When I recommended Nvidia (NASDAQ:NVDA) stock last November, the semiconductor firm was poised to benefit greatly from the impending artificial intelligence (AI) boom. Since then, it has risen from $195 to over $455. So, the pressing question is, has NVDA reached its peak, or is there still room for upside this year? I believe NVDA represents a long-term growth opportunity that’s flourishing amid the AI boom. Consequently, I perceive the recent decline from its all-time high of ~$502 as a buying opportunity.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

NVDA’s Marvellous Q2 Beat and Promising Q3 Outlook

On August 23, NVDA reported outstanding Q2 results. Revenues grew 101% year-over-year to $13.5 billion, significantly beating the company’s own revenue guidance of $11 billion provided in the preceding quarter.

GAAP EPS exhibited extraordinary growth as well, surging by 854% year-over-year and 202% sequentially to reach $2.48. Even more noteworthy is the remarkable improvement in its gross margin, as it soared to an impressive 70.1% compared to 43.5% in the prior-year period and 64.6% in the previous quarter.

On top of that, the company outlined a promising outlook for the future, surpassing analysts’ expectations. Notably, for Fiscal Q3 2024, the company expects revenues to grow to $16 billion, much higher than analysts’ expectations of $12.5 billion. More positively, its adjusted gross margin is expected to hover around 72.5%.

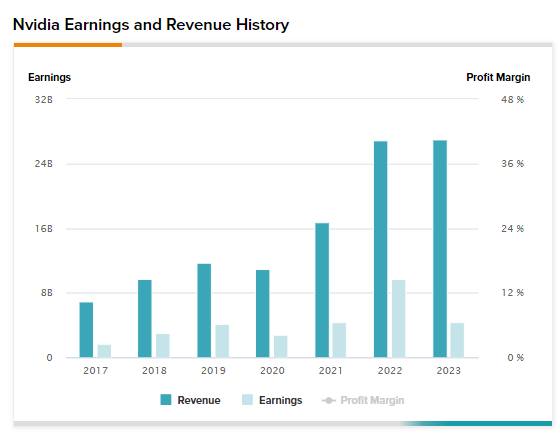

Is NVDA’s recent performance merely a one-off event, though? Let’s analyze its performance over a longer time frame. Looking at the last six years, NVDA’s revenues have almost quadrupled from $6.9 billion in Fiscal 2017 to $26.9 billion in Fiscal 2023 (NVDA’s fiscal year ends in January instead of December). What’s also applaudable is that its earnings have grown by 2.6x from $1.67 billion to $4.4 billion over the same period.

This data provides a substantial sense of reassurance in the robust business fundamentals and growth trajectory NVDA has consistently maintained over the years, even before the onset of the AI boom.

The AI Growth Story is Here to Stay — NVDA Will Benefit Greatly

Nvidia stock achieved a market capitalization of over $1 trillion in June 2023, making it the ninth company to reach this milestone. While some may believe that the potential of AI has already been fully realized, they could be mistaken.

I believe the AI growth story is here to stay, as the AI industry is still in its infancy and expected to continue delivering exceptional growth. In fact, the industry is expected to become a $1.85 trillion industry by 2030 versus approximately $207.9 billion in 2023, according to Next Move Strategy Consulting.

NVDA, in particular, has unmistakably demonstrated its dominant position in the AI industry in recent quarters. Offering a comprehensive range of services, including AI supercomputers, algorithms, data processing, and training modules, NVDA holds a competitive edge over its rivals in the AI market. Furthermore, NVDA remains at the forefront of innovation, solidifying its position as a leading provider of AI services across various industries.

As a result, NVDA is significantly ahead of its closest competitors. The company’s scale and dominant market share in the AI sector have led to remarkable top-line and bottom-line growth over the past quarters.

In light of this, NVDA’s revenue growth is likely to continue unabated. In fact, Wall Street analysts project NVDA revenues to double by the end of Fiscal 2024 compared to Fiscal 2023 and nearly triple from 2023’s baseline by the end of Fiscal 2025.

Meanwhile, NVDA’s EPS is also projected to surge to around $10.50 by the end of Fiscal 2024 and to $16 by the end of Fiscal 2025. These are indeed ambitious projections, but given NVDA’s track record of growth, they are not impossible to reach.

On another note, Nvidia CEO and co-founder Jensen Huang sold $42 million worth of NVDA shares recently. Does this suggest that the top management believes it’s time to start taking profits? It could, but on the contrary, the company initiated a buyback program worth $25 billion, signaling to the investor community that the stock is likely still undervalued relative to its true potential.

Is NVDA Stock a Buy, According to Analysts?

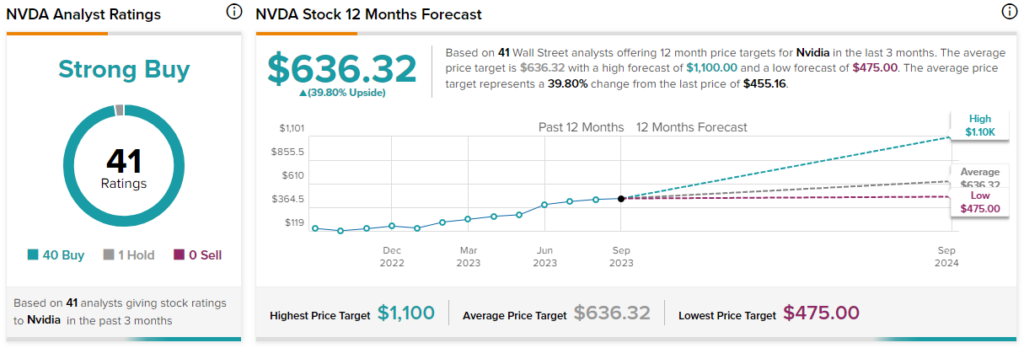

NVDA is that elusive titan — a widely covered stock on which almost every analyst is in accord. Given that it has received 39 Buy ratings and one Hold from analysts in the last three months, it has a Strong Buy consensus rating. The average NVDA stock target price of $636.32 implies 39.8% upside potential.

Breaking the Myth: NVDA’s Valuation Isn’t Expensive

In terms of its valuation, NVDA is currently trading at a forward P/E multiple of 42x. At first, this may look expensive. However, this is a much lower level compared to the P/E of 135x it was trading at just six months back. Further, its competitor Intel (NASDAQ:INTC) is trading at much higher levels (61x forward P/E), even though INTC has just begun its mark in the AI world and remains far behind NVDA.

The Takeaway

The indisputable fact is that Nvidia holds a leadership position in the AI market. The insatiable demand for AI chips should sustain the stock’s multi-year growth trajectory. While some investors might cash in on NVDA stock, I believe the occasional dips represent buying opportunities for those who believe in the firm’s ability to keep performing well.

Consequently, this is my approach: I will persist in purchasing NVDA stock, even when it hovers near its all-time highs, seizing the opportunities presented by occasional dips as they arise.