While David Ellison, the head of Skydance Media and son of Oracle co-founder Larry Ellison, has been linked to a possible Warner Bros. Discovery acquisition, another potential suitor has emerged.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Netflix (NASDAQ:NFLX) is reportedly considering a bid to acquire WBD, namely the film studio and streaming assets, rather than the entire company. This move would allow the streaming giant to expand its content library with established franchises like DC Studios, Harry Potter, and Looney Tunes. The acquisition could also provide access to HBO Originals, boosting Netflix’s competitive position in the streaming market.

Sizing up the idea, Bernstein analyst Laurent Yoon thinks Netflix “stands out as interesting.”

Yet having explored this scenario, the analyst sees it as unlikely, largely because it is unclear what strategic value the streaming giant would realize from the purchase. “That said,” Yoon goes on to add, “this industry is no stranger to head-scratching deals and/or valuations: AT&T/WarnerBros, Comcast/Sky, Amazon/MGM – the list goes on.”

While Yoon thinks bringing WBD into the fold could result in a short-term lift in engagement, he doesn’t expect it to be “sustainably material” over the long term. Netflix has steadily grown its content library over the years, but average engagement has stayed at roughly 60 minutes a user per day. This suggests the platform may be nearing a limit for general entertainment, meaning that simply adding more similar content is unlikely to drive meaningful growth. “The real opportunity lies in diversifying beyond general entertainment and legacy formats,” says Yoon.

On the subscriber front, Yoon thinks the growth potential is limited, as over 90% of HBO Max subscribers are already Netflix users (using the US as a proxy), and Netflix already enjoys strong penetration in other developed and growth markets where HBO Max plans to expand. While churn could improve with an even stronger content lineup, the upside is constrained given Netflix’s already best-in-class churn metrics.

What about the acquisition representing a defensive move? Any major MediaCo+WBD combination could present a long-term competitive threat to Netflix, especially if the merged entity is well-capitalized. However, any impact is likely to unfold over several years, leaving Netflix time to scale and diversify its offerings.

As for costs, while Yoon thinks there are clear “’no-brainer’” synergies to capture, such as corporate functions and a technology platform, he considers these as “check-the-box efficiencies rather than key drivers of the decision.”

Bottom line, Yoon is not entirely convinced. “While we see limited downside given WBD’s strong IP and studio assets, we also do not view it as a compelling acquisition for Netflix – whether in whole or just S&S down the line,” he summed up.

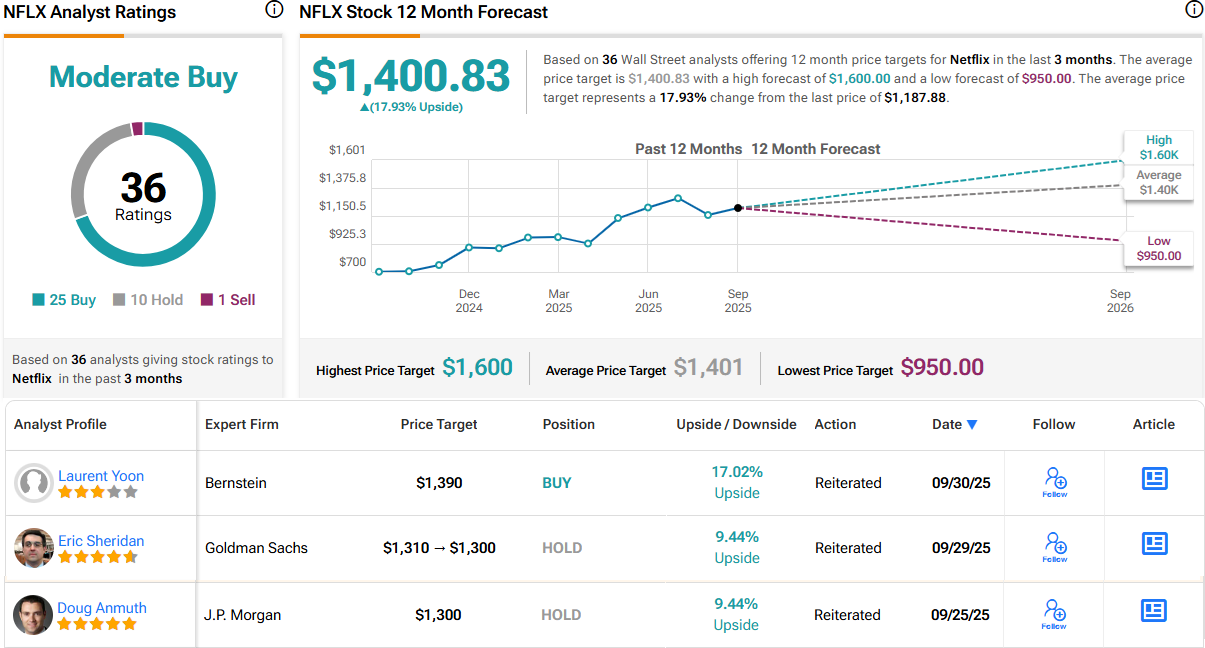

All told, Yoon reiterated an Outperform (i.e., Buy) rating on NFLX shares, backed by a $1,390 price target. There’s potential upside of 17% from current levels. (To watch Yoon’s track record, click here)

That target is only slightly lower than the Street’s average, which stands at $1,400.83 and factors in a one-year gain of 18%. On the rating front, the stock claims a Moderate Buy consensus view, based on a mix of 25 Buys, 10 Holds and 1 Sell. (See Netflix stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.