Michael Wilson, Morgan Stanley chief equity strategist, has been among the most prominent of the bearish prognosticators this past year, and while he still sees rough times ahead, he also offers some hope for the long term.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

At base, Wilson says the S&P 500 is likely to sink another 20% before hitting a bottom near 3,100 during 1Q23. The index slipped into a bear market in June of this year, when the Federal Reserve began its aggressive anti-inflationary interest rate hikes, and has been on a volatile ride ever since. Wilson believes that volatility will only increase as we head closer to the end of the current bear.

“You’re going to make a new low some time in the first quarter, and that will be a terrific buying opportunity,” Wilson opined. “Because by the time we get to the end of next year, we’ll be looking at 2024, when the earnings will actually be accelerating again.”

Meanwhile, Wilson’s analyst colleagues at Morgan Stanley have pointed out two stocks that are already in the ‘buy’ zone. These are equities that have been flirting with their own bottom levels lately, but retain Buy ratings from the analysts – and offer solid upside potential going forward. We’ve opened the TipRanks database to see if there’s agreement regarding these names in the wider analyst community. Let’s take a closer look.

L3Harris Technologies, Inc. (LHX)

The first Morgan Stanley pick we’ll look at is L3Harris, a $39 billion defense contractor agency, whose modern incarnation represents the 2019 merger of L3 Technologies and Harris Corporation. L3Harris offers a range of technological solutions for the defense industry, including important contribution in the vital missile warning and defense segment. The company also offers products valuable in command and control, ISR and SIGINT, and electronic warfare. The company saw more than $17.8 billion in revenues last year, and is active in more than 100 countries around the world.

In the most recent reported quarter, 3Q22, L3Harris had a top line revenue total of $4.2 billion, a flat result year-over-year. On the bottom line, the company reported a net loss of $1.56 per share – this reflected a one-time goodwill impairment charge of $4.16 per share. By non-GAAP measures, L3Harris had a 3Q EPS of $3.26, up a modest 1.5% year-over-year, but missing consensus estimates of $3.39.

Dividend-minded investors should note that L3Harris had a Q3 operating cash flow of $588 million, which included $546 million in adjusted free cash flow. This strong cash position allowed the firm to return $386 million to shareholders through a combination of buybacks and dividends. The current dividend is set at $1.12 per common share, or $4.48 annualized, and delivers a return of 2.2%.

L3Harris has recently been making active moves to expand its position in the industry through two acquisitions. The first was the purchase, in a transaction worth $1.96 billion, of Viasat’s Tactical Data Link products, known as Link 16. This purchase received regulatory clearance earlier this week. The second acquisition was the outright buy of Aerojet Rocketdyne (AJRD) in an all-cash move totaling $4.7 billion. The AJRD purchase indicates that L3Harris is intent on maintaining its ability to deliver mission-critical capabilities in the missile segment.

On the trading side, L3Harris shares have lost 17% over the past two months. What this comes down to, is a stock that investors need to pay more attention to – in the view of Morgan Stanley analyst Kristine Liwag.

“We see LHX as the new tactical value play entering 2023,” Liwag noted. “The stock has lagged both Defense peers and the S&P QTD… We see this relative underperformance driven by the company’s 3Q22 earnings miss, lowered 2022 outlook and more cautious take on 2023. The stock price has since reached levels, in our view, that are too attractive to ignore and we expect LHX to narrow the valuation gap vis-à-vis Defense peers.”

Going into some detail on the recent AJRD acquisition, Liwag adds, “We view this deal as strategic in nature, offering LHX the ability to expand its footprint in missiles and space endmarkets, which we see as some of the fastest growing segments of the DoD budget.”

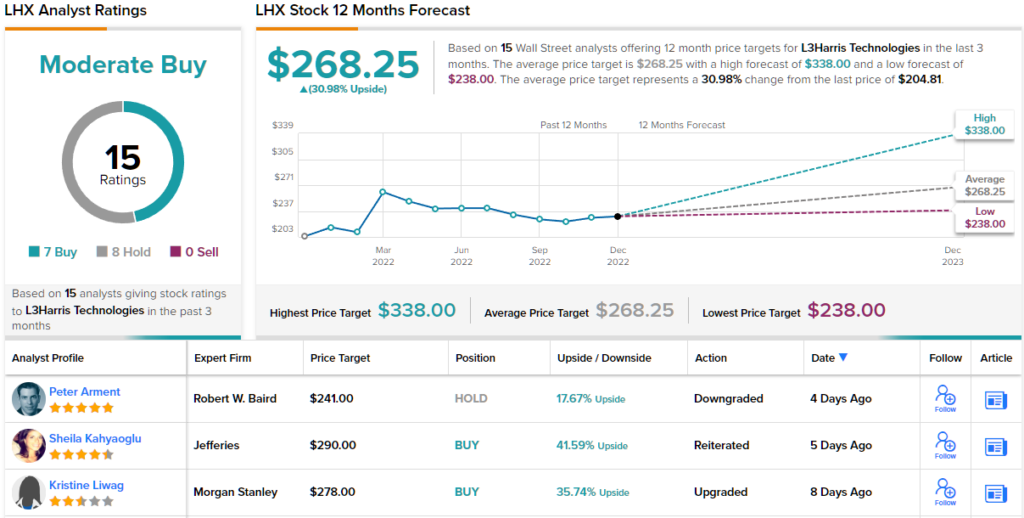

Liwag’s comments back up her Overweight (i.e. Buy) rating on the shares, and her price target of $278 implies ~36% upside for the stock over the coming year. (To watch Liwag’s track record, click here)

Overall, this defense contractor holds a Moderate Buy rating from the analyst consensus, based on 15 recent reviews which include 7 Buys and 8 Holds. The shares are trading for $204.81, and their $268.25 average price target suggests 12-month gains of ~31% from that level. (See LHX stock forecast on TipRanks)

RingCentral, Inc. (RNG)

Next up, RingCentral, is a communications tech company whose software packages offer solutions to the wide range of communications issues faced in the modern business office. At base, RingCentral’s products allow for users to route phone lines, video calling, screen sharing, call forwarding, and most other telecom features through the office’s centralized computer server, making it easier to manage business telecommunications. In addition, RingCentral’s packages are compatible numerous popular office applications, such as Outlook, Salesforce, and Google Docs, and are available on desktop computers as well as handheld tablet and smartphone devices.

RingCentral saw its shares surge during the pandemic and lockdown periods of 2020, when forced work-from-home put a premium value on business communication systems – and investors, seeking any silver lining at the time, pushed the stock prices up and up. Since then, however, the return to a more normal operating environment has shown that many of these companies are now facing the consequences of overinflated share prices and their recent overextended spending. RNG shares, in that context, are down 82% this year.

Even though the company’s shares are down, RingCentral has continued to see gains this year at both the top and bottom lines. In the last quarter reported, 3Q22, RNG had total revenues of $509 million, up 23% year-over-year. At the bottom line, the company’s non-GAAP diluted EPS was reported as 55 cents, up 52% from the 36 cents shown in the year-ago period. Both the revenue and earnings figures beat the forecasts. The wins were driven by a strong increase in ARR (annualized recurring revenue), which rose 25% y/y to reach $2.05 billion.

Morgan Stanley analyst Meta Marshall, in her coverage of RingCentral, is cognizant of the company’s long share price decline 2022, but sees ‘near term upside.’

“We think the market is missing an opportunity as free cash flow from the company improves. RNG is currently trading at <2x24e Revenue and ~11x24e P/E, well below software peers. We appreciate the bear cases on RNG. However, at current levels we think RNG’s valuation is reflecting more bear case scenarios on the top line and ignoring cash flow potential,” Marshall explained.

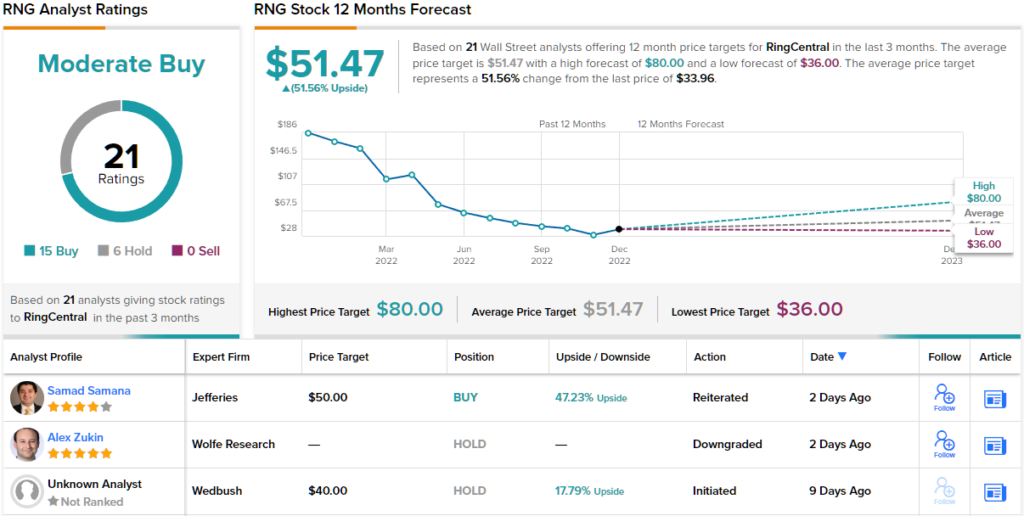

Quantifying RingCentral’s prospects, Marshall rates the stock an Overweight (i.e. Buy), with a $50 price target that indicates her confidence in a 47% upside by this time next year. (To watch Marshall’s track record, click here)

Tech-oriented companies are known for attracting plenty of Wall Street analyst attention, and RingCentral has no fewer than 21 recent analyst reviews on record. They break down 15 to 6 in favor of the Buys over Holds, for a Moderate Buy analyst consensus view. The shares boast an average price target of $51.47, which implies ~52% one-year gain from the current trading price of $33.96. (See RNG stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.