Is all not well in the land of the tech giants? Microsoft and Alphabet, two of the stock market’s undisputed heavyweights, reported earnings on Tuesday after the market’s close and both disappointed.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

The lackluster showing from two of the most dependable names on Wall Street is a reflection of persisting negative macro factors, including a weakening economic backdrop, decades-high inflation and a strong dollar.

However, despite the underwhelming results, it’s not as if these trillion-dollar companies have suddenly turned into duds. As any investor worth their salt will know, when shares of companies with solid fundamentals get hammered, the time might be right to pounce. While cognizant of present headwinds, that is what some of the Street’s experts are recommending now.

So, let’s take a closer look at what happened to these two giants in the most recent quarter and see why these analysts think investors should stay in their corner. With help from the TipRanks database, we can also check in with the rest of Wall Street’s current sentiment.

Microsoft (MSFT)

With a market cap of $1.72 trillion, Microsoft ranks 2nd on the list of the world’s most valuable companies but that hasn’t made it immune to the bearish environment; following the post-earnings rout, the shares now sit 31% into negative territory for the year with investors not impressed with the fiscal first-quarter results.

At first glance, however, that seems a bit strange as the tech giant beat the estimates on both the top-and bottom-line. Revenue clocked in at $50.1 billion, in turn beating the analysts’ call by $410 million, while the company posted EPS of $2.35, $0.06 above the $2.29 consensus estimate.

But the beats mask several worrying developments. Against a backdrop of a soft PC market and a strong dollar, revenue climbed by just 10.6% year-over-year, amounting to the slowest quarterly revenue growth seen in 5 years. And despite the beat on the bottom-line, at $17.6 billion, net income represented a 14% decline from the same period a year ago.

With hopes pinned on Microsoft’s ever-growing Azure cloud services to offset other problems, the segment also underperformed; its 35% revenue growth might seem healthy, but it represented a deceleration and came in below the analysts’ expectations.

As for the outlook, while the company anticipates revenue will climb by double-digits this fiscal year, there were no exact earnings or revenue forecasts for the present second quarter or for the full year. At the same time, Microsoft warned the headwinds are unlikely to abate any time soon.

Nevertheless, while factoring in the current issues, Morgan Stanley’s Keith Weiss remains upbeat about the company’s long-term prospects.

“Bottom line,” said the 5-star analyst, “while heavier cyclical weights brings down our FY23 EPS estimates, we remain firmly convicted in the longer-term secular growth story at Microsoft, which we forecast drives a high-teens total-return profile over the next five year, framing an attractive risk/reward with shares trading at 23X our CY23 EPS.”

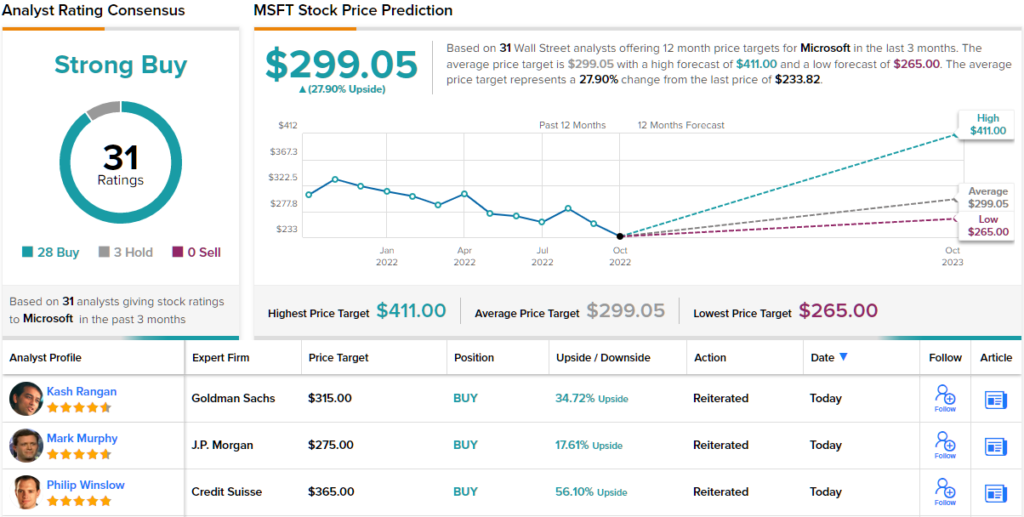

Weiss sticks with an Overweight rating, although there is a trim to the price target which is lowered from $325 to $307. Still, there’s upside of ~31% from current levels. (To watch Weiss’s track record, click here)

Wall Street remains mostly in the tech giant’s corner; based on 28 Buys vs. 3 Holds, the stock boasts a Strong Buy consensus rating. At $299.05, the average target suggests shares have room for ~28% growth in the year ahead. (See Microsoft stock forecast on TipRanks)

Alphabet (GOOGL)

On the list of stock market giants, boasting a market cap of $1.24 trillion, Alphabet sits just below Microsoft and likewise has endured a rough ride in 2022 with shares down by 34% in this year’s market rout.

But while Microsoft shares might have gotten the cold shoulder from investors despite beating expectations in the quarter, Alphabet did not even manage that feat.

Sending a warning shot to all operators in the digital advertising space, aside from a temporary decline as the pandemic hit, the company delivered its slowest growth rate since 2013. Revenue climbed by just 6% to $69.09 billion, coming in shy of the $70.7 billion anticipated by Wall Street.

Net income dropped from $18.94 billion in the same period a year ago to $13.9 billion, as the company delivered diluted EPS of $1.06 compared to the consensus estimate of $1.25.

There were disappointing metrics across the board. Google Search revenue increased by just 4.2% to $39.5 billion, some distance below the 8% growth forecast, and representing the first instance of a decline since it began reporting separate metrics for the unit in 2020, YouTube advertising dropped by 2% to $7.1 billion. The analysts were looking for a 4.4% uptick.

The market might have been spooked by the results and the impact felt by stocks exposed to the digital ad space, but Truist’s Youssef Squali had some reassuring words for disconcerted investors.

The 5-star analyst wrote, “While top-line results for Search missed consensus estimates and growth decelerated from lapping tough Y/Y comps, and a weakening macro environment, Google’s preeminent position as the engine of the global digital economy keeps it more resilient than other platforms, in our view. We believe that Google’s Search remains one of if not the most important customer acquisition and growth strategies for advertisers, who are continuing to advertise on Search despite a weakening global economy…”

“With mgt’s commitment to reign in hiring and focus investments on the highest growth priorities as it responds to the current uncertain macro, we expect revenue growth to re-accelerate throughout 2023 and the drop in margins to normalize, creating a compelling case for the stock N/M terms,” the analyst added.

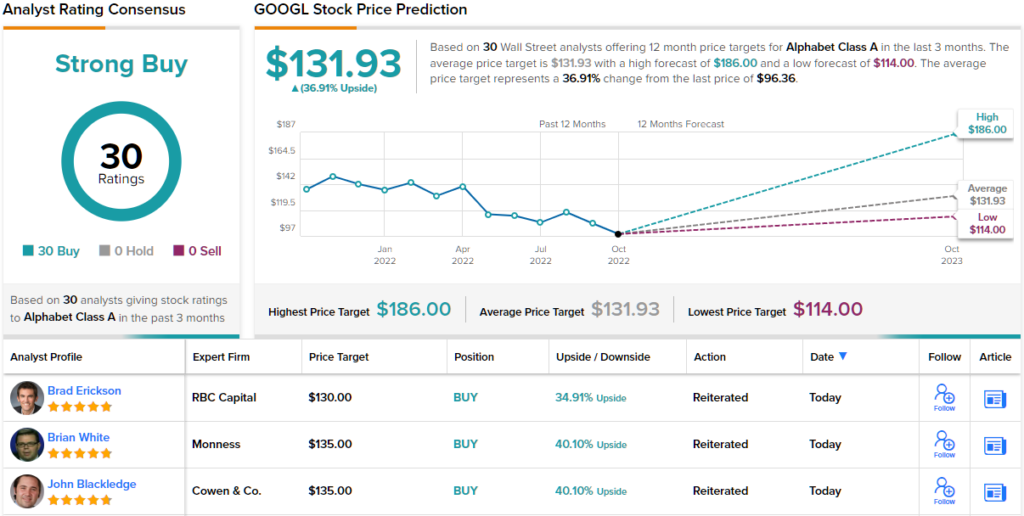

Therefore, Squali sticks with a Buy rating although the price target is lowered from $136 to $130. Investors are looking at returns of 35% from current levels. (To watch Squali’s track record, click here)

The results have done little to change Wall’s Street’s resoundingly positive stance on GOOGL; the stock claims a Strong Buy consensus rating, based on a unanimous 30 Buys. The forecast calls for one-year gains of ~37% considering the average price target stands at $131.93. (See GOOGL stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.