If there’s one way to describe the markets recently, that would be top-heavy. The mega-caps, the largest US companies, have been outperforming the broader indexes, and by their very size they are pulling the rest of the markets along. To give an idea of the scale, the three largest S&P-listed companies are Apple, Microsoft, and Alphabet; together, they have a combined market cap over $6.9 trillion and make up a big chunk of the S&P 500’s total value. That $6.9 trillion is a higher market cap than every national stock market in the world outside of the US.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

This kind of scale makes the market giants hard to ignore. But that doesn’t mean investors have to stay locked into the few dominant mega-cap stocks. As BMO’s chief investment strategist Brian Belski points out, there are other games in town: “There is no denying the sharp outperformance of mega-caps in 2023 with the five largest stocks by market cap eclipsing the S&P 500 by 30 percentage points YTD and on pace to outperform for the fifth straight month. That being said, however, our work shows that once relative performance of these megacaps has subsided or winning streaks have ended, the broader market has historically held up just fine with gains being more common than losses.”

We can put Belski’s point into action and start following some of the smaller stocks with high upside. Using the TipRanks platform, we’ve pinpointed two equities in the small-cap category, both offering ‘Strong Buy’ ratings and both with more than 100% upside potential, according to the analyst forecasts.

Pliant Therapeutics (PLRX)

We’ll start with Pliant Therapeutics, a clinical-stage biopharmaceutical firm that focuses on the discovery and development of novel treatments for fibrotic diseases. Fibrotic diseases belong to a class where abnormal deposition of connective tissue, typically occurring during wound healing and scarring, obstructs and inhibits normal organ function. These diseases can affect various organ systems in the body, including the lungs and liver.

Pliant’s research pipeline, for the moment, is targeting diseases of those two organs, including idiopathic pulmonary fibrosis (IPF), primary sclerosing cholangitis (PSC), and NASH-associated liver fibrosis. These programs are currently at the clinical trial stage; the company has two additional research tracks, targeting solid tumors and various muscular dystrophies, undergoing preclinical studies.

The company’s ongoing clinical trials feature two leading candidates: PLN-74809, also known as bexotegrast, and PLN-1474. Last month, Pliant released data on the Phase 2a INTEGRIS-IPF trial, showing that bexotegrast demonstrated a ‘favorable’ profile in safety and tolerability, as well as positive indications of antifibrotic activity in the treatment of IPF (idiopathic pulmonary fibrosis). Data from the INTEGRIS-PSC trial, also a Phase 2a study of bexotegrast, is expected during 3Q23. Pliant’s third clinical-stage track is for PLN-1474, a potential treatment for NASH-associated liver fibrosis. A Phase 1 trial on this track has been completed, and showed positive results.

The pipeline here, particularly the IPF track, has attracted the attention of Canaccord analyst Edward Nash, who writes: “There is a sizable market opportunity in IPF with worldwide sales for both Esbriet and Ofev generating >$3.7B combined in 2021. We believe that bexotegrast’s potential superior efficacy, high selectivity, and minimal side effect profile coupled with an oral administration has the potential to garner significant market share, as well as the potential to be prescribed as an add-on therapy to current standard-of-care. We believe that bexotegrast could conservatively be a $1.7B drug in IPF in the out year of our projections, 2037.”

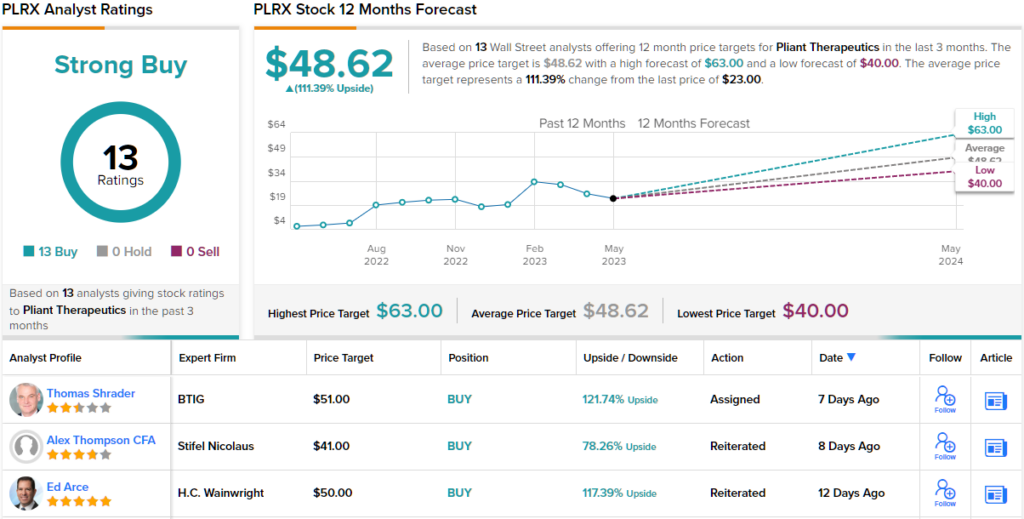

Quantifying his stance, Nash gives Pliant shares a Buy rating with a price target of $48 that suggests ~109% upside for the next 12 months. (To watch Nash’s track record, click here)

Overall, this stock gets the Street’s full support. Based on 13 positive analyst reviews, PLRX garners a Strong Buy consensus rating. The stock’s $23 trading price and $48.62 average price target imply a one-year upside potential of 111%. (See PLRX stock forecast)

Kura Oncology (KURA)

Let’s stick with the clinical-stage biopharmas, and take a look now at Kura Oncology. This company is focused on new precision medicines in the field of cancer treatment, and is working on creating new small-molecule drugs that will target cancer signaling pathways. Kura takes the additional step of pairing its drug candidates with molecular and/or cellular diagnostics, to develop a more precisely targeted medication by tailoring it directly to the patient – Kura’s treatments are directed at the patients most likely to show a positive response to the drug candidate.

Most of Kura’s pipeline is at the pre-clinical stage, with several drug candidates being investigated on multiple tracks. Leading the way, ziftomenib has multiple research lines ongoing. The most advanced pipeline track is the KOMET-001 clinical trial, in which the drug is being assessed as an oral inhibitor of menin-KMT2A (MLL) for the treatment of acute myeloid leukemia (AML). Evolving data from the Phase 1 KOMET-001 is expected on June 11 at the 2023 European Hematology Association (EHA) Congress in Frankfurt, Germany.

Kura has two more clinical trials getting started. The KURRENT-HN trial is a combination study looking at the drug candidate tipifarnib together with alpelisib in the treatment of certain head and neck squamous cell carcinomas. Enrollment here is ongoing, with determination of the biologically active dose expected in the middle of this year.

Additionally, the FIT-001 trial will be a dose escalation study of drug candidate KO-2806, an FTI inhibitor and potential treatment for several cancers including clear cell renal cell carcinoma. Patient dosing in FIT-001 is expected in 2H23.

All of this gives Kura plenty of ‘shots on goal,’ and BTIG analyst Justin Zelin sees that as a net positive for the company.

“Ziftomenib has shown promising Phase 1 data with clear evidence of clinical activity, differentiated pharmacological properties to revumenib and efficacy exceeding regulatory bars for approval. Kura is slated to be second to market, ~1 year behind in development, and we expect the important menin class will be sizeable enough to support multiple players with blockbuster potential for both Syndax and Kura,” Zelin noted.

“While investor focus has been on Ziftomenib, we expect Kura’s underappreciated Farnesyltransferase inhibitor (FTI) program will demonstrate combination proof-of-concept (POC) data in solid tumors, unlocking a large solid tumor opportunity with no competition in the class,” Zelin went on to add.

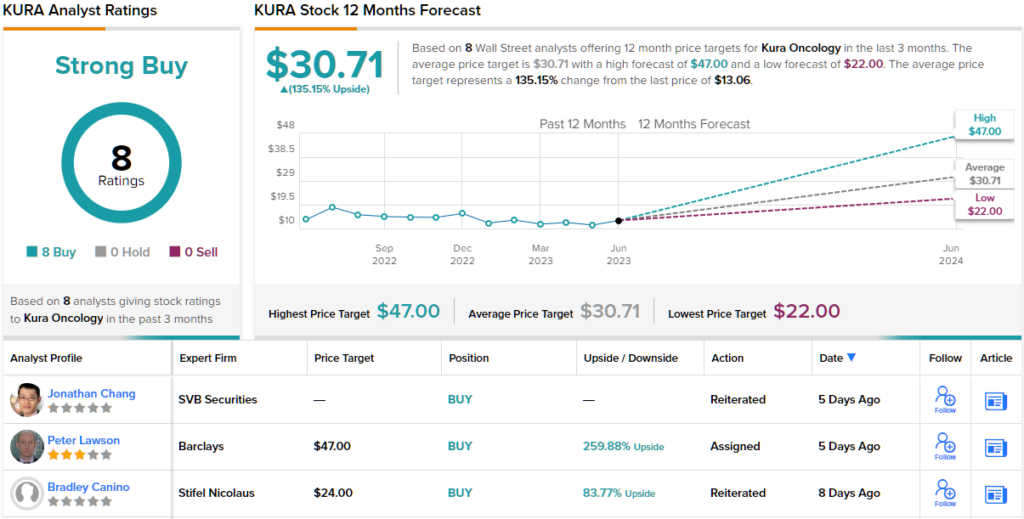

Looking ahead, Zelin gives KURA shares a Buy rating, and his $31 price target indicates his confidence in a 137% upside going out to the one-year time frame. (To watch Zelin’s track record, click here)

And what about the rest of the Street? Everyone is on board. The stock boasts a Strong Buy consensus rating, based on a unanimous 8 Buys. The forecast calls for 12-month gains of 135%, considering the average price target stands at $30.71. (See KURA stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.