Microsoft’s (MSFT) investors are showing some impatience with the pace of AI development, as evidenced by the negative reaction to the company’s June quarter results. With MSFT now trading at a more depressed valuation, I remain bullish on its long-term prospects, acknowledging that these market reactions appear to be more short-term oriented.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

While Microsoft reported strong Fiscal Q4 results, there was a drop in margins and revenue growth, especially in cloud, where AI spending is concentrated. Short-term concerns about AI and CapEx seem exaggerated and likely led some investors to take profits from the stock’s recent gains. Consequently, long-term investors now have the chance to buy MSFT shares at a more attractive valuation.

Microsoft’s Fiscal Q4 Earnings Bar Was Too High, and Investors Grew Impatient

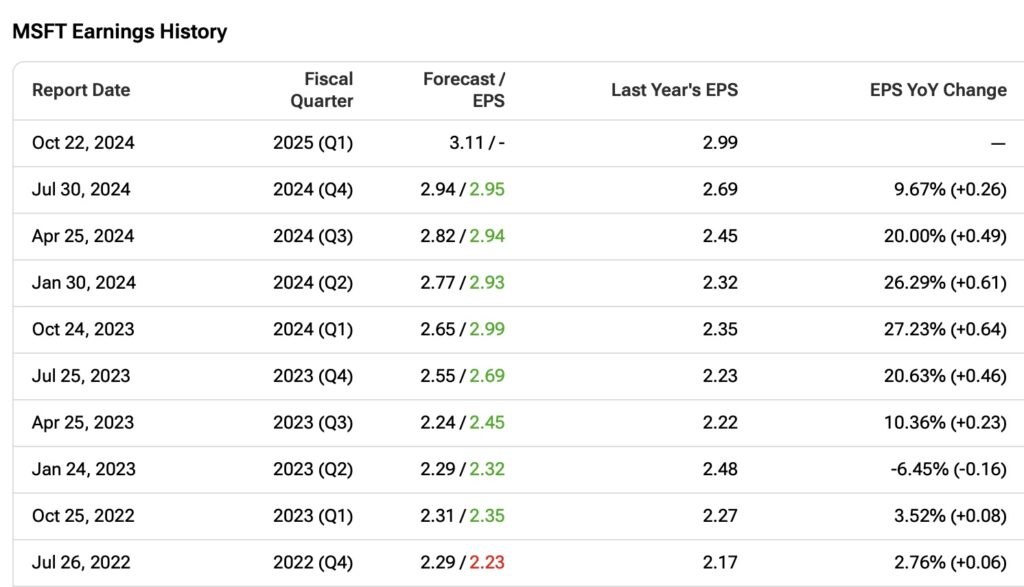

Once again, the company delivered strong results. For the eighth consecutive quarter, Microsoft exceeded EPS estimates, reporting $2.95 compared to the expected $2.94. In terms of revenue, Microsoft also surpassed expectations for the sixth consecutive quarter, with reported revenue of $64.7 billion versus an anticipated $64.4 billion, marking a 15% year-over-year increase.

Despite these achievements, many market participants were disappointed with Microsoft’s Fiscal Q4 results. Although the gross profit margin was an impressive 70%, it represented a 1% decline from the previous year. While this drop in profitability might seem minimal at first glance, the high expectations set by the 2024 rally in AI and large-cap tech stocks have made investors particularly cautious.

As a result, any signs that Microsoft’s profitability could be negatively impacted by AI investments have prompted some investors to take profits. This led to a roughly 4% drop in Microsoft shares following the earnings report. Now, the stock trades at a more de-risked valuation of 30x forward P/E, about 3% below its five-year average.

Moreover, two additional factors drew negative attention from investors.

First, the growth in commercial bookings was reported at 17% year-over-year, which fell short of the higher acceleration investors had anticipated, despite management seeing growth beyond its expectations. It’s important to consider the tough comparisons from the previous quarter, when this segment had recorded 29% year-over-year growth.

On a positive note, commercial remaining performance obligations increased by $34 billion from the previous quarter, reaching $269 billion. This indicates that Microsoft has secured contracts that will contribute to future revenue.

Second, the performance of the Intelligent Cloud segment, driven by Azure, was another area of disappointment. Server Products and Cloud Services revenue totaled $28.5 billion, reflecting 22% year-over-year growth. However, this figure slightly missed investor expectations because last quarter, Azure had grown by 24% year-over-year.

The slowdown in cloud revenue growth is particularly concerning, as competitors like Amazon (AMZN) and Alphabet (GOOGL) have managed to accelerate revenue growth for AWS and Google Cloud, respectively. This suggests that Azure might be lagging behind.

An interesting point made by analyst Gil Luria of D.A. Davidson is worth noting. He highlighted that Microsoft’s cloud growth is being driven by AI-related services, which are fueling additional growth. The company is leveraging its AI capabilities to cross-sell other products, such as premium Office products with co-pilot functionality, to enterprises that are using its AI services.

The bottom line is that AI remains the key driver for Microsoft. The company holds a significant lead in this area and continues to leverage AI to fuel growth across its business segments.

High Capital Spending Reveals High Confidence in Sustained Demand

Capital expenditures (CapEx) were also a big focus during the Big Tech earnings season. This metric highlights long-term growth plans and the challenge of balancing these goals with the need to stay profitable and meet short-term investor expectations.

Microsoft reported CapEx of $19 billion for the last quarter and has forecasted further increases in investment to strengthen its AI capabilities. This rising spending trend has led to growing impatience among investors, especially as profit growth has slowed. Alphabet faced a similar reaction. Despite solid quarterly results, its stock dropped due to concerns over its continued high spending on AI. The same issue applied to Microsoft. Despite strong overall numbers, its stock price declined.

However, it is crucial to note that Microsoft’s CFO, Amy E. Hood, emphasized that these investments will persist as long as there is demand.

She stated, “To meet the growing demand signal for our AI and cloud products, we will scale our infrastructure investments with FY ’25 capital expenditures expected to be higher than FY ’24. As a reminder, these expenditures are dependent on demand signals and adoption of our services that will be managed through the year.”

A primary concern is that half of the spending is allocated to land and financing leases, while the remaining half is invested in servers (which will depreciate quickly). In my opinion, the more concerning scenario would be if management hinted at a slowdown in AI spending, which could indicate a demand issue. Yet, this is clearly not the case here.

Is MSFT Stock a Buy, According to Analysts?

Analysts are very bullish on MSFT, maintaining a Strong Buy consensus rating. Following the Fiscal Q4 earnings results, five analysts have recently increased their price targets, with the average MSFT stock price target now at $503.19. This implies upside potential of 26.3% from the current share price.

Key Takeaways

On the back of still-great results, though not as outstanding as some wish to be, many Microsoft investors viewed this slight shortfall as an opportunity to sell shares and lock in profits.

Nonetheless, I believe that Microsoft’s bullish thesis remains intact, especially now that its valuation has become more attractive. Despite facing tough comps from previous strong quarters, the company continues to deliver impressive results, with revenues and earnings consistently surpassing expectations. The ongoing investment in AI capabilities indicates that robust demand is still to come. Even with a slight slowdown, Microsoft remains a compelling choice for the long term.