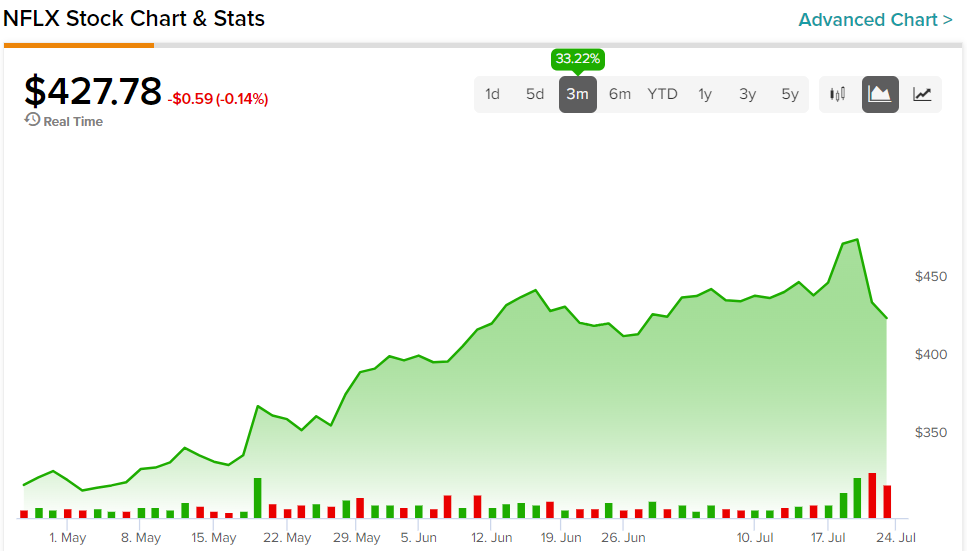

Netflix (NASDAQ:NFLX) stock corrected in the back half of last week despite reporting impressive growth in subscribers for its second quarter. Undoubtedly, the stock got ahead of itself after a 60% year-to-date surge. With the Hollywood actor and writer strike taking a toll on the broader basket of media and streaming firms, questions linger about how vicious the latest Netflix pullback will be.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Indeed, last week’s ugly reaction appears to be a case of a company running into a fairly high bar set for it going into a quarterly result. Though the Q2 numbers weren’t all that bad, the firm still came up short on the revenue front, with $8.2 billion, just shy of the $8.3 billion analyst estimate. This won’t cut it for a company trading at 45.6 times trailing price-to-earnings.

Further, shares of Netflix still seem expensive after the latest correction, as they’re in line with the already-high entertainment industry average of ~46 times. As momentum reverses course, I’m inclined to take on a neutral stance on the stock.

Netflix: The Easy Subscriber Gains are Already In

At this juncture, the easiest gains seem to have been made already, with the password-sharing (or freeloader) crackdown already helping the firm add nearly six million to its subscriber base in the latest quarter. Undoubtedly, that was a one-time move to bolster the subscriber base. From here, it gets harder to add subscribers while keeping operating expenses in check. The business of streaming content can get pretty expensive.

Encouragingly, the streaming juggernaut is still outperforming its top competitor Disney+ (NYSE:DIS), which is feeling the full force of media industry headwinds these days. Indeed, Netflix has proven that it’s still the top dog in the maturing streaming market. Also, although the stock has bucked the downward trend for the streamers, at least so far this year, I’m not sure how much longer the streamer can keep expanding its valuation multiple without another big strategic shift.

Even if Netflix remains the top dog for the long haul, it’s unclear as to how much profit potential the market holds as media firms continue to throw money at new content to beckon in new subscribers. It turns out it’s not so easy to dethrone Netflix. Now, the real question is whether it’s worthwhile to spend so much money to have a shot at the streamer, given the fairly muted state of the industry.

Netflix Must Embrace Tech to Justify Its Valuation

For Netflix to justify its valuation, which is well above most of its peers in the FAANG basket, the company needs to find other ways to keep its investors entertained. The rise of AI (artificial intelligence) and the Metaverse may be areas that Netflix could invest in. However, it’s still unclear which medium Netflix will find itself in around five years’ time.

Could we all be plugged into a VR or AR headset to view immersive spatial content developed by Netflix? It’s always a possibility. However, until management clears the air regarding its longer-term prospects, the stock may struggle to sustain the first-half rally.

At the same time, AI content is a wild card that could be a double-edged sword for Netflix and other Hollywood players. Undoubtedly, heavy use of AI could harm a film producer’s reputation among viewers and all workers in the industry. Even if AI is capable of generating impressive content, it may be difficult to procure certain human actors, writers, or directors who are so against the use of disruptive AIs in the movie business.

Fortunately, I do think Netflix won’t be joining the machines anytime soon. As such, I’d look for the company to steadily ease a toe into the AI waters, rather than seeking to replace people to drive down operating expenditures. At the end of the day, it’s the human touch that makes films and TV shows so special among viewers.

Is NFLX Stock a Buy, According to Analysts?

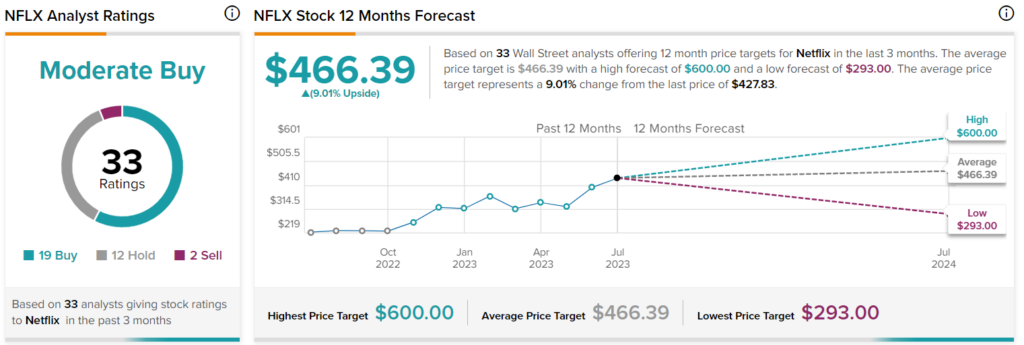

Turning to Wall Street, NFLX stock comes in as a Moderate Buy. Out of 32 analyst ratings, there are 18 Buys, 12 Holds, and two Sell recommendations. The average Netflix stock price target is $466.39, implying upside potential of 9%. Analyst price targets range from a low of $293.00 per share to a high of $600.00 per share.

The Bottom Line on Shares of NFLX

Netflix stock is unloved again after a glorious first-half rebound rally. As shares run out of steam on a pretty decent quarter, I wouldn’t look to buy the dip just yet. I think there’s a lack of growth catalysts for the name, and that alone could act as an overhang on the share price.