For most of this year, the bears have been out in force – the S&P hit a 52-week intraday low on October 12, when the index dipped below 3,500. Since then, we seen something of a rally, and the index is up 7%. The question now is, will the rally hold or do the markets have more room to fall?

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

There may be no simple answer to that one. Inflation remains far too high, despite the Fed’s rapid shift toward increasing interest rates. Most pundits see the central bank continuing with rate hikes into the first quarter of next year, which may rein in the rate of inflation but may also tip the economy into recession.

But Michael Wilson, equity strategist from Morgan Stanley, is mixing some hope into the forecast. Wilson has been among the most prominent of the bearish prognosticators this past year, and while he does not see a sea-change coming for the markets, he does believe that investors have a window of 6 to 8 months to ride a bear-market rally, and engage in some profitable trading.

“We think ultimately the bear market will be over probably sometime in the first quarter [of next year]… All of this is subject to revision… We’re probably more bearish than most for the outlook next year. But we do think this tactical rally is going to be big enough to try and pivot and trade it,” Wilson told Bloomberg.

Wilson’s colleagues among the Morgan Stanley stock analysts are running with that view, and picking out the stocks they see offering high potential for 2023. In their view, investors can find possible gains if they look in the right places. We’ve used the TipRanks platform to pull up details on two of these picks.

HubSpot, Inc. (HUBS)

We’ll start in the digital world. HubSpot, since its 2006 founding, has become one of the better-known names in online inbound marketing, and has built up a reputation for innovation. HubSpot caters to CRM experts, SEO optimizers, content managers, and social media marketers with a range of web analytic products. These are offered on the freemium model, with basic services given free of charge and subscription upgrades available for customers who need higher-level options. HubSpot currently boasts over 150,000 customers, and operates in more than 120 countries. The customer base expanded by 25% between June 30, 2021 and June 30, 2022.

HUBS has fallen 58% so far this year, badly underperforming the broader markets. Shares in HubSpot are down even though the company remained profitable through the COVID pandemic and has recorded 8 consecutive quarters of sequential revenue growth.

In the last quarter reported, 2Q22, HubSpot had a top line of $421.8 million, up 36% year-over-year. This was accompanied by a non-GAAP net income of $22.4 million, or 44 cents per diluted share. The non-GAAP earnings were about flat year-over-year.

Q2 saw the company generate $40.9 million in cash from operations, along with $22.4 million in free cash flow. On the balance sheet, HubSpot reported having $1.4 billion in cash on hand as of June 30.

This company has attracted the attention of Morgan Stanley’s 5-star analyst Keith Weiss, who writes of it, “While acknowledging near-term headwinds, we view HubSpot as attractively valued, well positioned to weather a softening demand environment near term and competitively advantaged in the long term as incremental focus on efficiency drives consolidation to platform solutions and multi-hub adoption at HubSpot.”

To this end, Weiss rates HUBS shares an Overweight (i.e. Buy). In his view, the stock justifies a price target of $378, suggesting an upside of 34% in the next 12 months. (To watch Weiss’s track record, click here)

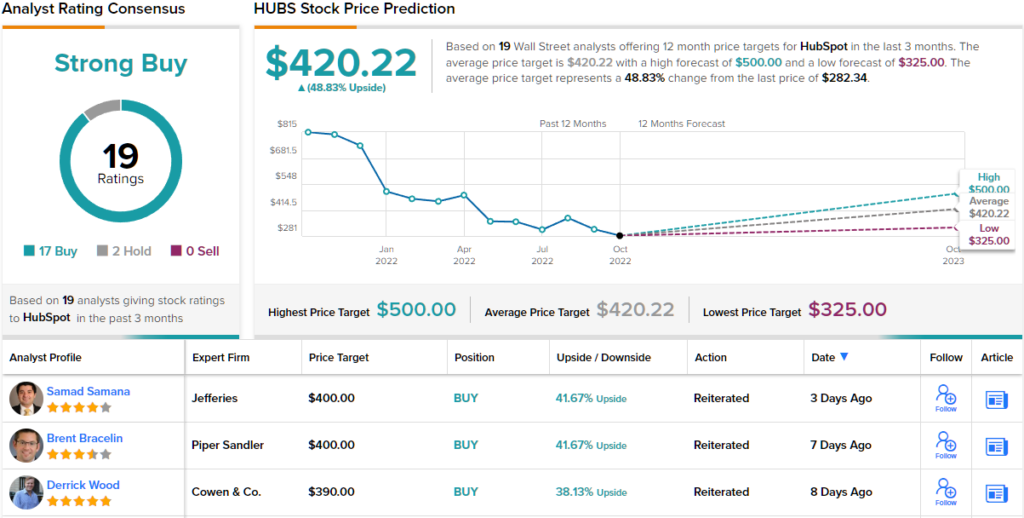

There’s no doubt that the bulls are running for HubSpot as the 19 recent analyst reviews include 17 Buys against just 2 Holds, for a solid Strong Buy consensus rating. The stock is selling for $282.34 and its average price target, now at $420.22, is even more bullish than Morgan Stanley’s Weiss allows, and implies a ~49% gain over the next year. (See HUBS stock forecast on TipRanks)

Bridge Investment Group (BRDG)

Next up is Bridge Investment Group, a company in the real estate investment trust (REIT) niche. Bridge bills itself as a ‘vertically integrated real estate investment manager,’ and currently has a diversified portfolio composed of real estate-backed credit, industrial net-leased real estate properties, logistics properties, office space, and residential properties. These various properties include 52,350 multifamily housing units, 10,750 senior housing units, and some 12.9 million square feet of leasable office space. The company has approximately $42 billion in total assets under management, and boasts a market cap of $2.3 billion.

Bridge last reported quarterly results for 2Q22, and showed total quarterly revenue of $99 million, with investment income of $104.9 million. These figures were up year-over-year, by 38% and 31%, respectively. Bridge’s net income for Q2 came to $124.4 million, and was up 50% from 2Q21. And in a metric of particular interest to return-minded investors, Bridge showed a distributable income of $54.6 million. This came to 32 cents per share, and was up 28% from the year before.

The distributable income easily covered the company’s common share dividend, which was paid out in September at 30 cents per share. With an annualized rate of $1.20, the common stock dividend is currently yielding a strong 8%. This is 4x higher than the average dividend yield found among S&P-listed companies. Even better, the dividend yield almost matches the current rate of inflation, providing a strong defensive attribute for investors.

5-star analyst Michael Cyprys, in his coverage of this stock for Morgan Stanley, takes a bullish view, noting: “We view BRDG as a secular growth story with inflation protection given exposure to attractive real estate end markets with skew to housing (~80% of the book) that benefits from shortage of housing supply in the US and ability to pass through rising inflation with higher rents that support strong fund performance, as well as asset and earnings growth.”

Cyprys goes on to give BRDG shares an Overweight (i.e. Buy) rating, and a price target of $21 that implies a 40% share gain over the coming months. (To watch Cyprys’ track record, click here)

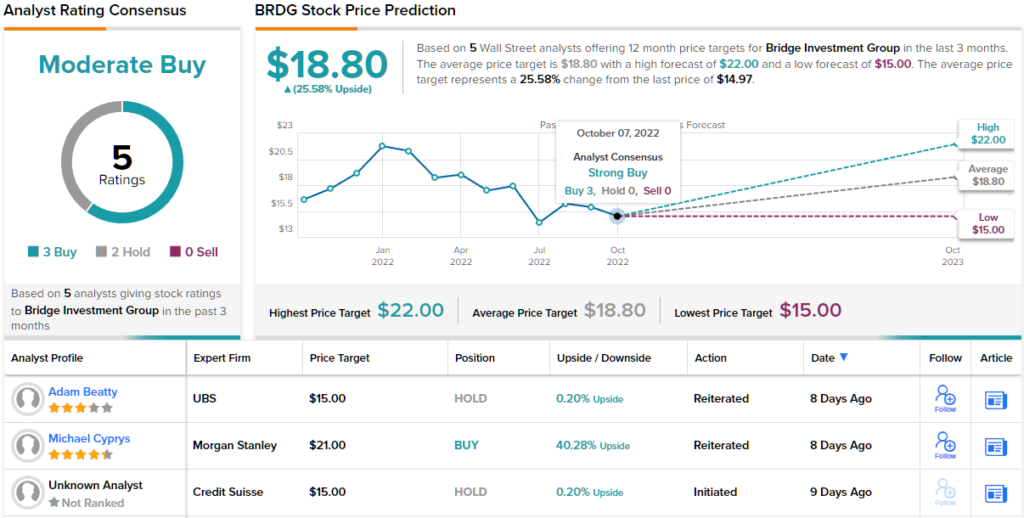

Overall, Bridge has attracted coverage from 5 Wall Street analysts recently; their reviews include 3 Buys and 2 Holds for a Moderate Buy consensus rating. The stock is currently trading for $14.97 and its $18.80 average price target suggests it has a one-year gain of ~26% ahead of it. (See BRDG stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.