November 1, 2023, could go down as a historic day for Microsoft (NASDAQ: MSFT). That is because it is the day when the Copilot AI assistant tool became generally available in Microsoft 365.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

It’s an event that cements Microsoft’s position as the leader in AI, where, given the enormous success of OpenAI’s ChatGPT (whom Microsoft is heavily invested in), it already has something of a head start on its competitors. The fact that Microsoft is actually leading the way here should not be taken for granted, says Stifel analyst Brad Reback.

“We highlight this is the first time in over 2 decades the company is not playing from behind in an emerging tech trend,” the 5-star analyst said. “Given how well MSFT has been able to close the gap in Cloud over the last decade, we eagerly await what we believe will be a very strong mix of AI-driven pricing and volume gains that should begin to become increasingly evident in coming quarters. The net result is we expect the coming AI cycle to allow Microsoft to sustain double-digit revenue and profitability growth for years to come.”

Following a highly successful paid preview program, Reback anticipates that organizations, regardless of their size, will soon start implementing the solution for their end-users. While large enterprises usually adopt new applications at a deliberate pace, Reback reckons a quicker adoption rate for the Copilot framework compared to historical rates. This is due to the significant operational advantages that customers can derive from it.

Management has emphasized that the anticipated efficiency improvements played a central role in determining the pricing of the product, which is set at an additional $30 per user per month at the list price.

“That said,” adds Reback, “given what is likely to be some level of early experimentation, phased roll-out among customers, and focused education/learnings by customers on how to best leverage the products, we expect the revenue contribution to continue to build over many quarters to come.”

And it’s the renewed focus on revenue growth ahead that is enticing. After dedicating a significant portion of the past year to aligning its operating expenses with the current economic conditions (resulting in a 7% year-over-year reduction in headcount in 1QFY24 and only a 1% increase in operating expenses), and also achieving cost-of-goods-sold (COGS) improvements through ongoing efficiency enhancements in its different Cloud assets, it is evident that management has now “shifted its attention back to top-line growth.”

So, down to business, what does it all mean for investors? Reback reiterated a Buy rating on MSFT shares, backed by a $390 price target. There’s potential upside of 10.5% from current levels. (To watch Reback’s track record, click here)

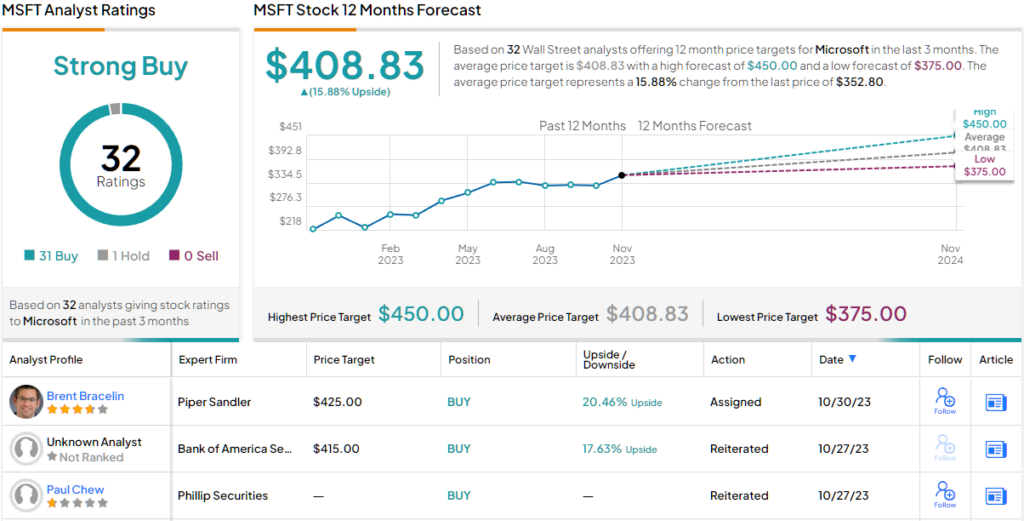

Support for Microsoft on Wall Street is almost unanimous. Barring one skeptic, all 31 other recent analyst reviews are positive, making the consensus view here a Strong Buy. At $408.83, the average target suggests shares will gain ~16% over the one-year timeframe. (See Microsoft stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.