Perceived wisdom goes that the way to outperform the market this year has been by leaning into the Magnificent Seven stocks (AAPL, AMZN, GOOGL, META, MSFT, NVDA, TSLA).

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

These market leaders – all tech giants – are seen as being responsible for the market’s rally, but hold that thought, says Ark Invest CEO Cathie Wood.

These names don’t take up much room in Wood’s flagship Ark Innovation ETF, yet the fund, with its focus on bold, innovative stocks, still managed to beat the main indexes’ performances throughout the first half of the year. And that is indicative of a notable trend, says Wood.

“We don’t own most of the Magnificent Seven. We own Tesla in size, but the others, either not at all or partial positions, are in our flagship strategy,” she recently said. “And through the second quarter, we outperformed even the NASDAQ 100, which is dominated by those stocks… I do think our outperformance in the first half – and it was significant outperformance – suggests that maybe underneath the market is broadening out, and that’s very healthy.”

Meanwhile, Wood has been loading up on the names she sees as primed to keep on outperforming, and as would be expected, amongst them are some cutting-edge equites. We decided to get the lowdown on a pair of her recent picks and ran them via the TipRanks database to also gauge general Street sentiment toward them. Here’s what we found out.

Intellia Therapeutics (NTLA)

Wood’s investing style heavily favors pioneers, and our first stock has that in spades. Intellia Therapeutics is a biotech company at the forefront of the development of CRISPR/Cas9 gene editing technology for therapeutic applications. Intellia is a leader in the field, harnessing the power of CRISPR to develop innovative treatments for a wide range of genetic diseases. The company’s mission is to create life-changing therapies by precisely editing the DNA within a patient’s cells, offering the potential to cure or significantly mitigate genetic disorders at their root cause.

This is a company boasting some serious credentials: one of Intellia’s co-founders, Jennifer Doudna, alongside Emmanuelle Charpentier, was awarded the 2020 Nobel Prize in Chemistry for the groundbreaking CRISPR endeavors.

All the above wouldn’t mean much for Intellia without an active pipeline, and here, in addition to several therapies in the pre-clinical stage, the company has several drugs that have advanced to the clinic.

Amongst these are NTLA-2001, being worked on as an in vivo, systemically delivered, investigational CRISPR-based therapy for protein disorder transthyretin (ATTR) amyloidosis. The company intends to submit an Investigational New Drug (IND) application to the FDA for a pivotal study of NTLA-2001 in ATTR-CM (cardiomyopathy) this month. And subject to regulatory feedback, Intellia hopes to kick off a global study before the end of the year. Before the end of the year, the company also plans on releasing additional clinical data from the ATTR-CM arm of the Phase 1 study.

The company is also studying NTLA-2002 as a treatment for hereditary angioedema (HAE), a rare genetic condition defined by inflammatory attacks. Intellia plans to complete enrollment in the Phase 2 portion of the Phase 1/2 study in the second half of the year, and should the regulators approve, initiate a global pivotal Phase 3 study by Q3 2024.

All of this has evidently gotten Wood in a buying mood. Over the past month, via the ARKK fund, she purchased 193,896 shares. Her overall holdings now stand at 6,940,818 shares, currently worth ~$261.6 million.

Based on the pipeline’s prior performance and upcoming catalysts, Barclays analyst Gena Wang is also confident Intellia represents an excellent opportunity for investors.

“Given initial IND clearance in HAE, broadly applicable preclinical data in fetal development, and older patient population in ATTR-CM, we expect high probability of IND clearance (likely in Nov) for NTLA-2001 Ph3 in ATTR-CM,” the analyst said. “We continue to believe NTLA’s in vivo gene editing platform was well validated by multiple clinical programs, with significant upside potential from multiple near-term clinical catalysts.”

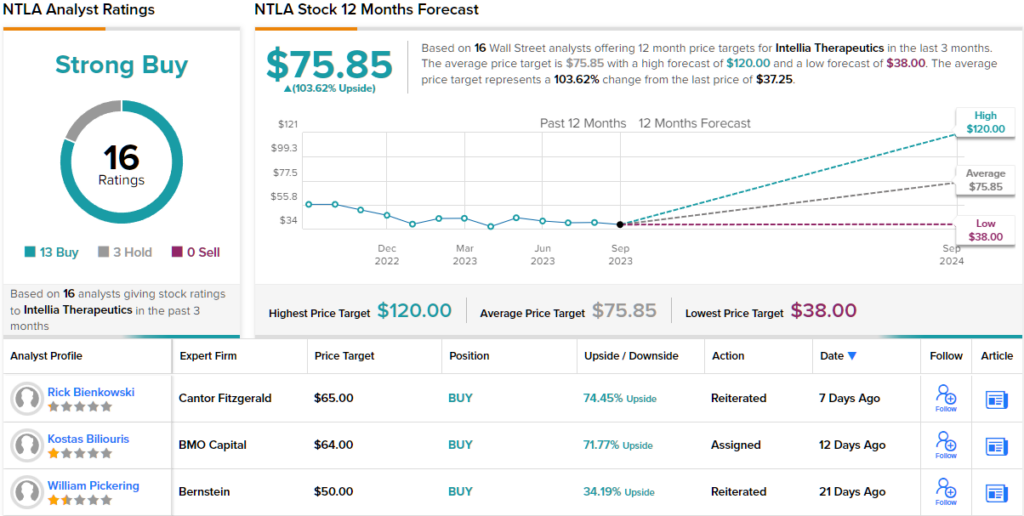

Accordingly, Wang has an Overweight (i.e., Buy) rating on NTLA shares, backed by a $90 price target. There’s plenty of upside – 139% to be exact – should the target be met over the next 12 months. (To watch Wang’s track record, click here)

Most on the Street agree with Wang’s stance. The stock’s Strong Buy consensus rating is based on 13 Buys vs. 3 Holds. At $75.85, the average price target indicates the analysts expect the stock to more than double in value in the year ahead. (See NTLA stock forecast)

Pacific Biosciences (PACB)

We’ll stay in the biotech space for the next Wood-backed name, although Pacific Biosciences operates in a different segment. The life science tools company develops and brings to market gene sequencing systems.

Pacific Biosciences operates with two primary sequencing systems: one is Single-Molecule Real-Time Sequencing (SMRT), which capitalizes on the characteristics of zero-mode waveguides, and the other is Sequencing by Binding (SBB) chemistry. The SBB method employs natural nucleotides and a seamless incorporation process for attaching and elongating DNA strands.

Unlike biotech companies focused on clinical development, the company’s products bring in a regular revenue stream. In Q2, boosted by the new Revio long-read sequencing systems (commercial shipments began in March), the company generated record quarterly revenue of $47.57 million, in what amounted to a 34% year-over-year increase. The figure also beat the Street’s forecast by $7.66 million. The strong performance extended to the bottom-line too. While operating at a loss, adj. EPS of -$0.26 fared better than the -$0.31 anticipated by the analysts.

On the Q2 earnings call, the company also disclosed that it had agreed to acquire Apton Biosystems, a developer of sequencing and single-molecule detection systems, in a deal that could rise up to $110 million.

Against this backdrop, Wood has been loading up. Via the ARKK fund, she bought 298,214 shares in August, bringing her total holdings to 15,108,533 shares. These currently command a market value of more than $172.3 million.

TD Cowen analyst Dan Brennan sees plenty to like about this next-gen DNA sequencing specialist.

“Expectations are high for PACB, with a targeted 40-50% multi-year revenue CAGR and an exciting, highly differentiated Revio launch. Our customer diligence has been solid, and we feel strong 2Q results support our positive thesis,” Brennan said. “The Apton acquisition will generate investor interest, with mgmt indicating gaining access to such a platform is consistent with their LT planning (and creates a leverageable asset in a very large market with a fairly advanced platform) – all true, though we argue given excitement over the material Revio opportunity, Apton focus/spending needs to be managed appropriately and not in any way dilute the focus/execution with Revio.”

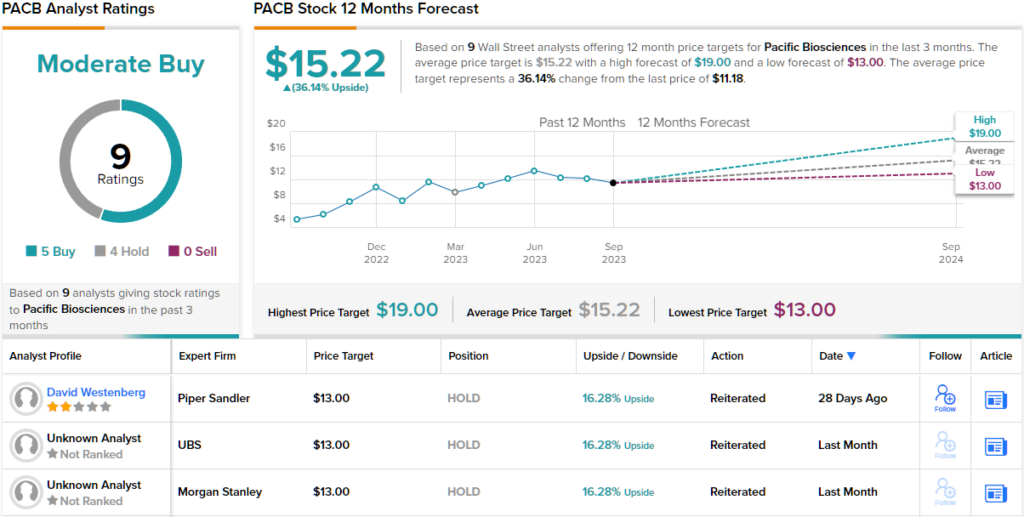

These comments underpin Brennan’s Outperform (i.e., Buy) rating on PACB, while his $19 price target offers one-year upside of ~70%. (To watch Brennan’s track record, click here)

Turning to the rest of the analyst community, opinions are split almost evenly. 5 Buys and 4 Holds add up to a Moderate Buy consensus rating. At $15.22, the average price target implies 36% upside potential. (See PACB stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.