The bears have been out in full force for Novavax (NVAX) this year and there has been little love in the current climate for this once high-flyer. Late for the Covid-19 vaccine party on account of manufacturing issues and beset by disappointing sales, sentiment has soured badly. All told, year-to-date, the shares have retreated by a massive 86% with the stock’s Covid-era triumphs well and truly gone.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

That said, not all are predicting doom and gloom for Novavax. Ahead of the Q3 print today, B. Riley analyst Mayank Mamtani thinks three key recent developments have the potential to alter the mood: “(1) FDA’s EUA granted to NVX-CoV2373 (Wuhan prototype) COVID-19 vaccine for use as a booster vaccine, broad enough in scope to be competitive to mRNAs (including the bivalent BA.4/5 format); (2) emerging dataset supportive of comparable immunogenicity delivered by prototype and updated bivalent vaccine constructs (mRNA) with some evidence indicative of perhaps better immune response profile of prototype vaccine, and (3) post-pandemic pricing leverage to COVID vaccine market, as recently substantiated by PFE’s commentary of raising price/dose to $110-130, ~4x the current contracted price with U.S. government.”

The mood can also improve significantly if in the wake of Q2’s disastrous showing and its downward revisions, Novavax can actually meet its new target in Q3. Considering that the $400 million of delayed EU revenue which led to the Q2 miss should be recognized in the quarter, Mamtani notes that in order to meet the lower end of the FY22 guide, an “incremental” ~25 million doses will need to be monetized in ex-US/Asia domains.

Mamtani believes the target is “achievable” as long as healthcare policymakers around the world continue to support regulatory bodies that have granted NVAX a broad booster label and remain dedicated to reducing the winter COVID spike by raising the booster rate. This partially depends on giving the public a different option in NVX-CoV2373 which is based on a conventional protein-based platform.

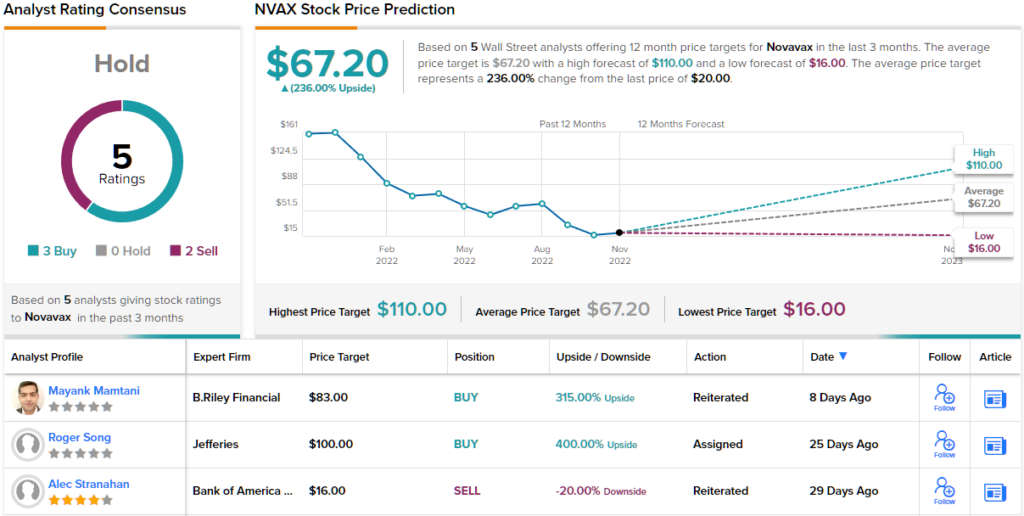

All told, Mamtani stays bullish on NVAX and sticks with a Buy rating and $83 price target, which makes room for 12-month gains of a hefty 315%. (To watch Mamtani’s track record, click here)

The Street’s overall take offers a bit of a conundrum; on the one hand, based on 3 Buys vs. 2 Sells, the stock receives a Hold consensus rating. However, those backing NVAX are a confident lot; at $67.20, the average price target represents upside of 246% from current levels. (See Novavax stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.