In recent years, an interlocked combination of social pressures and government incentives has provided strong support for ‘green’ initiatives, from biodiesels to solar power. The solar power industry, in particular, deserves our attention as it has produced numerous technology and installation companies dedicated to building solar systems for residential and commercial building use.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

The solar sector has faced a medley of headwinds and tailwinds in recent years, exerting conflicting pressures on companies within it. From the robust Federal incentives outlined in the Inflation Reduction Act to the adverse effects of elevated inflation and interest rates, uncertainty looms over the industry’s trajectory.

Nevertheless, according to RBC Capital analyst Chris Dendrinos, there is an optimistic outlook for solar stocks. He writes, “We believe the solar industry should continue to benefit from a positive rate of change and will continue to see long-term support from public policy, emissions regulation, and declining costs. Near term, both residential and utility scale solar are facing headwinds. Residential solar faces challenges from a higher interest rate environment, unfavorable changes in net metering policy, and the roll-off of certain subsidy programs in international markets. However, we see a potential turning point in investor sentiment, as the bottom of the demand slowdown is being set and expectations for declining interest rates support improving payback periods.”

To this end, Dendrinos has picked out 2 solar stocks he thinks are worth buying right now, and it seems like others in the market agree, judging by the positive outlook from analysts tracked by TipRanks. Let’s give them a closer look.

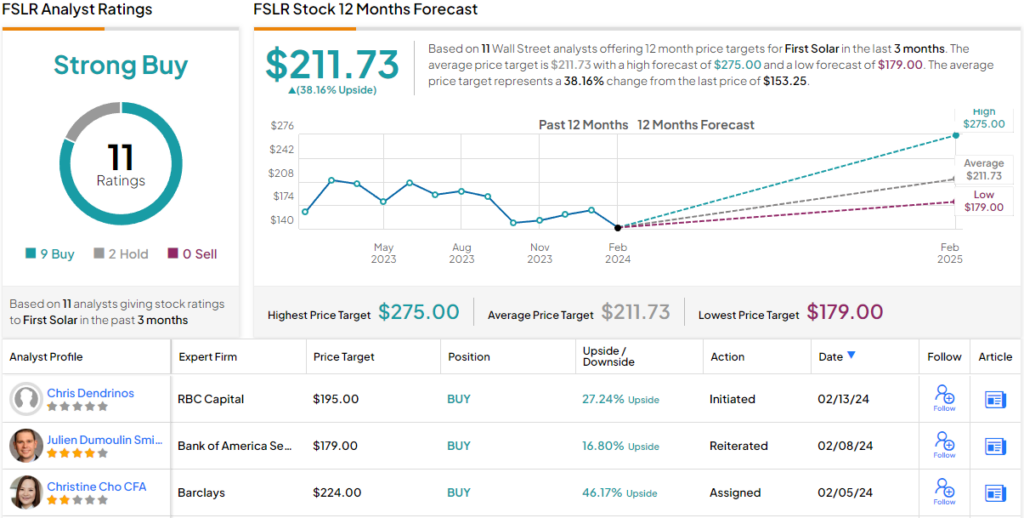

First Solar (FSLR)

The first of RBC’s ‘green shoots’ that we’ll look at is First Solar, the leading company in the US solar power industry and one that has been in business since 1999. First Solar produces photovoltaic panels, the emblematic item in any solar installation; these are the panels that actually capture sunlight and convert it to electrical energy. The company is the leading US producer of such panels and has a strong presence in the global solar market.

Earlier this year, First Solar announced the opening of two new manufacturing facilities. The first announcement concerned a new facility in Tamil Nadu, India. The plant is a vertically integrated solar panel factory, the first of its type in that country, and has an annual nameplate capacity of 3.3 gigawatts. The plant, which employs approximately 1,000 people, produces the Series 7 photovoltaic panel, a device developed in the US and optimized for the Indian solar market.

The second new manufacturing announcement concerned the acquisition of a 1.2 million square foot facility in Troy Township, Ohio. The site, which was formerly the Peloton Output Park, will be transformed into a First Solar distribution center to support the company’s Ohio manufacturing footprint. As of the end of 2023, First Solar had 6 gigawatts of solar panel manufacturing capacity in Ohio. The company plans to expand its US manufacturing output to 14 gigawatts by 2026. As part of this expansion, the company is investing up to $370 million in an R&D innovation center, to be located in Perrysburg, Ohio, and slated for completion this year.

First Solar will release its financial results for Q4 and the full year 2023 on February 27; we can look back at the Q3 numbers to see where the company is coming from going into the 2023 earnings print.

In Q3, First Solar reported top-line net sales of $801 million, up 27% year-over-year. The revenue total missed the forecast by $91.25 million. First Solar’s bottom line, the EPS figure of $2.50, was 46 cents per share better than had been expected. First Solar turned from a net loss to a net profit in 1Q23, and earnings have been rising since.

For RBC’s Dendrinos, this stock deserves an upbeat outlook based on the company’s solid market position and its commitment to expanded manufacturing and R&D. The analyst writes, “First Solar has established a dominant position in the utility scale solar market in the U.S. We believe there is an opportunity to continue to grow the domestic market share and expand internationally. Longer term, the competitive position will likely depend on the ability to improve the technology and compete against low cost foreign producers. We believe IRA tax credits are a key enabler to accelerating the technology road map. FLSR [sic] is investing $370mm in a R&D center and has committed to accelerating R&D spend the next few years.”

Quantifying his stance on FSLR, Dendrinos puts an Outperform (Buy) rating on the stock, with a $195 price target to suggest a near-27% upside for the coming 12 months. (To watch Dendrinos’ track record, click here)

Overall, there are 11 recent analyst reviews on FSLR shares, and these include 9 Buys and 2 Holds for a Strong Buy consensus rating. The stock’s $211.73 average price target is even more bullish than the RBC view, and implies a 38% gain from the current trading price of $153.25. (See FSLR stock forecast)

Shoals Technologies (SHLS)

Next up, Shoals Technologies works with EBOS, electrical balance of systems, providing the needed know-how and hardware to support solar and energy storage installations. EBOS is the essential link in the alt-energy industry, providing the connections between solar power generation, storage batteries, and the power grids where users tap into the electricity.

Specifically, Shoals’ product lines include a wide range of cable assemblies, combiner boxes, in-line fuses, junction boxes, PV wire, racking, recombiners, splice boxes, and wireless monitoring systems – all of these and more are considered ‘mission-critical’ in the solar power industry, and carry a high consequence for failure. Shoals has leveraged this fact to support premium pricing, noting that customers will ‘prioritize reliability and safety over price when selecting EBOS solutions.’

Shoals has been in the EBOS business for 27 years, and in that time has accumulated 35 patents to protect its intellectual property. The company boasts that it is the world’s largest supplier of EBOS equipment and currently has more than 62 gigawatts under contract, in construction, or in operation. The company can optimize its products and installations for solar-plus-storage projects or for standalone energy storage.

In its last earnings release, from 3Q 23, Shoals reported revenues of $134.2 million, up almost 48% year-over-year – although also down $1.23 million compared to the forecast. The company’s earnings, reported as the non-GAAP earnings-per-share of 20 cents, were 5 cents better than had been expected. The company has predicted full-year 2023 total revenues in the range of $485 million to $495 million. We’ll see on February 28, when Shoals releases results for 4Q and full-year 2023, how the company measures up to its guidance.

Checking in again with analyst Chris Dendrinos, we find him upbeat on Shoals’ built-in advantages in labor costs and margins. He says of the company, outlining these points, “Industry labor costs nearly doubled y/y as a result of the IRA’s implementation of new prevailing wage requirements tied to a 30% tax credit, and now account for ~20% of total utility scale solar system costs. Shoals’ products are not only engineered to reduce the need for skilled labor but to reduce the need for labor altogether. We believe the IRA wage requirements could drive additional demand for Shoals’ products as project developers look to minimize labor.”

“Shoals’ gross margins are ~10-20% above peers in the solar tracker and electrical connector & sensor segments.” Dendrinos wraps up by saying, “We attribute the leading gross margin profile to the high value add of the company’s products and a sales and distribution model that is primarily direct to consumer (EPC).”

These comments back up Dendrinos’ Outperform (i.e. Buy) rating on the stock, while his price target of $20 indicates a ~25% potential upside in the coming year. (To watch Dendrinos’ track record, click here)

All in all, the 7 recent analyst reviews on SHLS stock break down 5 to 2 favoring Buy over Hold, for a Moderate Buy consensus rating. The stock is selling for $15.94 and its $19.86 average price target suggests ~25% increase in the next 12 months. (See Shoals stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.