Stock experts often tout the merit of taking the long-term view rather than looking for short term gains. It’s a strategy that gets the thumbs up from Morgan Stanley’s US Equity Strategy team, led by Mike Wilson.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Wilson has been one of the Street’s most vocal bears for a while, but while he does not see the bear market as over just yet, he forecasts a “stronger earnings picture” by next year. A friendlier monetary policy, high inflation receding, pent-up demand in investment/capex and in specific segments of consumer services, plus a recovery in global economic growth could all drive the next bull run.

As for the stocks that will lead the charge, Wilson has an idea about them too: “Our best long-term picks are based on the sustainability and quality of the business model, and opportunity to widen their competitive advantage.”

With this in mind, Wilson and his team have prepared a list called ‘30 for 2025’ filled with names that reflect those attributes – stocks that are ripe for the picking right now and set to generate handsome returns for the patient investor. We ran 3 of them through the TipRanks database to see what the rest of the Street makes of them. Here’s the lowdown.

Blackstone Group (BX)

Morgan Stanley’s recommended list is packed with market giants and the first name we’ll look at is certainly that. With $975 billion in assets under management (AUM), Blackstone is the world’s biggest alternative asset manager. As a financial product enabler, the company takes a diverse approach, and has over 12,000 real estate assets and 250 portfolio companies, whilst specializing in private equity, credit, hedge fund solutions, public debt and equity, amongst others.

As private investment companies, institutional investors and the wealthy look for different options beyond traditional investment routes, there’s a growing appetite for alternative assets.

Despite an overall drop in revenue, the company delivered a strong Q4 report against a backdrop of economic uncertainty. In the quarter, the company generated $43.1 billion of fund inflows, resulting in a total to $226 billion for the full year. As such, assets under management increased by 11% to $975 billion. Blackstone’s major source of income, fee-related earnings, saw a 9% uptick to reach $4.4 billion. Additionally, total distributable earnings climbed by 7% to $6.6 billion.

That has all helped Blackstone pay a juicy dividend. The quarterly payout currently stands at $0.91, which translates to a robust 5.3% yield.

While the shares have outperformed year-to-date – up 16% vs. the S&P 500’s 3% return – Morgan Stanley analyst Michael Cyprys thinks they are still way undervalued.

“We see a compelling entry point with shares trading at low-teens P/E on normalized earnings for a best-in-class franchise with unrivalled product breadth and distribution capabilities that can grow earnings faster than the market expects,” Cyprys explained. “BX’s long duration locked-up capital and $187b of dry powder enable BX to patiently wait for opportunities and time their exits. This yields significant firepower and staying power, which combined with their enviable brand should enable BX to navigate through cycle and come out stronger.”

These comments underpin Cyprys’ Overweight (i.e. Buy) rating while his $115 price target makes room for 12-month gains of 35%. (To watch Cyprys’ track record, click here)

Elsewhere on Wall Street, the stock garners an extra 9 Buys, 4 Holds and 1 Sell, for a Moderate Buy consensus rating. The average target stands at $102.31, suggesting the shares will climb ~20% higher in the year ahead. (See BX stock forecast)

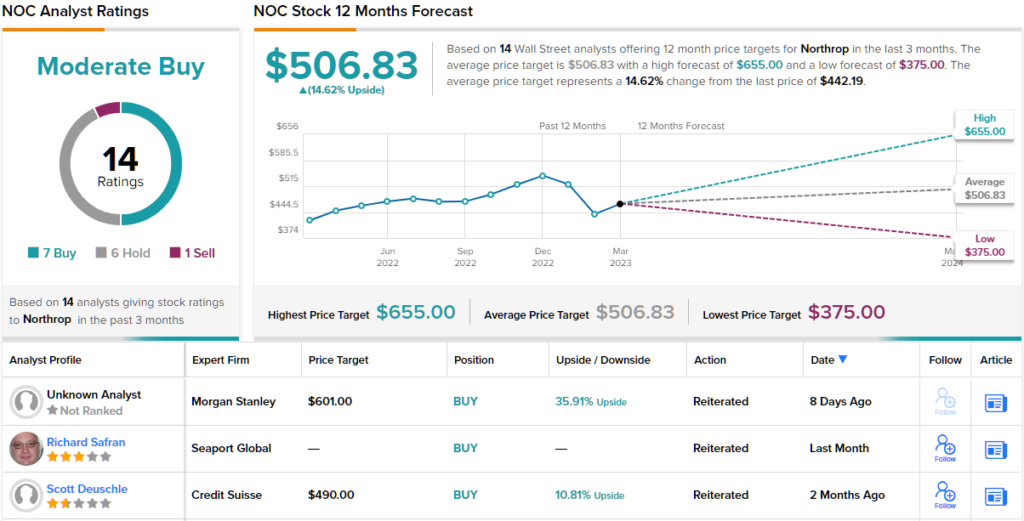

Northrop Grumman (NOC)

From one industry giant to another. With a market cap of $69 billion, over 90,000 employees and annual revenue above $35 billion, Northrop Grumman is one of the biggest A&D (aerospace and defense) companies in the world. The firm specializes in weapon manufacturing and is a provider of military technology, building defense vehicles, aircrafts, ships and space systems, amongst them the world’s most powerful space telescope – the James Webb Space Telescope.

It’s a recipe that served the company well in its most recent earnings – for 4Q22. Revenue rose by 16.6% year-over-year to of $10.03 billion, beating the Street’s forecast by $390 million. Adjusted earnings climbed 25% from the same period a year ago to $7.50, coming in well ahead of the $6.57 consensus estimate. Looking ahead to FY23, the company called for revenue in the range between $38 to $38.4 billion. Consensus had $37.85 million.

That said, the strong quarterly performance has been overshadowed in recent times by fears around the costs related to one of the company’s flagship programs – the development of the B-21 Raider stealth bomber. However, Morgan Stanley analyst Kristine Liwag says the concerns might be “overdone.” In fact, Liwag thinks the stock is one made for these “uncertain times.”

“We see NOC as the Defense ballast to own,” Liwag said. “Peer-high growth in 2023 and a >20% FCF growth CAGR through 2025 offer conviction… Space is a continued standout in the portfolio and we see management’s surprise at the extent of competitive program wins in this domain as a good problem to have. While NOC’s margins are not immune to macro pressures in 2023 and YoY pension headwinds weigh on non-cash earnings, the long-term story for NOC remains intact.”

Accordingly, Liwag rates NOC an Overweight (i.e. Buy), backed by a $601 price target. The implication for investors? Upside of ~36% from current levels. (To watch Liwag’s track record, click here)

Turning now to the rest of the Street, where 6 additional Buys and Holds, each, plus 1 Sell, provide the stock with a Moderate Buy consensus rating. Given the average target currently stands at $506.83, the analysts see shares rising ~15% in the year ahead. As an added bonus, Norhtrop also pays a $1.73/share quarterly dividend, which currently yields 1.56%. (See NOC stock forecast)

Eli Lilly & Co (LLY)

The last Morgan Stanley pick we’ll look at also belongs in the giant group. Eli Lilly is a multi-national pharmaceutical firm, and in fact, with a market-cap of almost $315 billion, is bigger than both the above companies combined.

With an almost 150-year-old history and with its products sold in around 125 countries, LLY has a storied background, being the first company to mass-produce the polio vaccine and one of the first to produce human insulin using recombinant DNA. Its famous products include depression drug Prozac and diabetes drugs Humalog (insulin lispro) and Trulicity. The latter was Eli Lilly’s biggest revenue generator last year, raking in ~$7.4 billion.

However, in the recently reported Q4 earnings, Trulicity fell short of Street estimates, delivering $1.9 billion in revenue – amounting to ~3% year-over-year growth. Additionally, with its COVID antibody therapies adding just $38 million in sales vs. $1 billion+ in the year ago period, revenues fell by 9% y/y to $7.3 billion, falling short of the Street’s call by $74 million. However, the company posted a strong beat on the bottom-line, as adj. EPS of $2.09 came in ahead of the $0.85 forecast.

LLY also has an active drug development pipeline. With results expected during H123 from both the Phase 3 study of Alzheimer’s candidate donanemab and from the Phase 3 trials of Mounjaro for obesity, Morgan Stanley’s Terence Flynn thinks there could be volatility in LLY shares. Yet, while projecting a 60% probability of success for the former, for the latter Flynn does not expect any surprises and anticipates the data will “support a filing/approval of the drug in obesity.”

All told, Flynn considers LLY a Top Pick and explaind why he thinks the stock deserves a lofty valuation. He writes: “Our thesis on the stock is unchanged as we continue to expect Mounjaro and LLY’s other new product cycles (Pirto for CLL,Lebri for AD and Miri for IBD) to drive a best-in-industry rev/EPS growth profile (2023-2030 rev/EPS CAGR of 10%/18%) and operating margin expansion with 2025 EPS of >$16 vs. ~$8 in 2022, deserving of a premium P/E multiple vs. the industry 2024 average of ~15x.”

What it all boils down to is an Overweight (i.e. Buy) rating that sits alongside a $444 price target. Should the figure be met, investors will be pocketing returns of ~33% a year from now. (To watch Flynn’s track record, click here)

Most on the Street agree with Flynn; based on a total of 11 Buys, 3 Holds and 1 Sell, the analyst consensus rates this stock a Moderate Buy. (See LLY stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.