One of the biggest stories in markets today is the boom in AI – and with it, the surge in data center development. This trend extends far beyond the digital realm; data centers are massive physical structures, and their expansion has impacts in numerous industries.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

At the heart of this construction wave are the world’s largest tech firms, whose AI ambitions are driving unprecedented levels of capital spending. Companies such as Microsoft, Amazon, Meta, and Alphabet are pouring record amounts into data center construction to power their AI and cloud computing goals. Their combined spending reached about $245 billion last year and is now approaching $360 billion.

Data centers are extraordinarily power-hungry, consuming around 415 TWh last year, with forecasts from the International Energy Agency (IEA) suggesting that figure could reach 945 TWh by 2030, making them a central force behind rising global electricity demand. Much of that power goes toward cooling and climate control systems essential for maintaining stable operations.

Covering the energy sector for Needham, analyst Sean Milligan points to two lesser-known energy stocks that stand to gain as data centers multiply and the demand for reliable power infrastructure accelerates.

Do other analysts share his optimism? We turned to the TipRanks database to find out.

Generac Holdings (GNRC)

First up is Generac, a company that provides ‘total energy solutions,’ enabling people and businesses to personalize their energy use. More specifically, Generac provides energy technology and solutions, including power generation equipment, energy storage systems, energy management devices, and other specialized power products to a wide range of customers in the light commercial, industrial, and residential markets. The company has been in business since 1959, and today is a $10 billion-plus player in the power generation segment and a leader in North America’s generator market.

Generac’s power solutions have applications in several areas, including portable power, home backup, solar power storage, and EV charging. The common denominator is demand for either off-grid power or reliable backups to grid power; in every case, Generac’s products are designed to ensure that the essential electricity continues to flow under any conditions. The company conducts its sales under an array of brand names and boasts that it is the top name in home backup generators.

On the industrial side, Generac’s products support everything from microgrid local power supplies to specific industrial needs such as telecom, water infrastructure, and – of course – data centers. Reliable and sustainable power is necessary for data centers, and Generac provides a wide range of industrial-strength diesel-powered generators capable of meeting high power demands in the data center segment.

This company’s last set of financial results covered 2Q25 and showed a top line of $1.06 billion. This figure was up 6% year-over-year, and it beat the forecast by just under $35 million. Generac had a net income of $74 million in the quarter, or $1.25 per share in GAAP measures; this beat the forecast by 22 cents per share.

Needham’s Sean Milligan notes that Generac’s recent gains – the stock spiked as much as 29% in the days after the 2Q25 earnings release – are tied to the data center business and sees that as the key to the stock going forward.

“We think shares began trading on the data-center thematic after 2Q25 results (August 2025), when management publicly framed the $5B+ opportunity; we see further upside with execution (award announcements and pipeline-to-backlog conversion)… We see margin quality improving through 2026–2027 as data-center volumes ramp and the energy-technology drag eases… We assume $250MM of data-center revenue in 2026 at ~17.5% adjusted EBITDA, scaling toward a ~$500MM run-rate in 2027; lead times and service coverage are key differentiators. Data-center revenue could scale quickly, driving revenue and margin upside vs. our model,” Milligan opined.

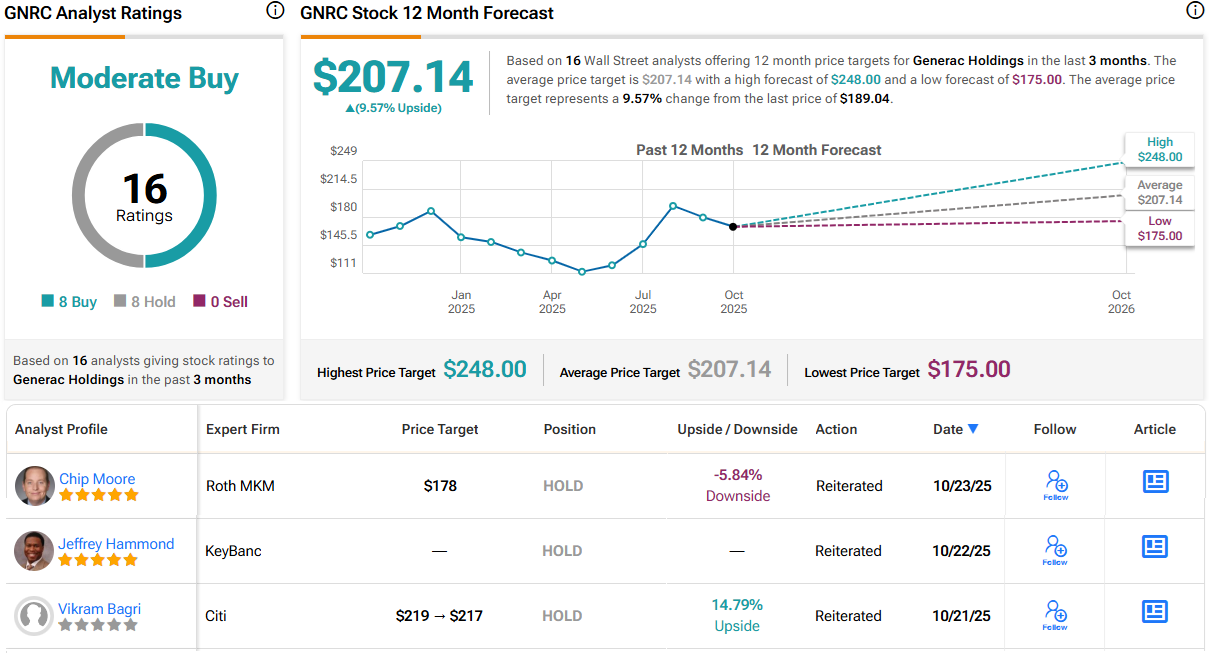

Quantifying this stance, the analyst puts a Buy rating on GNRC shares, along with a $248 price target that implies a potential upside for the year ahead of 31%. (To watch Milligan’s track record, click here)

Overall, Generac has earned a Moderate Buy consensus rating from the Street’s analysts, based on 16 recent reviews with a split of 8 Buys and Holds, each. The shares are priced at $189.04, and their $207.14 average target price suggests that the shares will gain 9.5% by this time next year. (See GNRC stock forecast)

Primoris Services (PRIM)

The next stock we’ll look at here is a specialty contractor company in the construction industry, a firm with a reputation for taking on difficult or challenging projects that its competition tries to avoid.

Primoris Services focuses on building sustainable infrastructure that supports the critical needs of the utility, energy, and renewable power sectors. The company operates in the US and Canadian markets, where it handles some of the most difficult construction projects. These include everything from gas processing and petrochemical plants, natural gas storage, fuel pipelines for everything from crude oil to natural gas liquids, and power generation facilities – and that list only scratches the surface.

The bulk of Primoris’ business is split into two large segments, Energy and Utility, but the company has an expanding Data Center segment as well that combines elements from the breadth of its business.

That capability includes planning, building, and connecting natural gas and solar power sources to the data center. Primoris can build gas power facilities, photovoltaic power installations, battery systems, and grid connections – and can design and install the maintenance and monitoring systems and piping and underground infrastructure vital to connecting the power systems to the data center. The company’s work in this area combines the latest in natural gas and renewable power technology with the ongoing data center boom.

This company’s revenues have been trending upward over the past two years – and in 2Q25 the firm recorded a solid quarterly performance. The top line in the quarter was up some 21% to reach $1.89 billion, and it beat the forecast by over $201 million. At the bottom line, Primoris realized a non-GAAP EPS of $1.68, a figure that was 60 cents per share better than had been anticipated.

This company’s potential for continued increases in revenue and earnings has caught the attention of Milligan, who writes in his coverage for Needham: “We see EPS compounding via top-line growth and operating leverage, with upside from transmission awards, simple-cycle gas wins, data center wins, and potential ‘inside-the-box’ data center expansion… PRIM is evaluating nearly $1.7B of work tied to data centers expected to be contracted by year-end and is already shortlisted/selected on ~$400–$500MM. While <10% of current revenue is directly tied to data centers, management sees multi-year opportunity across ‘outside-the-walls’ scopes (site prep, gen, T&D, fiber).”

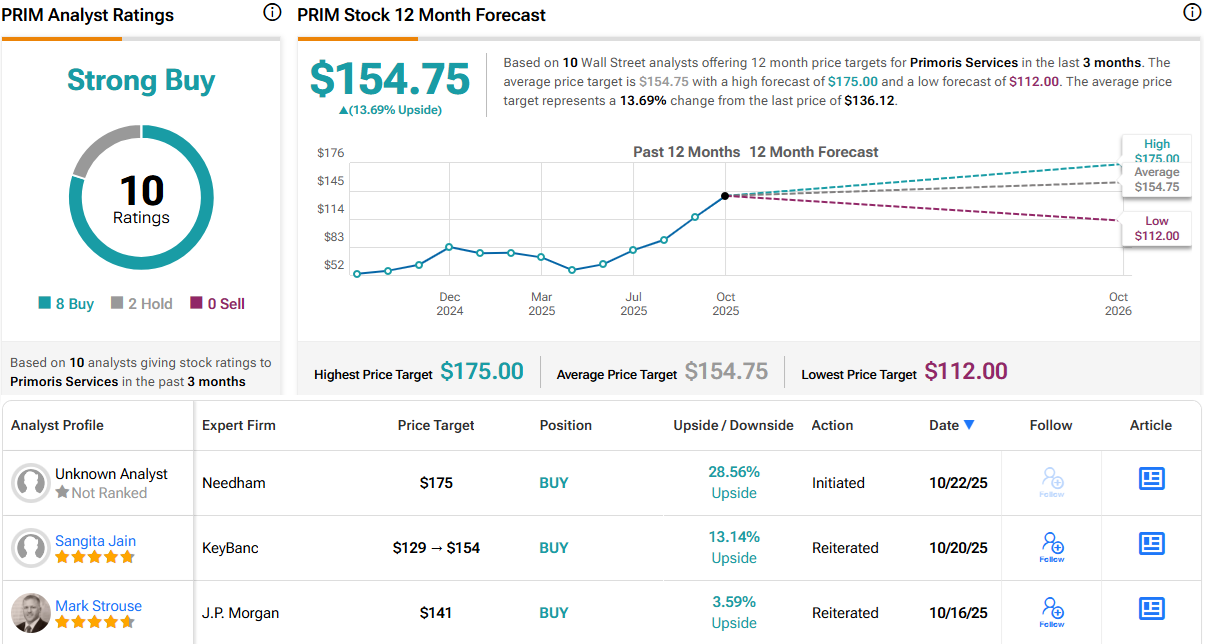

To this end, Milligan rates PRIM shares as a Buy, and his $175 price target points toward a gain of 28.5% on the one-year horizon.

All in all, PRIM holds a Strong Buy consensus rating from the analysts, based on 10 ratings that break down 8 to 2 in favor of Buy over Hold. The stock is currently trading for $136.12 and has an average target price of $154.75, a combination that supports a 14% upside potential over the next 12 months. (See PRIM stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.