One of the most exciting electric vehicle (EV) stocks in the market late last year, when valuation soared to the stratosphere, the tables have sadly turned for Lucid Group (LCID).

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Against the January opener of 2022, LCID stock finds itself deep into negative territory, though if historical trends regarding automotive innovation pan out, this investment could be a long-term discount. I am bullish on LCID.

For any investor seeking a growth opportunity to hold and marinate for several years, if not decades, the burgeoning EV sector seems to be a no-brainer.

Fundamentally, multiple government agencies have sounded the alarm about carbon emissions and the need to implement mitigatory measures immediately. Politically, the Biden administration has spearheaded efforts to tackle global pollution.

Finally, the economic incentive is only expanding in scope. After years of consecutive net losses, sector leader Tesla (TSLA) is finally profitable, posting annual net income in 2021 and 2022 – encouragingly during the COVID-19 crisis. Recognizing the lucrative opportunity, EV upstarts sprouted like weeds, each determined to cover the entire income spectrum, particularly the middle-income segment that Tesla has difficulty reaching.

However, EV battery costs are such that – while significantly declining over the years – the underlying vehicles are still too expensive for average households. It’s not just about the science but the historical integration of new technologies. Therefore, Lucid, with its focus on premium EVs, is arguably best positioned among the non-Tesla competitors.

Lucid Group Stock Analysis

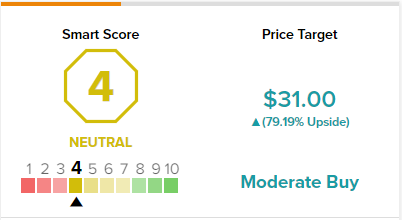

On TipRanks, LCID scores a 4 out of 10 on the Smart Score spectrum. This indicates moderate potential for the stock to perform in line with the broader market.

History Smiles on LCID Stock

According to the Office of Energy Efficiency & Renewable Energy, there were about 816 vehicles per every 1,000 people in the U.S. – at least this was the case in 2014 – newer information was hard to find. Understandably, consumers take for granted that anybody who wants to own a personal vehicle can relatively easily save up for one. However, such privileges weren’t always readily available.

In fact, back at the start of the 20th century, there were only 0.11 automobiles per every 1,000 people, a staggeringly low figure in comparison to modern standards. However, this low rate of early adoption is analogous to what analysts recognize in the EV market.

Performing the same exercise above for EVs, in 2011, there were roughly 0.06 electric-powered vehicles per every 1,000 people. A decade later, this metric increased to slightly over seven vehicles per 1,000. During the same ten-year span, combustion cars jumped from 0.11 to 5.07.

When visually represented, the rate of integration for both combustion cars and EVs during their respective timelines are almost identical. Indeed, the correlation coefficient between the two data points is 98%. Here is where circumstances are becoming very intriguing for LCID stock.

Historically, the concept of auto ownership didn’t become comprehensively normalized until around 1960, when car culture took root in the U.S. At that point, there were 410 vehicles per 1,000 people. In other words, Lucid enjoys a very long upside pathway before middle-income-focused competitors eat away at its market share.

The Pandemic Offers a Cynical Catalyst

Interestingly, the rate of integration for EVs dipped in 2020 – logically a casualty of the COVID-19 pandemic. Integration would later improve in the following year – and quite dramatically so – yet, even this improvement has surely been impacted by global supply-chain disruptions. Stated differently, people want to make the transition to electric, but the supply just isn’t there.

Add in soaring energy costs, and consumers are downright anxious to buy EVs. However, the economic reality is that only those blessed with the funds can make the transition. Data from earlier this year indicates that the average transaction price for a new EV skyrocketed to slightly over $60,000. Given that the median household income in 2020 was $67,521, a $60,000 EV for most households would be a stretch.

Naturally, then, Lucid stars under a cynical spotlight. With its Lucid Air starting at $87,400, the EV manufacturer offers zero pretenses about its mission statement. It exists to sell to the rich and the rich alone. Based on the rate of integration of new technologies, this is arguably the right business strategy.

Further, in the years ahead, Lucid – assuming that it can stay in business – can potentially dominate the upper-income threshold. Once economies of scale allow for EVs to be sold to average-income households without causing financial distress, then management can adjust to the new paradigm.

Nevertheless, if history is any guide, this paradigm won’t arrive for many, many years into the future.

Wall Street’s Take

Turning to Wall Street, LCID is a Moderate Buy based on two Buys, zero Holds, and one Sell rating. The average Lucid price target is $31, implying 79.2% upside potential.

Getting Down to Brass Tacks

While the broader political narrative seemingly pushes consumers to electrify their transportation, the economic fact is that unless technology improves to the point where EVs are truly accessible to middle-income households, they will remain platforms for the affluent. This dynamic suits Lucid just fine.

Of course, EVs represent an extremely competitive sector, and all would-be Tesla killers have mountainous challenges ahead. However, as a speculative idea, LCID stock intrigues because the underlying strategy aligns extremely well with historical norms of technological integration.