As Lockheed Martin (NYSE:LMT) inks a host of big-money deals, value hunters should consider the stock an absolute steal. Yet, it takes courage to buy when others are selling. I invite you to flex your contrarian muscles today, as I am bullish on LMT stock as a long-term holding.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Lockheed Martin is one of the biggest and best-known aerospace and defense contractors in the U.S. The company has earned the trust of the American government and is able to generate revenue and profits regardless of whether the nation is at war or not. Check Lockheed Martin’s earnings track record, and you’ll find that the company usually beats Wall Street’s quarterly EPS estimates and is profitable.

Lockheed Martin is often considered a safe company to invest in, but lately, the market has turned against it. I’m thanking my lucky stars for this, as opportunities arise when short-term traders don’t see the true value of a solid business like Lockheed Martin.

Lockheed Martin is Still a Go-To Military Equipment Supplier

Regardless of the ups and downs of LMT stock, Lockheed Martin remains a favorite equipment supplier for military entities. Check TipRanks’ news page for the company, and you’ll see exactly what I’m talking about, as Lockheed Martin has scored one lucrative military deal after another.

Starting outside of the U.S., we can observe that Lockheed Martin announced a $6.5 billion deal to provide 32 F-35 fighter planes for Romania. Furthermore, Lockheed Martin just celebrated the delivery of F-35A Lightning II aircraft to the Royal Danish Air Force.

Let’s be honest, though. Lockheed Martin’s bread and butter is the company’s deals with the U.S. military. It’s hard to even keep track of Lockheed Martin’s recent deals and/or deal expansions with the American Armed Forces.

For instance, Lockheed Martin’s subsidiary Sikorsky secured a $12 million contract to provide spare parts for the CH-53K helicopter. Additionally, LMT struck a $175.9 million deal to procure and service the F-35 Lightning II fighter aircraft.

Meanwhile, RTX Corporation’s (NYSE:RTX) Pratt & Whitney business unit has clinched two significant contracts related to F135 propulsion systems for the F-35 Lightning II fighter aircraft: a $305.6 million deal to provide and service these systems and a $163.3 million modification contract to procure spare engines, power modules, special test equipment, and special tooling. Since Lockheed Martin is the primary manufacturer of the F-35 Lightning II aircraft, LMT benefits from these RTX contracts.

There’s also a $22.3 million Army contract to deliver an air-to-ground missile system and a $50 million Air Force agreement to provide and service U-2 Dragon Lady planes (one of which recently completed a successful first flight). I think you get the idea by now. No matter how you slice it, Lockheed Martin has boatloads of cash coming in from the company’s many deals with public entities in the U.S. and abroad.

Lockheed Martin Looks Terrific at Its Current Price

Both value investors and income seekers really ought to take a look at LMT stock. Lockheed Martin’s GAAP-measured trailing 12-month P/E ratio of 14.9x compares favorably to the sector median P/E ratio of 18.86x. Moreover, Lockheed Martin pays an annual dividend yield of 2.93% versus the sector average dividend yield of 1.639%.

Given everything I’ve just told you, it’s baffling that Lockheed Martin shares are so far down from their April peak price of around $500. There’s nothing negative that I could find on TipRanks’ Lockheed Martin news page. What’s going on, then?

I suspect that the market is generally rotating out of defensive names and dividend stocks. After all, if you can get a near-5% yield from 10-year Treasury bonds and it’s risk-free, some financial traders might view this as the best defensive play in 2023.

I can’t find any other reason why short-term traders would choose to punish Lockheed Martin now. In their quest for yield, they’re not considering the true, long-term value proposition that a stalwart aerospace and defense giant like Lockheed Martin can provide.

Is LMT Stock a Buy, According to Analysts?

On TipRanks, LMT comes in as a Hold based on two Buys, 10 Holds, and one Sell rating assigned by analysts in the past three months. The average Lockheed Martin stock price target is $497.27, implying 23.1% upside potential.

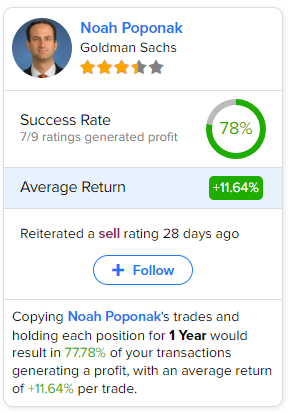

If you’re wondering which analyst you should follow if you want to buy and sell LMT stock, the most accurate analyst covering the stock (on a one-year timeframe) is Noah Poponak of Goldman Sachs, with an average return of 11.64% per rating and a 78% success rate. Click on the image below to learn more.

Conclusion: Should You Consider LMT Stock?

In case I didn’t drive this point home enough already, Lockheed Martin has a large number of agreements with military entities. These multi-million and multi-billion-dollar contracts will provide ongoing revenue to Lockheed Martin in the coming quarters.

Nonetheless, the market doesn’t favor Lockheed Martin right now, and I’m perfectly fine with that. Now is the time to seriously consider a position in LMT stock and give short-term traders time to rotate back into sensible, dividend-paying defensive names like Lockheed Martin.