Investors like getting a return on investment, of course, it’s why they are in the market to begin with. And when a company makes a commitment to return capital and profits to the shareholders, that’s a win – one that will both attract and reward investors. The key for investors is to find the best possible capital return, and dividend stocks make a logical place to start looking.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

With this in mind, we’ve used the TipRanks database to pull up the details on two true dividend aristocrats – real champions of capital returns for investors to consider. These stocks feature Strong Buy ratings from the Street’s analysts, reliable dividend payments over a decade or more, and they still have a double-digit share price upside in the near term. Here’s a closer look.

Exxon Mobil (XOM)

The first dividend aristocrat we’re looking at is Exxon Mobil, one of the major oil and energy firms operating in the global markets. The company operates on every continent except Antarctica, and has extensive production ops in both crude oil and natural gas. Its US activities include extensive refining operations, while the company has major oil and natural gas extraction plays offshore of Guyana in South America, in Indonesia, and in Papua New Guinea. Exxon Mobil boasts a market cap near $370 billion, and where the broader markets are down this year, XOM shares have gained 53%.

A look at Exxon Mobil’s recent 2Q22 earnings shows that the company operates on a sound footing. Top line revenues came in at $115.7 billion, and supported $20 billion in cash flow from operations and $17.9 billion in net earnings. Per share, earnings were reported at $4.14, a significant increase from the year-ago quarter’s $1.10 EPS.

This solid performance backs up a solid dividend. XOM paid out 88 cents per common share in Q2, and the Q3 payment has been declared at the same level for next month’s distribution. At this level, the dividend annualizes to $3.52 per share and gives a yield of ~4%. Exxon Mobil has kept up a reliable dividend payment for the past decades.

Checking in with the Street’s analysts, we find that Credit Suisse’s Manav Gupta rates XOM shares an Outperform (i.e. Buy), and sets a $125 price target to suggest a one-year upside of ~37%. (To watch Gupta’s track record, click here)

Backing this stance, Gupta writes: “We have XOM generating ~$37.8Bn in post dividend FCF in 2022, which will be used to support higher shareholder returns (~$15Bn buyback) and build cash on the balance sheet. Post Russia-Ukraine conflict, world is short crude, refined products and natural gas, XOM’s differentiated growth strategy will deliver excellent return on capital employed.”

Overall, this oil major has picked up reviews from 13 Wall Street analysts in recent weeks, and these include 10 to Buy and 3 to Hold, for a Strong Buy analyst consensus rating. XOM shares are priced at $91.45 and have an average price target of $110.13, indicating room for ~20% share growth in the year ahead. (See XOM stock forecast on TipRanks)

Linde plc (LIN)

From oil and natural gas, let’s switch over to industrial gasses. Linde is the world’s largest provider in this niche, and manufactures a wide range of gasses for industrial use. The company’s products include such common materials as argon, nitrogen, and oxygen, as well as more volatile gasses like hydrogen and acetylene. Linde can provide gasses in a wide range of forms, from normal atmospheric pressure or higher pressure liquefied forms. The company also provides engineering services for gas processing, separation, and liquefaction. Linde’s gas products are found in applications as varied as welding, laser technology, and medicine. The company reported $31 billion in total sales last year.

Turning to corporate performance, we find that Linde’s 2Q22 top revenues came in at $8.5 billion, a gain of 12% year-over-year. For the first half of 2022, the company has brought in $16.7 billion, more than half the total from 2021 – which bodes well for the full-year totals. Linde saw an operating cash flow for the quarter of $2.1 billion, an increase of 17% y/y, and adjusted earnings of $3.10 per share. EPS was up 15% from the year-ago quarter.

Looking forward, Linde bumped up its full-year earnings guidance significantly, to the $11.73 to $11.93 range. Achieving this will mark growth of 10% to 12% year-over-year.

So Linde runs a profitable business – and it passes the profits on to investors. The company’s dividend, recently declared for Q3 and scheduled for payment in mid-September, is currently $1.17 per common share, or $4.68 annualized. At that rate, the dividend yields a 1.5%, but the real attraction here is the reliability; Linde has been keeping up its dividend payments, and gradually increasing them, for the past 30 years.

Looking at Linde’s second quarterly results, Morgan Stanley’s Vincent Andrews is impressed with the company’s execution in recent months, writing: “Linde’s pattern of beating its conservative guidance continued in 2Q22 despite the continued run up in European natural gas prices and adverse FX movement, which were clearly a headwind, though the company beat both MSe and consensus easily in the EMEA segment.”

“The company beat both Morgan Stanley and consensus in all segments but Americas and investors are likely to key off of the continued ex-passthrough margin expansion in APAC and EMEA, in line with our view that Linde continues to have a significant self-help opportunity in those segments that is particularly advantageous in the current environment of energy cost inflation,” the analyst added.

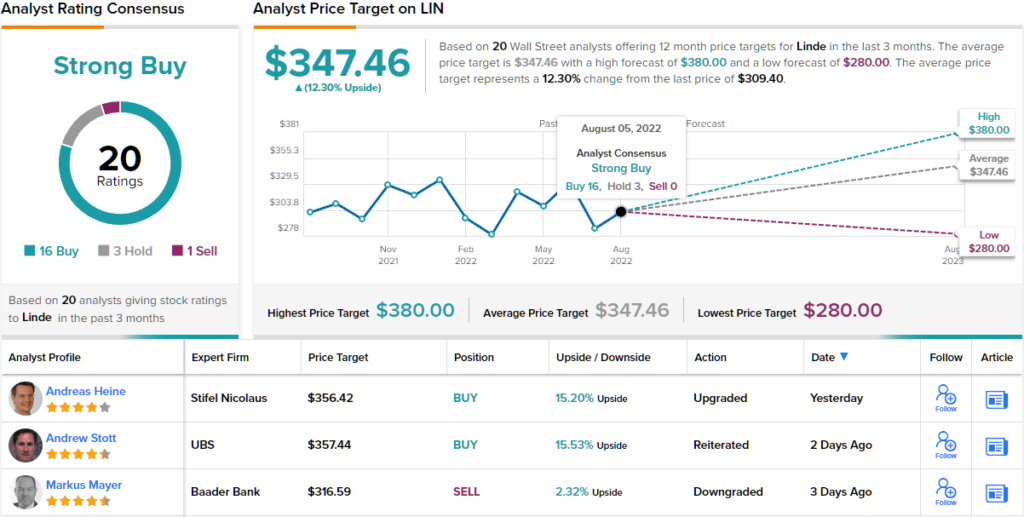

In line with his comments, Andrews rates LIN shares an Overweight (i.e. Buy), and sets a $365 price target, implying an upside potential of 18% for the next 12 months. (To watch Andrews’ track record, click here)

While Linde is hardly a household name, the company is an essential link in multiple industries, and as such, it has attracted plenty of attention from Wall Street. LIN shares have received 20 recent analyst reviews, a total that includes 16 Buys, 3 Holds, and a single Sell, for a Strong Buy consensus rating. Overall, the stock has ~12% one-year upside, based on a trading price of $309.40 and an average price target of $347.46. (See LIN stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.