Shares of athleisure pioneer Lululemon (LULU) are starting to see a bit of relief.

Despite the recent run-up in expensive, risky stocks, there are reasons to think that the recent win streak in such names is more of an opportunity to take profits rather than the start of a sustained turnaround.

Lululemon is one of the most intriguing companies with a remarkably long growth runway. However, merely having a long growth runway is no guarantee of success if a firm cannot execute.

The company’s management team has done a magnificent job perfecting the omnichannel experience. The company has perfected both the online and offline experiences, the latter of which could get a jolt as the COVID-19 pandemic continues to abate. Can management pull it off again as it looks to go global?

While the firm’s e-commerce strengths are undeniable, Lululemon will have to push into new product categories to maintain its hefty multiple.

The Canadian company, which single-handedly induced the rise of the “athleisure” fashion trend, is not afraid to broaden its focus. Many companies in the tech sector have done this to excite shareholders and pursue new growth verticals.

However, at current valuations, I’m skeptical as to whether the company can continue its streak of profound success. For that reason, I’m staying bearish on LULU stock.

Lululemon: Massive Expansion Opportunity

Menswear and footwear are not traditional areas of retail that Lululemon is known for. That could change as the company looks to put its brand power to the test in an arena it’s not as familiar with.

There’s no denying Lululemon’s brand power, at least in the North American market. If the firm can find further success in new corners of the apparel market, the next leg of growth could be astronomical, as management readies to put its foot to the gas internationally.

Undoubtedly, China is a hot market that could fuel many years of enviable growth. After all, Canadian and American brands have been very appealing among Chinese consumers.

As Lululemon bolsters its brand strength, I think it will be tough to stop the firm once it’s ready to expand beyond Canada and the U.S. Still, some challenges could weigh on the firm’s ability to garner even more brand affinity.

Rising Rivals

The real question is whether Lululemon’s brand is attractive enough at the international level to justify its above-average prices. Lululemon is no luxury retailer. At best, it’s on par with Nike or Adidas. Given its many years as a yoga apparel maker, drawing in crowds from the non-yoga segment could prove tricky.

Ultimately, I think Lululemon will struggle with its push into new product categories that go above and beyond just yoga. At the same time, Lululemon also has to play defence, as other sporting apparel makers like Nike, Adidas, and Athleta, a fast-growing yoga clothing brand under the Gap (GPS) umbrella, set their sights on Lululemon’s traditional market.

Athleta, in particular, stands out as a prominent threat that could eat into Lululemon’s brand power and its ability to charge premium prices. The company teamed up with Olympic champion Simone Biles and most recently, singer Alicia Keys, with a logo that’s arguably as graceful as Lululemon’s.

Though its growth levers could help push Lululemon’s growth moving forward, I find it difficult to believe that it can continue sustaining its enviable margin growth once the initial margin enhancement from the DTC (Direct-to-Consumer) efforts begin to fade.

Lululemon’s Less-than-Stellar ESG Score

Lululemon has considerable exposure to fluctuations in the price of raw materials. The company faced backlash during the Beijing 2022 Olympics, as protestors rallied in front of Lululemon’s flagship shop, slamming the firm for its fossil fuel (most notably coal) emissions.

Lululemon doesn’t have the worst ESG score in the world, but it can certainly do better. Climate activists recently shed light on the firm’s emissions, which could harm the brand if management doesn’t commit to further efforts to reduce its environmental impact.

Brand power is vital for Lululemon to sustain its high margins. Any reputational harm could act as a hit to Lululemon and provide a boon for the likes of a more affordable up-and-coming competitor in the yoga space.

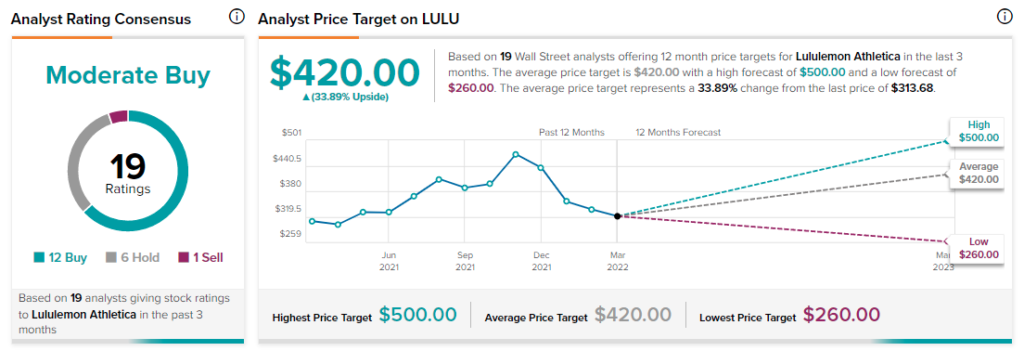

Wall Street’s Take

According to TipRanks’ rating consensus, LULU stock comes in as a Moderate Buy. Out of 19 analyst ratings, there are 12 Buy recommendations, six Hold recommendations, and one Sell recommendation.

The average Lululemon price target is $420, implying 33.9% upside potential. Analyst price targets range from a low of $260 per share to a high of $500 per share.

Bottom Line on Lululemon

There’s a lot to love about how far Lululemon has come over the past few years. It’s an omnichannel powerhouse with intriguing opportunities to expand its focus.

With intense competition in the yoga and apparel scene and other headwinds that could weigh on margins, investors must ask if there’s any value in buying the stock at over 46 times trailing earnings. That’s expensive, and it doesn’t leave much room for error.

Even after the stock’s significant drop, I’m not inclined to chase it here. Further, it’s too soon to gauge how strong the brand is from a global perspective.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure