Microsoft (NASDAQ:MSFT) beat expectations on both the top and bottom line in its latest quarterly readout, but that was not enough to stave off the bears who latched onto other issues and sent shares down 4% in Wednesday’s trading session.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

In the fiscal fourth quarter of 2023 (June quarter), the tech giant delivered revenues of $56.2 billion, amounting to an 8.3% year-over-year increase and beating the Street’s call by $710 million. On the other end of the equation, the company recorded EPS of $2.69, convincingly ahead of the $2.55 expected on Wall Street.

But there were evidently bits that rankled. Cloud service Azure’s revenue showed a bit of slowdown, increasing by 26% y/y vs. the 27% growth notched in the previous quarter, and although that figure beat expectations of 25% growth, it was not to the extent some bulls were hoping for.

The company also intends to spend heavily on its AI endeavors. Moreover, the revenue guide came in below expectations. Impacted by a weak outlook for its PC business, for F1Q, the company sees revenues hitting the range between $53.8 billion to $54.8 billion. At the midpoint, that is below the $54.94 billion the analysts were looking for.

With AI pushing the narrative and Microsoft in the driver’s seat, perhaps expectations were a bit too high heading into the print. In any case, Morgan Stanley analyst Keith Weiss thinks investors might “bristle over a lack of hand-holding into FY24,” yet he is no less convinced the company remains the “long-term leader in AI.”

“While the excitement of Microsoft’s solid positioning for Generative AI was clearly palatable in management’s commentary and the expectations for ramping capex growth to support this demand, the lack of direct commentary on FY24 revenue growth left some investors wondering what they’re missing,” the 5-star analyst said. “Our view, the consternation likely proves to be much ado about nothing, as the scope of Microsoft’s forward FY24 guidance has been volatile in the past and following the management’s bread crumbs through the conference call leads to an equation of expanding share gains, accelerating revenue growth and solid EPS upside ahead.”

With an outlook like that, it should be no surprise that Weiss sides with the bulls on MSFT. His comments come with an Overweight (i.e. Buy) rating, and a $415 price target that indicates potential for 21% share growth on the one-year time horizon. (To watch Weiss’s track record, click here)

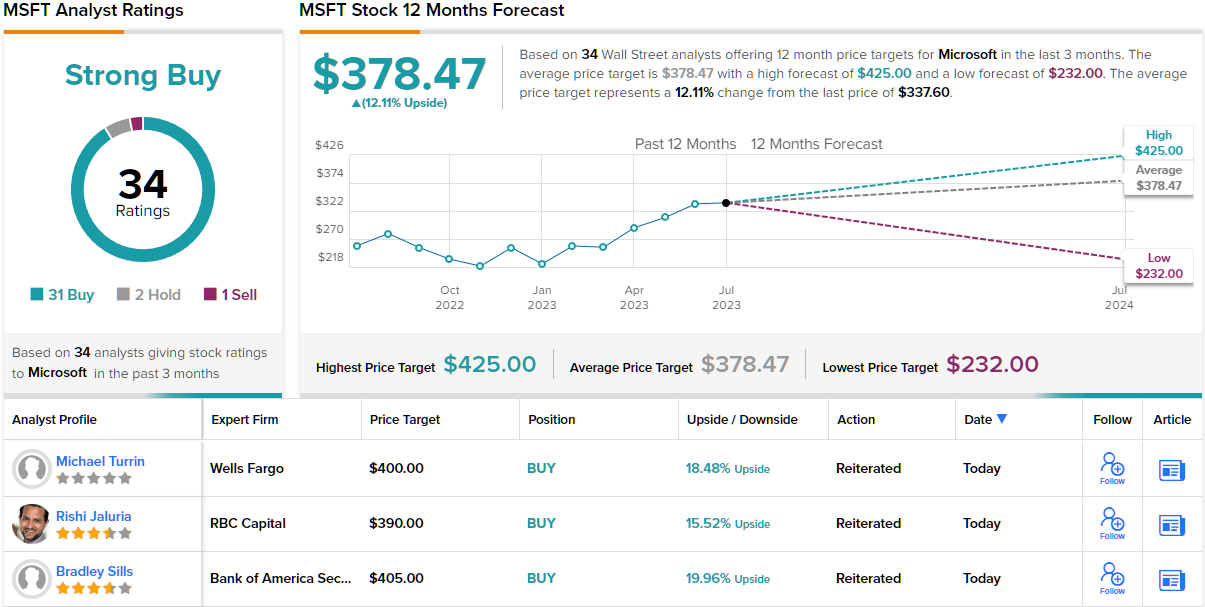

The rest of the Street also remains in MSFT’s corner. The stock gets a Strong Buy consensus rating, based on 31 Buys vs. 2 Holds and 1 Sell. At $378.47, the average target makes room for 12-month returns of 11%. (See Microsoft stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.