Markets move in cycles, experiencing ups and downs that are influenced by various conditions, ranging from inflation rates to consumer sentiment. The key to successful investing is to track these shifts, avoid the black swans, and build a portfolio that can consistently generate returns. Dividend stocks, with their steady passive income stream, make a sound addition to such an investment strategy.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

According to Morgan Stanley’s outlook, a recession is expected to occur this year, making dividend stocks more attractive than ever. They’re a classic defensive play, ensuring a return even if markets go south. And that downward turn is looking more likely, according to Morgan Stanley strategist Mike Wilson.

“If this new inflationary regime mirrors the post-WWII period, it will be volatile with significant cyclical ups and downs that should be traded if one wants to fully capture excess returns in this new regime. In short, the boom/bust period that began in 2020 is currently in the bust part of the earnings cycle — a dynamic that’s not yet priced, in our view,” Wilson opined.

Taking this into consideration, Morgan Stanley analysts have pinpointed two dividend payers with impressive yields of up to 11%, potentially providing a solid source of passive income for investors. Let’s take a closer look.

Equitrans Midstream (ETRN)

We’ll start with Equitrans, an energy company that operates in the midstream segment. This segment is a vital part of the energy industry as midstream companies are responsible for transporting hydrocarbon products from wellheads to storage, refineries, and distribution points. Equitrans, which spun off from EQT in 2018, is one of the largest natural gas gathering companies in North America. The firm’s network includes assets for gathering and transmitting natural gas, as well as water transport pipelines, in the gas plays of the Appalachian Mountains, particularly in the region where Pennsylvania, West Virginia, and Ohio meet.

By the numbers, Equitrans operates more than 1,180 miles of high-pressure gathering lines, 950 miles of interstate transmission pipelines, and 200 miles of water pipelines; overall, Equitrans has a 4.4bcf natural gas transmission capacity.

The company received a dose of good news early this month, when the debt ceiling legislation was signed. The bill, in its final form, included authorization and Federal funding for Equitrans’ Mountain Valley Pipeline (MVP) project. This pipeline is planned for completion by year’s end, at a total cost of $6.6 billion.

In the company’s 1Q23 results, reported last month, Equitrans showed a top line of $376.34 million. This was up 10% year-over-year, and came in $15.6 million ahead of expectations. At the bottom line, the company reported a non-GAAP earnings per share of 22 cents, a total that compared favorably to the 14-cent EPS from the prior year quarter and was 10 cents per share better than the forecast.

Of interest to dividend investors, Equitrans has been successful at generating cash. The company’s cash from operations came in at $224.7 million, up from $185.9 million in 1Q22, and the free cash flow of $94.2 million expanded 300% y/y from the $23.5 million in the year-ago quarter. The strong cash flows support the company’s dividend payments.

Equitrans paid out its last declared dividend on May 15. That payment was sent out at 15 cents per common share, or 60 cents annualized. The annualized rate gives a yield of 6.3%.

Covering this stock for Morgan Stanley, 5-star analyst Devin McDermott sees plenty of potential for investors to grab onto.

“ETRN continues to trade below its fair value, in our view. Realization of fair value will likely be tied to (1) completion of the project to fully de-risk investor concerns, (2) deleveraging progress and management communication of capital allocation priorities, and (3) articulation of strategy and drivers of shareholder value creation following a prolonged period of focus on the outcome of MVP,” McDermott wrote.

McDermott adds an Overweight (i.e. Buy) rating to his commentary, and completes his stance with a $14 price target, indicating his confidence in an upside of ~49% for the next 12 months. Based on the current dividend yield and the expected price appreciation, the stock has ~55% potential total return profile. (To watch McDermott’s track record, click here)

While McDermott represents the bullish view, Wall Street is somewhat divided on this stock, as shown by the 9 recent analyst reviews. These break down to 3 Buys, 5 Holds, and 1 Sell, resulting in a Hold consensus rating. Shares in ETRN are trading at $9.42, and the average price target of $9.66 suggests a nominal gain of 2.55% within a one-year time frame. (See ETRN stock forecast)

Petroleo Brasileiro (PBR)

For the second high-yield dividend stock, we’ll turn our attention south of the border – all the way down to Brazil, the largest country in South America and home to Petróleo Brasileiro, or Petrobras, one of the world’s major oil companies. Petrobras had its start as a state-owned firm, and today the Brazilian government still directly owns just over 50% of the company’s publicly traded shares.

Looking at some raw numbers, we find that Petrobras boasts more than 5,000 oil and gas production wells, and proven hydrocarbon reserves of 9.878 billion barrels of oil equivalent, and the company’s daily production output stands near 2.77 million barrels of oil equivalent per day. In addition to producing oil and gas, Petrobras also operates 12 refineries, with an output of more than 1.85 million barrels per day of oil products.

Petrobras has a strong position in the midstream segment, as well as in production. The company controls more than 7,700 kilometers of oil pipelines, and another 9,100 kilometers of natural gas pipelines. In addition, the firm owns or charters over 120 tanker vessels.

All of this easily places Petrobras among the ranks of the world’s first-tier oil companies. In terms of US currency, Petrobras generated $26.77 billion in total revenue during 1Q23, resulting in a gross profit of $14.11 billion. These figures represented a 1.5% and 2.5% year-over-year decline, respectively, with the top-line number falling short of the forecast by $1.08 billion. At the bottom line, Petrobras reported a GAAP EPS of $1.12, surpassing expectations by 23 cents.

The company saw a small y/y increase in net cash from operations, which grew from $10.31 billion to $10.35 billion. The free cash flow slipped one-tenth of a percent y/y, to $7.92 billion.

On the dividend, Petrobras currently pays out some 38.16 cents per American Depositary Share each quarter. Calculating forward, this annualizes to just under $1.53 per ADS and yields 11.55%.

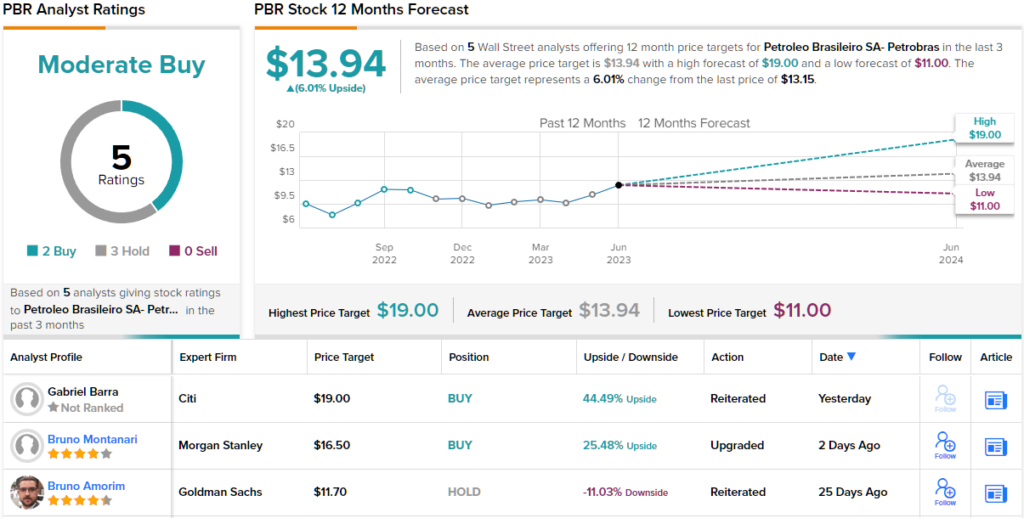

Morgan Stanley’s Bruno Montanari sees this company with plenty of potential to increase that yield, as he explains: “Policy changes thus far have been far less disruptive than initially expected, and lower oil prices and a stronger BRL contributed to the defensive nature of the stock. Our new estimates, using lower oil prices form the current forward curve, have PBR still generating FCF of $23B in 2023, a 30% yield. And our new dividend expectation, at 40% of FCF (before interest), generates a compelling 16% yield.”

To this end, Montanari gives Petroleo shares an Overweight (i.e. Buy) rating and his $16.50 price target, implies a potential one-year upside of 25% in the coming year. (To watch Montanari’s track record, click here)

Tuning now to the rest of the Street, where based on an additional 2 Buys and 3 Holds, this stock claims a Moderate Buy consensus rating. The shares are selling for $13.15 and the $13.94 average price target suggests a one-year gain of 6%. (See Petrobras stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.