In late March, the Cyberspace Administration of China (CAC) made known its intention to examine the products offered by Micron (NASDAQ:MU) in the Chinese market. The reason given for this action was to ensure the protection of the supply chain for vital information infrastructure. Essentially, the Chinese government was saying that the company’s products posed a threat to national security, in what was another example of ongoing tensions between the US and China.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Since then, the memory giant has given several updates outlining how much of a negative impact the CAC ruling could have. A recent 8-K filing stated that around 50% of revenue from firms headquartered in mainland China and Hong Kong, which in total represents 25% of the total revenue haul and which equates to low-double-digit (%) of company sales are now at danger of being affected.

With all this as backdrop and Micron about to report FY3Q (May) earnings on Wednesday (June 28), Goldman Sachs analyst Toshiya Hari thinks the time is right for a reassessment of his MU model.

“While the situation remains fluid — as the evolution in Micron’s estimation of the potential impact suggests — we are reducing near-term estimates to reflect what is, in our view, likely share loss for Micron in China, largely inline with the company’s current estimate of the impact from CAC’s ruling,” the 5-star analyst explained.

The result is a respective reduction of FY23/24/25 revenue estimates by 7%/18%/4%.

However, despite this headwind, it’s not all bad. On the contrary, says Hari, the outlook elsewhere remains upbeat. “our views on 1) the overall Memory cycle predicated on demand stabilization, particularly across the PC and smartphone end-markets, and disciplined supply-side actions on the part of all participants, and 2) Micron’s medium- to long-term competitive position in DRAM and NAND, remain unchanged,” Hari went on to add.

And despite the downward revision, on the back of more than 12 months of negative EPS revisions, Hari anticipates the stock will enter a “positive EPS revision cycle in 2HCY23,” driven by the trends outlined above.

In fact, these developments trump the CAC issue and result in a price target hike. The figure moves from $70 to $80, suggesting shares have room for 22% growth over the coming months. Hari’s rating stays a Buy. (To watch Hari’s track record, click here)

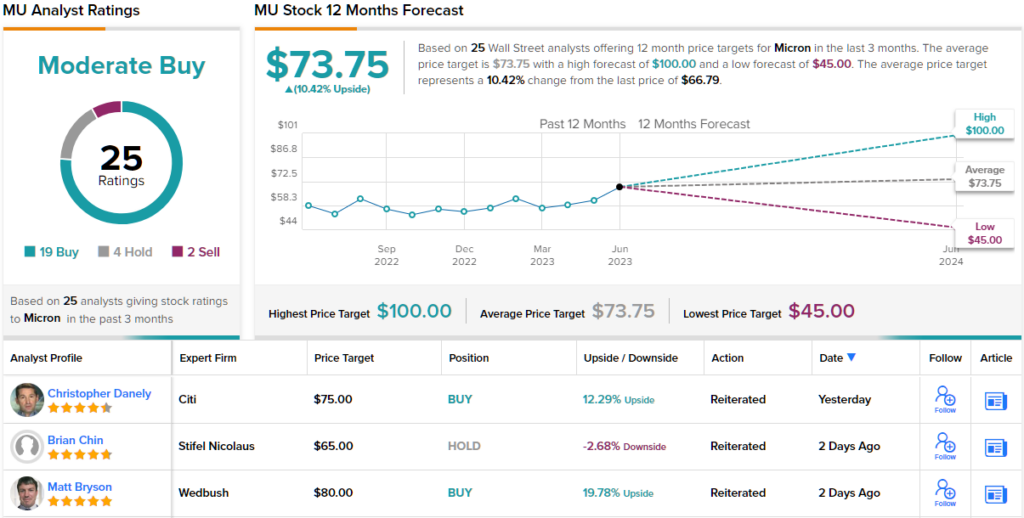

Elsewhere on the Street, the stock claims an additional 18 Buys, 4 Holds and 2 Sells, all for a Moderate Buy consensus rating. Going by the $73.75 average target, a year from now the stock will have appreciated by 10%. (See Micron stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.