In this piece, I evaluated two chipmaker stocks, NVIDIA (NASDAQ:NVDA) and Advanced Micro Devices (NASDAQ:AMD), using TipRanks’ comparison tool to determine which is better. A deeper analysis suggests a bullish view for NVIDIA and a bearish view for AMD.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

NVIDIA develops graphics processing units (GPUs) semiconductors for artificial intelligence (AI), gaming, creative design, robotics, and autonomous vehicles. Meanwhile, AMD designs processors and related technologies for AI, data centers, gaming, and business-computing applications.

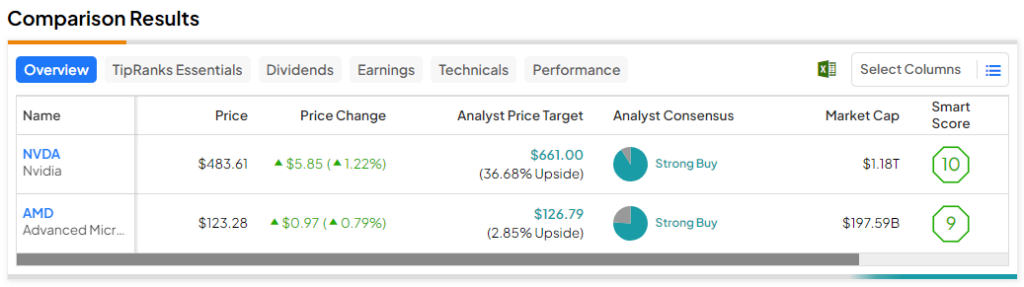

Shares of NVDA are up 240% year-to-date. Meanwhile, AMD stock has gained 93% year-to-date, including a 20% return over the last three months.

Despite NVIDIA’s much higher gains this year, it’s trading at a much lower valuation than AMD. We’ll look at their price-to-earnings (P/E) ratios to gauge their valuations against each other and that of their industry. For comparison, the U.S. semiconductor industry is currently trading at a P/E of 46.4 versus its three-year average P/E of 29.9.

NVIDIA (NASDAQ:NVDA)

At a P/E of around 64.3, NVIDIA is trading at a relatively small premium to its industry (compared to AMD’s premium anyway). In fact, the stock hasn’t been this cheap in a year, and its long-term gains also suggest a bullish view might be appropriate despite the tremendous year-to-date gain.

On a P/E basis, NVIDIA hasn’t been this cheap since December 2022. In fact, NVIDIA was trading at a P/E of over 100 just days ago — before the last earnings report. Of course, significantly higher earnings send a company’s P/E much lower if its stock price doesn’t change dramatically.

In NVIDIA’s case, its earnings exploded so much higher year-over-year that its P/E was cut nearly in half after just a small pullback from around $500 a share on November 22 to $489 on November 24. For its third quarter, the company reported adjusted earnings of $4.02 per share on $18.1 billion in revenue versus the consensus estimates of $3.37 per share on $16.2 billion in revenue.

On a comparative basis, NVIDIA’s revenue jumped 206% year-over-year and 34% quarter-over-quarter, while its adjusted earnings rose nearly sevenfold year-over-year and 49% quarter-over-quarter. The chipmaker’s GAAP (generally accepted accounting principles) earnings rose more than 13 times from a year ago to $3.71 per share, also demonstrating exploding growth.

Before that earnings report, NVIDIA shares had soared to a record high of around $505 with a P/E of about 120 in November. Normally, I wouldn’t suggest a bullish view of a stock that has risen so much, so fast.

However, once the market recognizes its lower valuation — and recovers from management’s warning about significantly lower sales to China and other countries due to export restrictions — NVIDIA shares will likely continue their tear. Despite that warning, the chipmaker still guided for almost 231% revenue growth to $20 billion in the fourth quarter, so it clearly isn’t all that worried.

Even if the stock doesn’t recover dramatically in the near term, NVIDIA’s long-term stock-price gains of 267% over the last three years, 1,184% over the last five, and 13,066% over the last 10 provide some level of safety over the long term. In fact, I would use any near-term pullbacks to add to the position.

What is the Price Target for NVDA Stock?

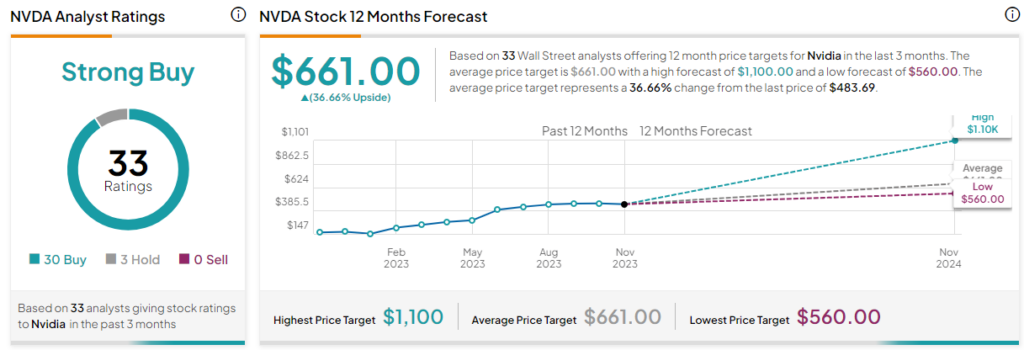

NVIDIA has a Strong Buy consensus rating based on 30 Buys, three Holds, and zero Sell ratings assigned over the last three months. At $660.39, the average NVIDIA stock price target implies upside potential of 36.7%.

Advanced Micro Devices (NASDAQ:AMD)

At a P/E of 1,120, Advanced Micro Devices has the opposite problem of NVIDIA. Its valuation has skyrocketed because it’s now barely profitable. However, the chipmaker certainly isn’t going anywhere anytime soon, so it’s only a matter of time before it bounces back. For now, though, a bearish view seems appropriate, pending a better entry price or improved earnings numbers.

In the third quarter, AMD reported $299 million in GAAP net income, although that was an improvement from net income of $66 million a year ago. On an adjusted basis, the company’s net income rose 4% year-over-year to $1.1 billion. AMD also reported revenue of $5.8 billion for the quarter, up from $5.6 billion a year ago.

Unfortunately, AMD continues to play catch-up to NVIDIA in the area of artificial intelligence, although management did reveal some progress on its last earnings call, announcing improvements in the company’s AI software capabilities through R&D and acquisitions. Management also expects the MI300 data center chip, which will support AI models, to be “the fastest product to ramp to $1 billion in sales in AMD history.” In short, AMD will likely catch up to NVIDIA at some point, but we’re not there yet.

What is the Price Target for AMD Stock?

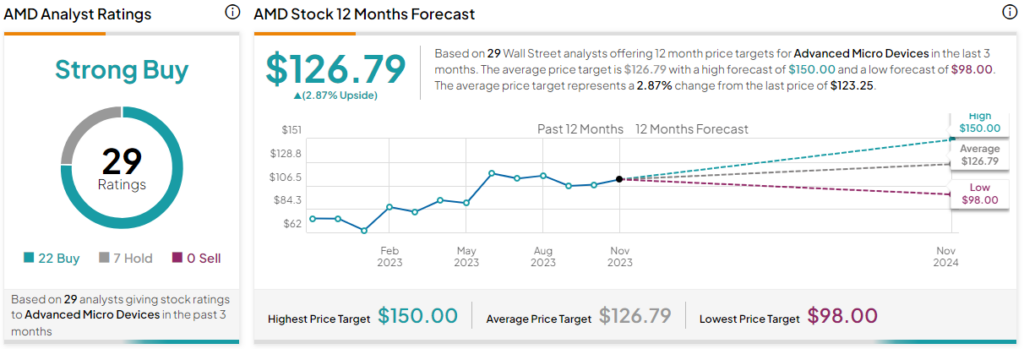

Advanced Micro Devices has a Strong Buy consensus rating based on 22 Buys, seven Holds, and zero Sell ratings assigned over the last three months. At $126.79, the average AMD stock price target implies upside potential of 2.9%.

Conclusion: Bullish on NVDA, Bearish on AMD

The battle between NVIDIA and Advanced Micro Devices has been going on for years, with one company pulling out in front of the other and then the other catching up and trading places. Nonetheless, neither of these companies is going anywhere anytime soon.

However, AMD could be playing catch-up to NVIDIA on AI for some time, calling for a wait-and-see approach. Meanwhile, NVIDIA will likely rerate higher once the market digests management’s warning about the new export restrictions.