Monday’s Update: UBS has agreed to purchase Credit Suisse for $3.3B in an all-equity deal backed by government guarantees and liquidity provisions.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

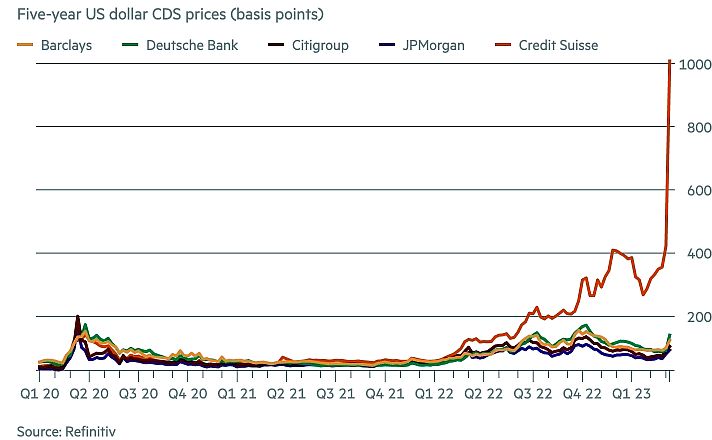

Last week, Europe’s banking stocks suffered their biggest drop in a year as Credit Suisse (NYCE:CS) shares tumbled so much, that at some point markets feared it might collapse. After years of steady decline, marked by a series of scandals and mismanagement issues, CS was the natural victim of a market rout, ignited by the failure of two niche U.S. banks. Push came to a shove after Credit Suisse’s main shareholder, Saudi National Bank, said it would not invest any more money in CS. The news spooked investors, who already felt uneasy about the lender, and pushed its shares down to a record low in the bank’s 167-year history.

Eventually, the Swiss central bank was forced to provide Credit Suisse with a $54 billion in a liquidity backstop to help revive investor confidence; although twice smaller than it was before the 2008 crisis, the bank is still too big to fail. However, the liquidity injection didn’t help quell markets anxiety about what was supposed to be safe, well, as a Swiss bank. CS stock continued to decline, stoking fears of a global banking crisis. JPMorgan (NYCE:JPM) assessed that CS’s loss of investor confidence prevents its future existence as an independent financial institution; outflows from the troubled lender reached over $10 billion a day, raising worries that the bank would become insolvent within a week.

During the weekend, Swiss officials have been scrambling to arrange for CS to be taken over by UBS (NYCE:UBS), Switzerland’s largest bank, in effort to restore confidence and stability. However, forced weddings aren’t bankers’ favorite pastime, and UBS seemed to be reluctant from the beginning to mar its relatively good record with CS’s indecent reputation, scarred with money-laundering convictions, fraud, holding accounts of criminals and dictators, corporate espionage fines, bad investment decisions and management churn. UBS is financially robust, especially compared to that of CS: it has $1.1 trillion in total assets, more than twice the assets of CS, and has reported a $7.6 billion net profit in 2022, while Credit Suisse posted a $7.9 billion net loss.

Besides, to save Credit Suisse from collapsing (and to save Europe’s already weakened banking system from imminent disaster that would follow such collapse), the deal would have to be closed in a number of days. This would work out perfectly for a small company or even a small bank, but it’s hard to see such a breakneck speed when the entity concerned is among the world’s largest wealth managers and is one of 30 global systemically important banks.

UBS Agrees to Buy Credit Suisse

Eventually UBS agreed to a deal, offering to buy Credit Suisse for $1 billion, a fraction of its value. CS’ market value stood at $8 billion this past Friday, after its stock lost over 75% year-to-date – so the $1 billion price tag would all but wipe out CS’s shareholders. UBS also demanded extensive guarantees and backstops to cover future risks and asking the Swiss government for a pledge to take on potential losses from the deal.

The largest Swiss lender also insists that if CS’s credit default swaps (a price of an “insurance” against default) rise by 100 bps or more after the deal is signed, it would void the contract. Although an instant scale-up of assets and operations could be beneficial for UBS, it would be taking on large unknown costs and the complexities of integration, in addition to other risks, such as customers taking their money elsewhere for diversification reasons.

The current draft of the acquisition outlines a 100% takeover of Credit Suisse; however, UBS is said to plan a dramatic downsizing of the fallen giant, keeping only parts that fill gaps in UBS’s geographical or business areas. Besides, if the acquisition were to come through, Swiss authorities expected to change country’s law to bypass UBS shareholder vote, which is seen by many as poor corporate governance and has drawn antagonism towards the deal. Credit Suisse was reported to protest at the deal because it believes the offer is too low and would hurt shareholders and employees of the bank; CS’s largest shareholder, Saudi National Bank, have backed the bank’s opinion. However, other options for the future of CS may be even worse for shareholders of the “Schrödinger’s Cat” of finance, unknown to be alive or dead before the markets open on Monday.

As the window of opportunity closes by the second, Swiss authorities are now weighing either full or partial nationalization of Credit Suisse as a backup option if a UBS deal isn’t closed before it’s too late. This is an uneasy decision to make for any regulator, and especially for the Swiss, who have been proud bankers of the world for many decades. But now, they have to decide whether they wipe out the shareholders and damage their country’s financial reputation or risk a full-blown financial crisis not only in Switzerland, but in Europe – and, probably, the whole world.