Having a bearish stance has worked nicely in 2022, but as in most walks of life, flexibility is often a key ingredient for success. With this in mind, Morgan Stanley’s Chief U.S. Equity Strategist Mike Wilson thinks having an open mind as 2023 enters the frame is now more important than ever.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

“After a 12-month period when being stubbornly bearish paid off handsomely, we think we will now enter the final stages of the bear market where two-way risk must be respected,” Wilson said.

Not that Wilson thinks we’re totally done with the bear market just yet; the strategist does not expect the path ahead to be “smooth” and thinks consensus earnings are still “materially too high.”

Nevertheless, Wilson has pivoted to a more “bullish tactical view,” and this also applies to investors who will need to be “more tactical and make choices with no regrets.”

Against this backdrop, the analysts at the banking giant have pinpointed two names that they think make good investment choices in the current environment. Do other analysts agree? According to the TipRanks database, they certainly do; both stocks are rated as Strong Buys by the analyst consensus and are projected to pick up steam in the months ahead.

Palo Alto Networks (PANW)

Cybersecurity is an essential ingredient these days for any online operation, and the first Morgan Stanley pick we’ll look at is a leader in the space. Palo Alto Networks specializes in cybersecurity offerings which run the gamut from firewall appliances and software, zero trust network security, security analytics and automation through to professional, and educational services and cyber security consulting, amongst other products. The company splits its operations into three distinct platforms: Network Security, Cloud Security and Security Operations.

It’s a model that has shielded the stock relatively well in 2022’s bear; the shares might be down 7% on a year-to-date basis, but that performance amounts to a far better display than the tech-heavy NASDAQ’s 29% drop.

And it is earnings displays like the latest which have assisted in the relative outperformance. Against a backdrop of other tech stalwarts stumbling badly, in the recently released FQ1 report (October quarter), the company beat Street expectations. Revenue rose by 24.8% year-over-year to $1.56 billion, coming in ahead of the Street’s call by $10 million, while billings increased by 27% from the same period a year ago to $1.7 billion. At the other end of the scale, the company delivered adj. EPS of $0.83, some distance above the $0.69 expected on Wall Street.

That performance has drawn the applause of Morgan Stanley’s Hamza Fodderwala, who sees plenty of more growth ahead.

“We continue to believe PANW will be the first $100 billion market cap company in cybersecurity, or nearly double its current share price in 2 years,” the analyst confidently said. “Our thesis is predicated on PANW’s broad platform evolution, market leadership in Cloud security and improving profitability coming out of a multi-year investment cycle. FQ1 results highlighted all of these aspects, as the company once again delivered a strong result against an uncertain macro backdrop in which several security companies cut their outlooks.”

Accordingly, Fodderwala rates PANW an Overweight (i.e., Buy), backed by a $268 price target. The implication for investors? 56% upside from current levels. (To watch Fodderwala’s track record, click here)

Overall, PANW receives widespread coverage on Wall Street and most of it is decidedly positive; of the 36 analyst reviews on file, 4 implore to stay on the sidelines, but all the rest are positive, making the consensus view a Strong Buy. Going by the $228.24 average target, the shares will climb 32% higher over the coming months. (See PANW stock forecast on TipRanks)

Bath & Body Works (BBWI)

Let’s take a sharp turn for the next Morgan Stanley-endorsed name. Bath & Body Works is a retailer that sells personal care products such as soaps, lotions and other items like candles and fresheners. The company’s products are distributed through its chain of stores, websites, and partner locations. While the majority of operations are in the United States, it has a burgeoning Canadian and international business.

With consumers tightening wallets due to the effect of soaring inflation, many retailers have been in a rough spot this year, and while that has been reflected in BBWI’s dwindling sales, the company has shown operational excellence in dealing with the downturn. This was evident in the recently released Q3 financial statement.

While revenue fell by 5% year-over-year to $1.6 billion, the figure trumped Street expectations by $40 million. But the really good news was the bottom-line; the company delivered EPS of $0.40, double the analysts’ $0.20 forecast while also increasing the full-year outlook for earnings per diluted share from between $2.70 to $3.00 to between $3.00 and $3.20. Consensus had that figure at $2.89.

BBWI also saw out the quarter with inventory up by only 10% from the same period a year ago, a performance 20+ points better than Q2’s 33% uptick. Moving forward, the company’s Q4 guide called for year-over-year inventory growth of +mid-teens.

This is a particularly impressive feat, says Morgan Stanley’s Alexandra Straton.

“In our view, this could represent one of the best inventory results in our coverage this earnings season, & should make for potentially less promotion & discounting-driven margin pressure in 4Q and beyond compared to specialty retail peers,” explained the analyst. “This speaks to BBWI’s incredibly nimble & mostly domestic supply chain.”

“We’re bullish on BBWI for its fundamentally attractive business model, ongoing room for beats & raises, as well as its valuation re-rating opportunity,” Straton went on to say.

Unsurprisingly, then, Straton rates the shares as Overweight (i.e., Buy) while the price target is given a bump; the figure moves from $72 to $76, suggesting shares will climb 92% higher in the year ahead. (To watch Straton’s track record, click here)

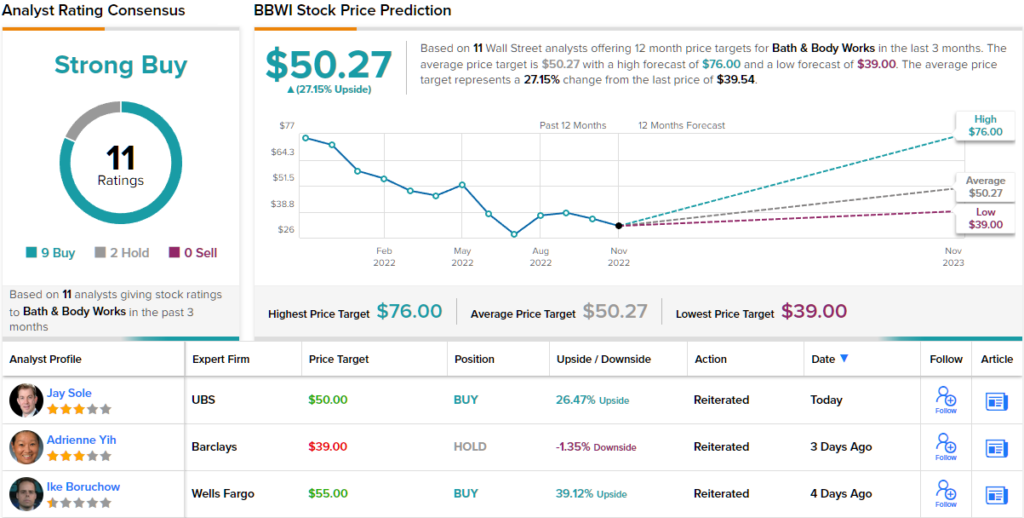

BBWI gets strong support from Straton’s colleagues too; the ratings break down 8 to 2 in favor of Buys over Holds, all culminating in a Strong Buy consensus rating. The forecast calls for 12-month returns of 27%, considering the average target stands at $50.27. (See BBWI stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.