company that is now a $197-plus billion going concern, while Fisher’s own net worth stands north of $5 billion.

So, for those getting restless from 2022’s unrelenting bear, Fisher has some very simple advice: “The things that tend to drop the most in a bear market, when you get to the other side and come up the other side of the V, whenever it is, tend to bounce the most early on. So, that’s why patience is a virtue… If you become patient, you’ll become worth more money.”

Turning to Fisher for inspiration, we took a closer look at two stocks the billionaire made moves on recently. Using TipRanks’ database to find out what the analyst community has to say, we learned that each ticker boasts a “Strong Buy” consensus rating from the analyst community. Let’s see why they are considered good investment choices right now.

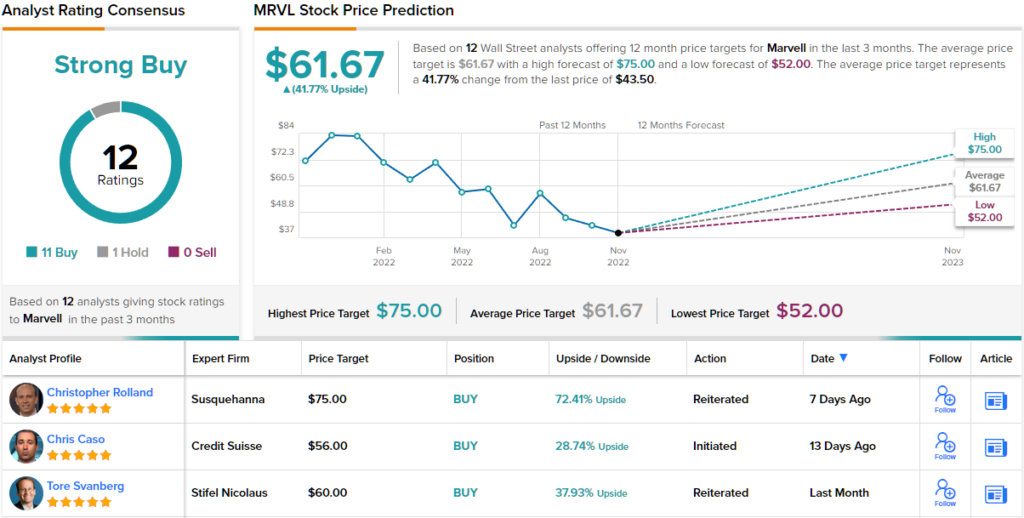

Marvell Technology (MRVL)

The first Fisher-endorsed stock we’ll look at is a chip industry stalwart. Marvell is a maker of semiconductors and associated tech. The integrated circuit specialist serves a wide range of markets from data centers to automotive, enterprise networking to cloud and carrier infrastructure, amongst others. Following various acquisitions, the company’s primary source of revenue has shifted from the consumer electronics sector to data infrastructure (data center, industrial, automotive, mobile network).

Meanwhile, Marvell’s revenue and earnings have been trending in one direction – up. And though supply chain issues have made their presence felt, Marvell still managed to meet Wall Street expectations.

The company will be releasing its fiscal third-quarter on December 1, but in the meantime, we can get a good feel for the company’s situation by looking back at the F2Q22 numbers. Specifically, revenue climbed by 41% from the same period a year ago to $1.52 billion, meeting Street expectations, while the company delivered adj. EPS of $0.57, coming in $0.01 above the $0.56 consensus estimate.

However, citing supply chain hitches, for FQ3, the company expects revenue of $1.56 billion, missing the $1.58 billion anticipated by the analysts, while for the bottom-line, the outlook called for adj. EPS of $0.59 at the midpoint, below consensus at $0.61.

Overall, Marvell has been unable to withstand the bearish market forces and the shares have tumbled ~50% this year.

Fisher obviously thinks they represent excellent value. He upped his stake considerably in Q3, and bought 11,133,134 MRVL shares, now worth in excess of $478 million.

Echoing Fisher’s bullish stance, Credit Suisse’s Chris Caso sees plenty to like about the chip company.

“Our longer-term favorable view of MRVL is due to the number of company-specific drivers that account for well over half of the Street revenue growth expectations heading into CY23,” the 5-star analyst explained. “Those drivers include hyperscale semi-custom silicon, the former Inphi business, automotive ethernet, the Innovium switch business and continued 5G rollouts. We expect that growth in all these areas is much less heavily dependent on end-markets, and will buffer against a market slowdown. In addition, spending by cloud operators has held up better than we would have thought given the compression in ad spending.”

Backing his comments, Caso rates MRVL shares an Outperform (i.e. Buy) while his $56 price target makes room for 12-month gains of 28%. (To watch Caso’s track record, click here)

His colleagues agree – almost unanimously so. While one analyst favors sitting this one out, all 11 other reviews are to Buy, providing the stock with a Strong Buy consensus rating. The average target is more bullish than Caso will allow; at $61.67, the figure suggests shares will gain ~42% in the year ahead. (See MRVL stock forecast on TipRanks)

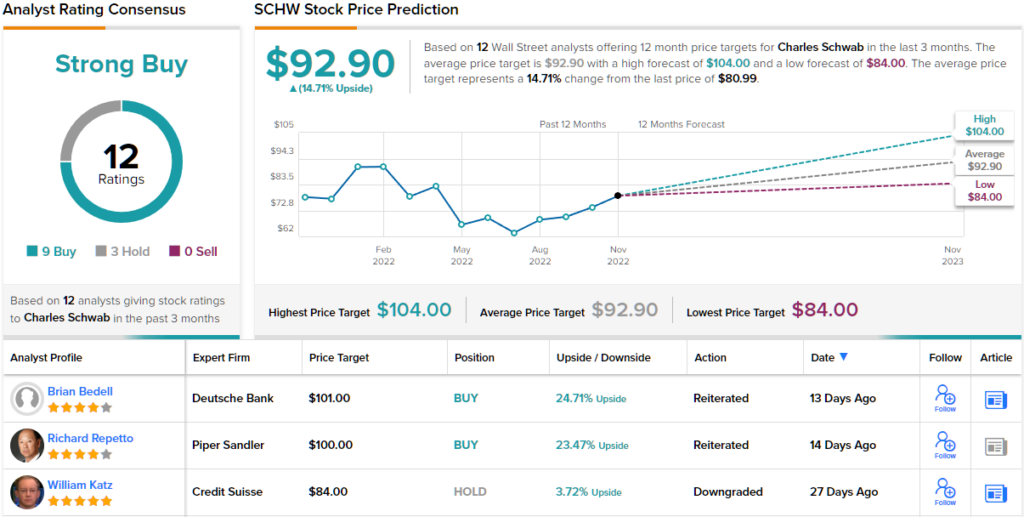

Charles Schwab (SCHW)

From the chip industry, let’s now pivot to an entirely different segment for Fisher’s next pick – to that of the financial services sector. Charles Schwab as a leader in the business of investment services, helping both retail and institutional clients invest in capital markets in a smart and efficient manner. Its services range from banking and securities brokerage to wealth and asset management, custody, and financial advisory services. Boasting around ~$7 trillion in client assets, the company is the U.S.’s 7th biggest banking firm.

Part of Schwab’s modus operandi is to collect as many deposits and cash as it can and invest it so to generate interest. This is especially helpful for the present climate in which interest rates are rising and has helped the company perform well in 2022’s depressed environment.

In the latest quarterly report, for 3Q22, revenue rose by 20% year-over-year to $5.5 billion, while beating the Street’s call by $80 million. The company generated a record $2 billion in net income, compared to the $1.5 billion delivered in the same period a year earlier. This resulted in adj. EPS of $1.10, trumping the Street’s $1.05 forecast.

Not wanting to miss out on a compelling opportunity, Fisher pulled the trigger on 15,433,332 shares, giving his fund a new position in SCHW. Looking at the value of the new holding, it comes in at almost $1.26 billion.

While J.P. Morgan’s Ken Worthington notes that the stock’s valuation is not cheap, he thinks there is good reason for that.

“We believe Schwab is a well-managed and highly valued company that trades at a premium to peers based on an industry-leading brand for retail financial services,” Worthington opined. “We view Schwab as a growth company with numerous initiatives to drive both incremental organic growth and a higher fee rate. We see Schwab benefiting from an engaged retail trading base that should drive a future generation of Schwab’s investor clients.”

To this end, Worthington rates SCHW shares an Overweight (i.e. Buy) while his $102 average target suggests investors will be pocketing returns of ~26% a year from now. (To watch Worthington’s track record, click here)

Looking at the consensus breakdown, with 9 Buys vs. 3 Holds, the analysts’ view is that this stock is Strong Buy. At $92.9, the average target implies 12-month share appreciation of ~15%. (See SCHW stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.