Palantir (NYSE:PLTR) finds itself uniquely positioned at the right place at the right time, helping its customers navigate an increasingly complex geopolitical and risk-oriented environment. The escalating demand for Palantir’s cutting-edge software solutions has translated into strong financials and a growing client base, setting the stage for lasting expansion. S&P 500 (SPX) inclusion has now become possible as well. Thus, further upside is not unlikely despite the stock’s 221.8% YTD rally. I remain bullish on the stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Q3 Results: Government Contracts Grow, Commercial Demand Follows

Palantir’s cutting-edge software solutions were initially crafted to empower government agencies in combating threats ranging from terrorism to the challenges posed by the COVID-19 pandemic. However, the overwhelming success and efficacy of these products have ignited a remarkable surge in commercial demand for Palantir’s software. In turn, this has transformed into a rapidly expanding revenue stream. In its Q3 results, Palantir posted robust growth in both segments, setting the stage for continuous success.

Specifically, in Palantir’s most recent quarterly report, revenue soared to an impressive $558 million, marking a 17% year-over-year increase and a 5% sequential rise, surpassing the upper limit of management’s earlier guidance range of $553 to $557 million. Excluding the impact of revenue from strategic commercial contracts, Q3 revenue experienced a remarkable 21% year-over-year surge and a 6% sequential increase.

Palantir’s software has continued to demonstrate its value, as revenue from its top 20 customers rose by 13% year-over-year to an impressive $54 million per customer in the trailing 12 months. Simultaneously, the company witnessed a substantial 34% year-over-year and 8% sequential increase in customer count. It reached a total of 453 customers, as Palantir remained dedicated to securing new accounts.

This exceptional growth suggests a promising trajectory for future revenues, especially considering the significant expansion of PLTR’s customer base compared to revenue growth. When customers initially engage with Palantir’s software, they essentially embark on a free trial or demonstration phase. Thus, once they gradually exit this phase, Palantir’s top line is likely to see a notable uptick in the coming quarters.

This already appears to be the case, as, along with strong growth in U.S. customer count, the company experienced U.S. Commercial revenue growth acceleration. Its U.S. Commercial top line reached $116 million, reflecting a remarkable 33% year-over-year increase and 13% sequential growth. Excluding strategic commercial contracts, U.S. Commercial revenue exhibited an even more impressive 52% year-over-year surge and a 19% sequential increase.

Palantir’s unwavering focus on its Commercial business, particularly its Foundry platform, has resulted in the company acquiring new customers and expanding existing opportunities. In a world increasingly shaped by risk, Palantir’s software has proven more relevant than ever.

Thus, while its Government business is steadily maturing (with Q3 revenues growing by 12% year-over-year and 2% sequentially to $308 million), the Commercial segment has only just begun to gain momentum. This has sparked growing excitement as the numbers speak to its promising future.

Profitability Improves, S&P 500 Inclusion Incoming

With Palantir’s revenues growing and its overall margins improving, the company has made substantial progress in terms of expanding its profitability. In fact, Q3 marked the fourth consecutive quarter of positive GAAP net income. This accomplishment has positioned Palantir for inclusion in the prestigious S&P 500 Index, a development expected to amplify its stock appeal as it garners increased interest from corresponding ETFs now obligated to incorporate it.

Specifically, Palantir achieved record GAAP net income of $72 million, representing a 13% margin. Notably, this marks the first time the company has attained both GAAP net income and GAAP operating profitability on a trailing 12-month basis. A noteworthy boost to the bottom line was the substantial increase in interest income, soaring from last year’s $5.5 million to an impressive $36.9 million, comprising more than half of the quarter’s profits.

This is due to Palantir’s sound balance sheet, boasting $3.28 billion in cash and zero long-term debt as of the end of Q3, a strategic advantage in the face of rising interest rates. With interest rates likely to remain elevated, interest income should continue to significantly contribute to the bottom line over the next few quarters, if not years.

Is PLTR Stock a Buy, According to Analysts?

As far as Wall Street’s view on the stock goes, Palantir features a Hold consensus rating based on three Buys, five Holds, and five Sells assigned in the past three months. At $15.00, the average PLTR stock price target forecast implies the potential for 24.81% downside potential, which may sound rather alarming.

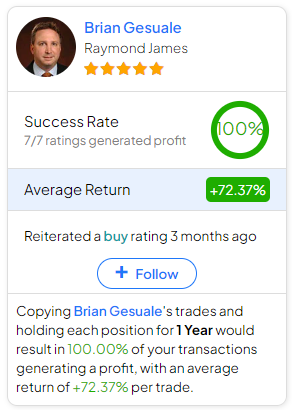

If you’re wondering which analyst you should follow if you want to buy and sell PLTR stock, the most accurate analyst covering the stock (on a one-year timeframe) is Brian Gesuale from Raymond James, with an average return of 72.37% per rating and a 100% success rate. Click on the image below to learn more.

The Takeaway

In conclusion, Palantir Technologies’ strategic positioning in navigating complex geopolitical landscapes has fueled its robust financial performance, evidenced by a reacceleration in revenues in Q3. Additionally, the surge in commercial demand, exemplified by a 34% year-over-year growth in customer count, indicates a promising trajectory.

In the meantime, the company’s expanding bottom line, marked by a record GAAP net income and the prospect of S&P 500 inclusion, underscores why Palantir’s investment case has become increasingly compelling over time.

With shares skyrocketing in recent months, Palantir’s valuation has expanded considerably, which could be a risk for current investors. Specifically, the stock is currently trading at about 19.6x FY2023’s expected revenues and at about 80-81x this year’s expected EPS.

However, given that Palantir’s financials are likely to keep accelerating from their already attractive growth levels, the company could quickly grow into its valuation in the coming years. There’s certainly some speculation involved here, but in the meantime, I choose to hold my Palantir shares tight and potentially add during dips.