After several years of enormous real-world growth reflected in the stock’s ascent, NVIDIA’s (NVDA) 2022 has been a rather different affair. A sharp drop in gaming sales, softness in the data center business and the constraints put on the exports of state-of-the-art data center chips to China have all been issues the company has had to contend with.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The result has been a stock that has shaved 44% off its value, a worse showing than the SOX’s (the major semiconductor index) 33% drop.

But with 2023 now clearly in view, Needham analyst Rajvindra Gill thinks it’s time to look at the chip giant in a new light. In fact, heading into the new year, such is Gill’s confidence in a turnaound, he has designated Nvidia with ‘Top Pick’ status.

Explaining his stance, the 5-star analyst said, “As we exit one of the semiconductor industry’s most volatile years, investors should focus on companies where both the consensus estimates and the end-markets have largely corrected.”

And for Nvidia, they most certainly have. The graphics segment has dropped ~30% year-over-year, while China data center has fallen at a similar rate.

Yet, Gill thinks we are “approaching a bottom in the gaming segment” in C1Q23. And while the analyst thinks volatility could indeed be in the cards for the overall data center market next year, he believes NVDA’s clients are “upgrading to the latest H100 architecture.”

As for EPS consensus estimates, for CY23, these have come down by 31% over the past year, with “underutilization” also negatively impacting them. “NVIDIA took large inventory charges ($1.22BN in F2Q and $702MM in F3Q) related to the weaker gaming and crypto outlook,” Gill noted. “That headwind could abate and reflect higher margins not currently built into estimates.” There’s also been a 20% drop in CY23 sales estimates.

But based on the “transition to AI workloads and the adoption of new products (H100, Grace, Thor etc.),” Gill is expecting growth to accelerate in CY23 and CY24 and this sets up the company nicely.

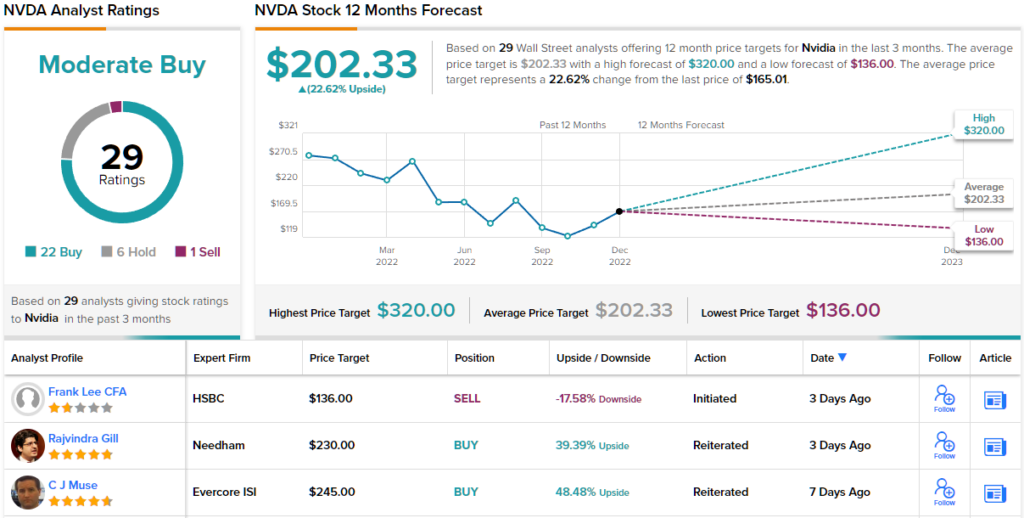

With this in mind, Gill bumped his price target on NVDA from $200 to $230, making room for 12-month returns of 39%. The 5-star analyst’s rating stays a Buy. (To watch Gill’s track record, click here)

Most other Street analysts remain in NVDA’s corner; based on 22 Buys, 6 Holds and 1 Sell, the stock claims a Moderate Buy consensus rating. Investors will be sitting on returns of ~23%, should the $202.33 average target be met a year from now. (See Nvidia stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.