While the Fed eventually applied an almost unheard-of aggressive approach in its efforts to quell inflation, it took its time in doing so, ignoring the initial data. Noted economist Mohamed El-Erian says that had the Fed not delayed crucial policy it could have spared unnecessary pain on millions of American households. Nevertheless, despite the “fumbled response,” fast forward to the present and there are signs inflation is cooling down.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

While El-Erian warns of complacency and notes of more “inflation complexity” ahead, he thinks one possible scenario moving forward is that the inflation rate “continues to decrease but then gets stuck at 3-4% over the second half of this year.”

Should that “sticky” scenario materialize, there’s a way for investors to circumnavigate that rate, by leaning into dividend stocks, particularly the ones that offer high yields. These classic defensive plays not only provide a shield against any incoming volatility but also present a way to stay ahead of the current inflation rate.

With this in mind, we dug into the TipRanks database and pulled up two stocks with a specific set of clear attributes: a dividend yield of at least 9% and Strong Buy ratings from the analyst community. Let’s take a closer look.

Starwood Property Trust (STWD)

The first high-yielding dividend stock we’ll look at is Starwood Property, the U.S.’s biggest commercial mortgage real estate investment trust (REIT). Being an affiliate of Starwood Capital Group, one of the world’s largest private investment companies, certainly helps its case and STWD has leveraged that connection to acquire, finance and manage commercial mortgage loans and other commercial real estate debt investments both in the U.S. and overseas. Over the years, total capital deployed by the company has exceeded $93 billion and Starwood currently handles a portfolio of more than $27 billion in total assets.

Given they’re obliged to pay 90% of taxable income to shareholders, REITs are known for their high dividend payouts and that is certainly the case here. Starwood offers a quarterly dividend payout of $0.48 and that yields an excellent 9.6% – that’s more than quadruple the average dividend yield found among S&P-listed firms, and easily beating the current 6.5% inflation rate.

Starwood will release 4Q22 earnings on March 1, but we can look at the Q3 results to get a picture of the company’s finances.

In 3Q22, the company generated revenue of $390.54 million amounting to a 29.2% year-over-year increase and rising from $294 million in the previous quarter. Net income came in at $194.6 million, amounting to $0.61 per diluted share.

According to the business, 97% of its infrastructure lending portfolios and 99% of its commercial lending portfolios have variable rates, making them favorably connected with rising interest rates.

Given the current economic backdrop, this could be beneficial to the company, says BTIG analyst Eric Hagen, who also likes the look of STWD “both an absolute and relative basis, especially around $20/share.”

“We think there’s more support for [STWD’s] valuation in response to rising interest rates… Another catalyst that we believe could unfold in the intermediate/long term is the acquisition of portfolios/companies that add new verticals or complement current business segments, and/or a potential spin-off of the residential non-QM business upon reaching greater scale. We believe the spin-off transaction could be similar to what STWD did with SWAY in 2014, which unlocked value in the platform,” Hagen opined.

Hagen backs up these comments with a Buy rating and a price target of $24, suggesting the shares will climb 20% higher over the coming months. Based on the current dividend yield and the expected price appreciation, the stock has ~30% potential total return profile. (To watch Hagen’s track record, click here)

Elsewhere on the Street, with one analyst preferring to sit this one but two others joining Hagen in the bull club, the stock garners a Strong Buy consensus rating. The forecast calls for one-year gains of 15%, considering the average price target clocks in at $23. (See STWD stock forecast)

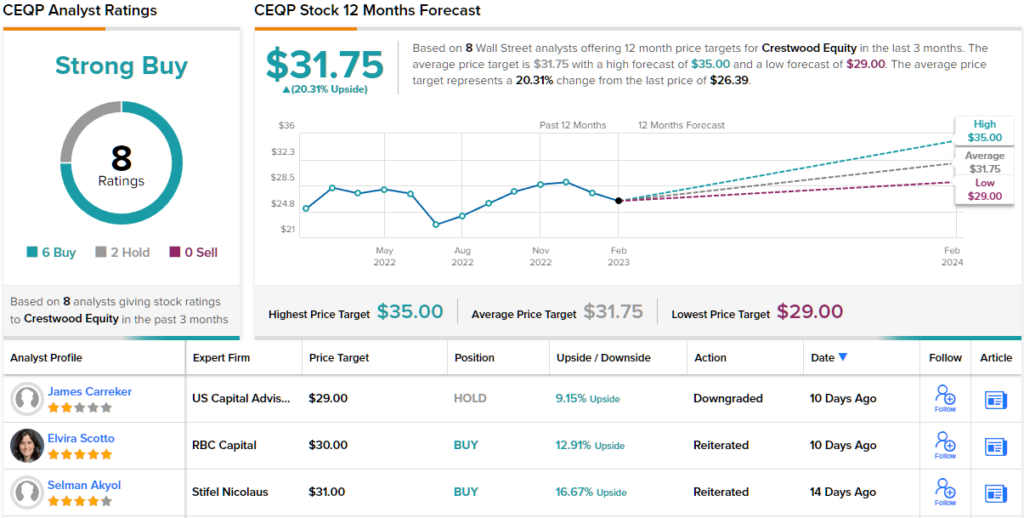

Crestwood Equity (CEQP)

Next up is Crestwood Equity, a master limited partnership midstream operator. That is, the company is involved in gathering, processing, storing, and transporting oil and natural gas. Its assets are located mainly in the Williston Basin, Delaware Basin and Powder River Basin, with segments split into Gathering & Processing North (Williston and Power River Basin), Gathering & Processing South (Delaware Basin) and Storage & Logistics.

In Q3, the latest quarterly report, Crestwood saw revenue rise by 27.6% year-over-year to $1.57 billion, yet falling short of the consensus estimate by $60 million. The company recorded a net loss of $43 million, vs. the net loss of $39.6 million in the same period last year, although adjusted EBITDA hit $209.3 million, improving on the $139.9 million generated in 3Q21, and amounting to a year-over-year increase of 50%.

The appealing aspect here is obviously the dividend and its strong yield. Earlier this week, CEQP paid out a quarterly cash dividend of 0.655 per common share. This annualizes to $2.62, and gives a yield of 10%.

Eyeing other gathering and processing companies, Crestwood has been busy on the acquisition front and closed a number of transactions last year including the acquisitions of Oasis Midstream Partners, and Sendero Midstream. The company also sold two unrequired assets.

Covering the stock for Wells Fargo, analyst Ned Baramov thinks last year’s events set up the company well for the future.

“Following a year of weather-related disruptions, acquisition/disposition activity, increase in leverage above management’s target, and an equity overhang from CHRD, we believe CEQP’s units are set for strong performance in 2023,” Baramov wrote. “Capex is projected to decline $50-75MM relative to 2022, as CEQP’s current gathering/processing capacity has room to accommodate growth and larger G&P projects across CEQP’s footprint are completed… We believe CEQP’s footprint in growing/stable producing regions (e.g., Bakken, Delaware, and PRB), declining capital requirements, and inflation protected G&P contracts will support a valuation premium relative to the G&P peer group.”

Taking all of the above into consideration, Baramov rates CEQP shares an Overweight (i.e., Buy) to go alongside a $35 price target. If Baramov is right, investors will be sitting on returns of ~33% a year from now. (To watch Baramov’s track record, click here)

Looking at the consensus breakdown, with the ratings skewing 6 to 2 favoring the Buys over Holds, this stock claims a Strong Buy consensus rating. At $31.75, the average target is set to generate returns of 20% in the year ahead. (See Crestwood stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.