The automotive industry is at the beginning of a major shake-up, akin to the first flowering and spread of combustion-engine cars in the first place. Important new technologies are bursting onto the scene, including electric drive systems – and autonomously controlled vehicles. In China, car makers are already building autonomous cars with full-stack sensor systems, and they’re getting them onto the roads. We can look forward to a similar evolution in the US auto industry, perhaps starting as early as next year.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The beginnings of the change are already here. In Houston, Texas, trials are already underway by Domino’s Pizza, Kroger, and FedEx, using autonomous vehicles to deliver everything from prepared food to groceries to packages, while in California, 7-Eleven is running a similar test in Silicon Valley. If successful, these small-scale trials bring with them the promise of expansion, and a sea-change to logistics networks. Some estimates project the eventual potential impact of autonomous vehicles on the global economy at $7 trillion annually.

None of this would be possible, however, without a major change in the sensor systems that make self-driving cars possible. These systems, called LiDAR, as recently as 10 years ago could cost more than the entire rest of the car – but in recent years that cost has come down to less $1,000 per system, and that cost decrease has been accompanied by improvements in quality. The advent of affordable, higher-quality sensor systems, the ‘eyes’ of autonomous vehicles, marks the solution of a major challenge for the industry.

Against this backdrop, we’ve used the TipRanks platform to pull up the details on two stocks that are intimately connected with the autonomous car revolution. The pair have recently been given the thumbs up by certain Street analysts who project big gains ahead for both. So, let’s see how they are poised to benefit from this new paradigm.

Mobileye Global (MBLY)

First up is Mobileye, a company that got its start in advanced driver-assistance technology and has since leveraged that experience into autonomous vehicle sensor systems. The company’s driver assistance and safety systems are well-known – sensors that activate alarms if you drive too close to the vehicle in front, or start to drift out of your lane. More than 25 automakers have partnered with Mobileye to install these systems, and over 50 million units are on the road globally. The company is now working with 13 automakers to enable self-driving vehicle systems.

The company’s service options include a range of functionality between simple driver assistance and full autonomous driving. From cloud enhancement and front cameras, to 360-degree camera coverage to the addition of LiDAR sensors to turnkey solutions that will adapt self-driving cars to the needs of the user. The fully autonomous Mobileye Drive systems includes options for mobility-as-a-service, that will have clear applications in goods delivery, public transit, and robot taxis.

All of this, however, requires funding at a massive level – and to raise that capital, Mobileye has re-entered the public markets. The company was public until its 2017 acquisition by Intel; in October of this year, it spun off and held its second public stock offering. The event, which saw the MBLY ticker enter the markets on October 26, put 41 million shares on the market at $21 each, and included an underwriter’s option to buy over 6 million additional shares. When the offering closed, Mobileye had successfully raised approximately $990 million in gross proceeds.

Initiating coverage of this stock for Raymond James, 5-star analyst Brian Gesuale notes the company’s $40 billion total addressable market, and describes it as “the pioneer and undisputed market leader for computer vision/advanced driver assistance systems (ADAS) in the automotive industry.”

Looking ahead, Gesuale predicts solid performance, noting: “We are modeling revenue growth of 27% ($1.76B), 24% ($2.18B) and 33% (2.89B) from 2022 to 2024. We expect 2022 and 2023 to be the slowest growth periods for the next 5-years given supply chain impeding auto production and the mathematical impacts of a larger revenue base but ultimately see new, higher content/vehicle products driving a reacceleration. We are modeling EBITDA of $594M, $627M, and $959M over the same periods on margins in the low 30s%”

The analyst summed up, “The stock is poised to benefit from coming key product launches, increasing content per vehicle, margin improvement, and accelerated growth as autonomous driving becomes a reality.”

Along with these bullish comments, the analyst gives Mobileye’s new shares a Strong Buy rating, and a price target of $50 to suggest a robust gain of 84% in the next 12 months. (To watch Gesuale’s track record, click here)

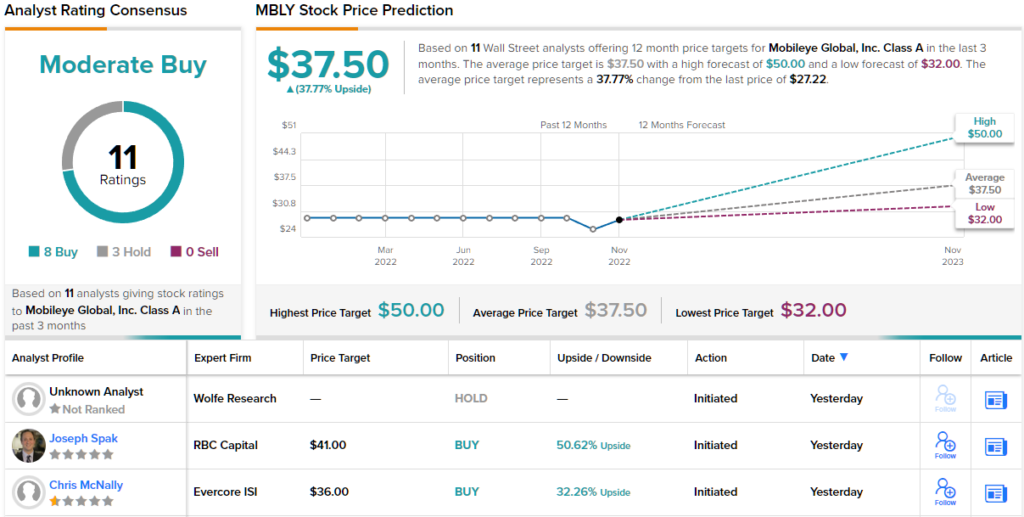

Overall, we’re looking here at a stock with a Moderate Buy consensus rating. MBLY has 11 analyst reviews on record, including 8 Buys and 3 Holds. The stock is currently selling for $27.22 and its $37.50 average price target indicates a potential one-year upside of 38%. (See MBLY stock forecast on TipRanks)

Luminar Technologies (LAZR)

Next up is Luminar, a Silicon Valley firm, based in Palo Alto, that designs and manufactures LiDAR systems. Luminar works at all stages of the development and manufacturing process, from the design of the semiconductor chips that are the ‘brains’ of the system, to the physical hardware of the electronics, transceivers, and receivers, that make the system work.

Luminar has been trading publicly for almost two years having IPOd via the SPAC route, and its shares in that time have fallen dramatically from the peaks hit in December 2020. The drop in share price has reflected the reality of a company that is not quite ready to switch to full production, as well as the regular quarterly net losses and SPACs falling badly out of favor. The most recent quarterly report, however, shows some reason for optimism.

In the 3Q22 financial release, revenue rose sharply, by 60% year-over-year, to $12.8 million. The Q3 revenue haul beat forecasts, and benefited from an acceleration of customer contracts; it also showed a 29% increase over the previous quarter. While the company delivered a non-GAAP net loss of $63.4 million, coming to 18 cents per share, the figure also trumped Street expectations. Also of interest to investors, Luminar finished Q3 with over $553 million in cash assets on hand – even after a quarterly cash burn of ~$52 million.

Most important, however, was the announcement that Luminar has finally entered regular production, with its introduction in SAIC’s R7 vehicle. SAIC is China’s largest automaker, and the R7 is the flagship of the firm’s Rising Auto brand. The introduction of Luminar’s sensor systems to the road with SAIC’s vehicle marks a major milestone for the LiDAR company, and its introduction to consumer vehicles.

Analyst Emmanuel Rosner, of Deutsche Bank, has been covering Luminar, and of the latest developments, he says, “The company is seemingly on track with building its new highly automated manufacturing facility, with 250k units of capacity coming online in 2H23, which we estimate could help Luminar reduce BoM towards the $500 level in 2024. All in, we believe Luminar continues to demonstrate solid traction in meeting or exceeding its near-term targets, and look forward to hearing more details about its pathway to profitability with existing capital… We continue to see LAZR as the best positioned LiDAR supplier to capture meaningful business wins for L3+ autonomy.”

Going forward, Rosner puts a Buy rating on LAZR shares, along with a $15 price target that implies a solid gain of 101% for the coming year. (To watch Rosner’s track record, click here)

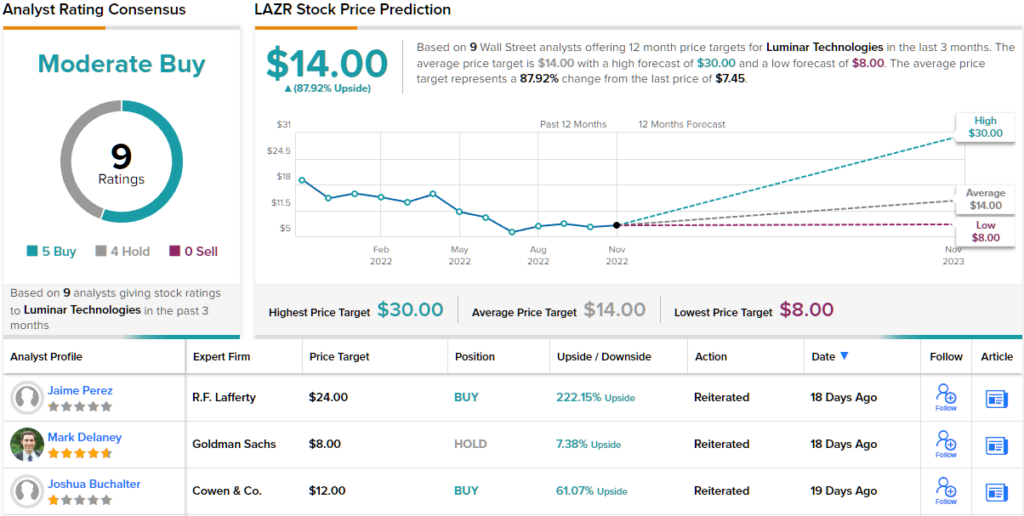

All in all, LAZR stock gets a Moderate Buy rating from the analyst consensus. This rating is based on 9 recent reviews from the Street, breaking down to 5 Buys and 4 Holds. With an average price target of $14 and a current trading price of $7.45, Luminar’s shares show a one-year potential upside of 88%. (See LAZR stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.