As a startup electric vehicle manufacturer, Lucid Group (NASDAQ:LCID) arguably started off on the right foot — exclusively targeting affluent consumers that can actually afford EVs before addressing the middle-income crowd. However, management’s latest decisions reflect that Lucid suffers from the same industry-wide acid test impacting other manufacturers. Subsequently, I am now neutral on LCID stock.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

The Right Idea Doesn’t Bolster LCID Stock

With sector stalwart Tesla (NASDAQ:TSLA) steadily moving toward the middle-income consumer segment over the past few years, Lucid presumably had the right idea to focus on another niche. Rather than suffer a war of attrition with Tesla for middle-income dollars, it seemed better to dominate the lower-volume but higher-margin, high-income subsector. Even history winked at LCID stock.

Last year, I authored a bullish argument for Lucid based on the historical trend of automotive integration. Back in the early 20th century, only 0.11 automobiles existed per every 1,000 people. That’s a staggeringly low figure by contemporary standards. However, it’s very similar to the adoption rate of EVs.

Eventually, as technologies such as mass production materialized and improved, combustion automakers at large benefited from economies of scale. Soon thereafter, the adoption rate of personal vehicles increased sharply. Theoretically, EV adoption should follow roughly the same path.

However, in the meantime, only those that can really afford EVs will be able to acquire one. With the average price of new electric-powered cars hovering above $60,000, making the transition to electrification isn’t feasible for the average U.S. household. Therefore, Lucid arguably had the right idea to target rich consumers.

Indeed, the average of vehicles on U.S. roadways increased from 12.2 years to the current 12.5 years. This dynamic indicates that consumers are holding onto their vehicles for longer than ever. Such a circumstance clashes with the concept that consumers are ready to make the leap to EVs. They’re not. Lucid understood this, but it just hasn’t worked out for LCID stock.

Price Cuts Send a Worrying Message

In early February of this year, TipRanks contributor Steve Anderson reported that Lucid took a page out of Tesla’s playbook, joining in the EV price wars. Fearing that its rivals would leapfrog the premium EV label, Lucid rolled out its own incentive plan — “$7,500 off the Air Touring and Air Grand Touring lines of Lucid cars.”

On paper, the move was probably a necessary one, given the tight competition in the EV space. At the same time, management broadcasted a worrying message: the upper-tier consumer category may not have been as economically insulated as previously perceived.

Compounding matters was that Lucid again issued a customer incentive. According to TipRanks reporter Sirisha Bhogaraju, ahead of the company’s second-quarter results, it “lowered the price its Air Pure sedan by $5,000 to $82,400, with the offer being valid ‘while supplies last.’”

At the risk of repeating the point, Lucid probably made the only decision it could. However, continuing to offer incentives articulates the same message: higher-income consumers are not necessarily immune to economic pressures.

Unfortunately, that’s not what an enterprise geared toward affluent customers wants to hear. After all, Lucid’s core reason for being centers on serving a luxury brand and eventually dominating this elite subsector. If it’s forced into a pricing war, that’s going to be a vexing challenge.

A Glimmer of Hope

While circumstances don’t look great for LCID stock, the faithful bulls can take comfort in Lucid’s liquidity. According to its Q2 report, the company commanded approximately $6.25 billion in total liquidity. Per management, that should keep the company funded into 2025.

Further, Lucid achieved several major milestones, perhaps most notably entering a long-term strategic partnership with Aston Martin. Given that Aston Martin is a world-recognized marquee brand, it’s good to see that Lucid hasn’t given up on its premium-label ambitions. However, management must make this framework stick because it really can’t go down the consumer-income spectrum.

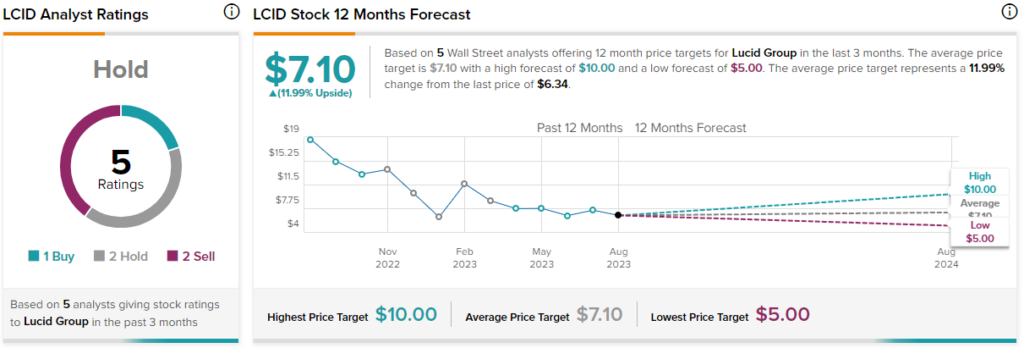

Is LCID Stock a Buy, According to Analysts?

Turning to Wall Street, LCID stock has a Hold consensus rating based on one Buy, two Holds, and two Sell ratings. The average LCID stock price target is $7.10, implying 12% upside potential.

The Takeaway: It’s Do or Die for LCID Stock

Although Lucid initially started off on the right foot by targeting higher-income consumers, its pricing cut decisions undermine the premium-label message. Still, it’s also making choices to forward the original strategy of targeting affluent customers. However, it really must make the strategy work because LCID stock is not viable as a middle-income play.