This week, Chinese coffee chain Luckin Coffee (OTC: LKNCY) got a positive research note from John Zolidis, president of Quo Vadis Capital, a long-term bear on the stock. I’m neutral on LKNCY.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

“It’s true that Luckin Coffee (LKNCY) is in Chapter 15 bankruptcy, is in China, and was a fraud,” Zolidis said. “However, the balance sheet is in very good shape, and we expect an exit from Chapter 15 in the first half of 2022. The fraud is over (we believe), and we now believe the numbers are as trustworthy as they can be.”

“Meanwhile, while Luckin remains a Chinese company, we believe it is insulated from the biggest China-related risks as it is a Chinese-native brand, and value-priced coffee is not particularly economically-sensitive. Lastly, the business is thriving despite Covid-related lockdowns, which brings us to the real reason we think the stock is interesting.”

Zolidis’ last point about Luckin’s business thriving doesn’t seem to be supported by its website traffic, which has been trending lower since August.

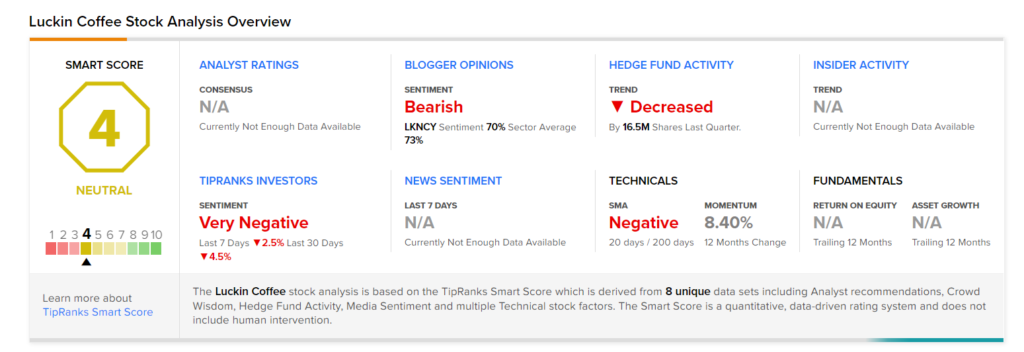

It also isn’t supported by TipRanks analysis and rating results. Luckin has a Smart Score of 4 out of 10, due to weak technicals, decreased hedge fund activity, and very negative investor sentiment.

Xolidis’ recent note is a big difference from a note out in September when he thought that Luckin Coffee was running out of time to restructure its convertible debt and get its business model right. Back then, he believed that the stock was overvalued and rated it a Sell.

What Makes the Stock Interesting

Zolidis has now provided several reasons that Luckin Coffee’s stock is attractive. One of them is that it is probably a remarkable turnaround story.

“Six quarters ago, store-level margins were negative 25%. But in the September quarter, store-level margins were positive 28%,” he explained. “In 2020, the company’s EBITDA margin was negative 39%. In 2021, we are forecasting a 5% EBITDA margin. By 2023, we estimate EBITDA margins can rise to 15%”

Then there’s the possibility that Luckin’s shares are mispriced.

“We previously had the stock at SELL, but took the name off our sell list on November 9, when it was trading around $14,” Zolidis continued. “Subsequently, the company reported stellar 3Q21 results (although perhaps no one noticed) and the stock sold-off into year-end, closing last week around $9. At this price, we estimate an EV of $2.7B, which represents 8.6x our 2023 EBITDA estimate. Given the apparent quality of the reconstituted business and its growth opportunity, we believe this is an attractive multiple.”

Still, investors looking into buying Luckin’s shares should be aware of several risks they face, like Finance and Corporate risks, Legal and Regulatory risks, and Production risks.

The company still needs to monetize its business model, which relies more on coffee to go and less on a “third place” concept, where people can enjoy their favorite drinks with friends and associates, as is the case with Starbucks’ business model.

Focusing on coffee to go, Luckin’s business model turns coffee into a commodity, meaning a product that everyone can sell, which leads to price wars.

Economists and business strategists know very well that price wars are detrimental to a business in the long term. They erode profit margins to the point where the return on invested capital is equal to or below what money can earn elsewhere.

Summary and Conclusions

Buying shares in turnaround companies is a high-risk proposition. Especially when these companies have no reliable financial statements, for investors to evaluate.

That’s why Luckin’s shares aren’t suitable for everyone.

“We know this idea is not for everyone, but if you can get involved in something like this, we feel like we have a real edge in analysis relative to the market, and there is a compelling case to spend time here,” Zolidis said.

Investors should be reminded that hype is never a good substitute for due diligence.

Download the TipRanks mobile app now

Disclosure: At the time of publication, Panos Mourdoukoutas owned shares of Starbucks.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of TipRanks or its affiliates Read full disclaimer >