The latest data shows inflation is clearly on the backfoot. The June report showed inflation fell for the twelfth month in a row, dropping to 3% year-over-year, in what amounts to the most prolonged period of pullbacks since the early 1980s.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

The core measure, which takes out food and energy prices, dropped to 4.8% – the slowest rate seen since November 2021. According to Raymond James CIO Larry Adam, an even more noteworthy aspect is that the core measure is now below the current fed funds rate, a situation that has only occurred 20% of the time in the past two decades.

What all of this means, according to Adam, is that following 500 bps rate hikes made over the last 16 months to curb runaway inflation, there is a growing belief that the Fed will not proceed with the two additional bps rate hikes initially planned for 2023. Instead, it is now expected that the Fed will proceed with only one more rate hike.

“The Fed is executing its playbook according to plan – get interest rates up quickly, keep tightening albeit at a more moderate pace and then hold rates steady to allow real rates to nudge higher as inflation recedes. While stronger than expected economic data in the first half of the year has kept the Fed in play, as the pace of job growth and inflation slow, the Fed should be able to raise rates one more time (at the July FOMC meeting) and then hold rates steady for an extended period of time,” Adam explained.

So, good news for investors who have longed for a pause to the rate hikes. Meanwhile, against this backdrop, the analysts at Raymond James have been pointing out stocks that look ripe for loading up in this environment and have tagged two names as ‘Strong Buys.’ According to the TipRanks database, both of these stocks are also rated as ‘Strong Buys’ by the analyst consensus. Let’s see why they are drawing plaudits across the board.

Tidewater Inc. (TDW)

We’ll start with Tidewater, an American offshore energy service company that specializes in providing marine support services to the global oil and gas industry. The firm is a leader in the Offshore Support Vessel (OSV) segment and with a history dating back to 1956, is actually considered the industry’s first OSV firm.

With a large modern fleet of offshore service vessels and a significant presence in various regions, the company’s ability to offer a comprehensive range of services, including platform supply vessels, anchor handling tug supply vessels, and offshore tugs, has enabled it to remain a major force in the market.

In fact, during Q1, given the offshore market’s recovery and recent times’ high day rates, the company generated its best quarterly revenue and adjusted EBITDA since 2015. Revenue climbed by 83% compared to the same period last year to $193.1 million, while adjusted EBITDA reached $59.1 million, the best quarterly EBITDA haul since 3Q15. These results made use of the highest quarterly global average day rate since that period and the good news is that over the next year, the rates are expected to stay high.

The rising rate environment is a point picked up by Raymond James analyst James Rollyson when laying out the bull case for Tidewater. He writes, “As the leader in the global OSV market, the company clearly has significant financial benefits to rising dayrates. The 1Q23 annualized EBITDA (including the Solstad vessels – the company recently closed the purchase of 37 vessels from Solstad) of ~$332 million would rise to more than $600 million at a $20,000 fleet average dayrates (1Q23 average bookings were ~$21,000), and more than $1.3 billion at a $30,000 fleet average, which is closer to where newbuilds would be viable. That is meaningfully higher than what is currently factored into TDW’s share price.”

“The potential improvements in TDW’s earnings and cash flows in a rising dayrate environment suggest a period of strong free cash flows, ROCE, and a materially higher share price, despite the rise that has taken place over the past 12 months,” Rollyson summed up.

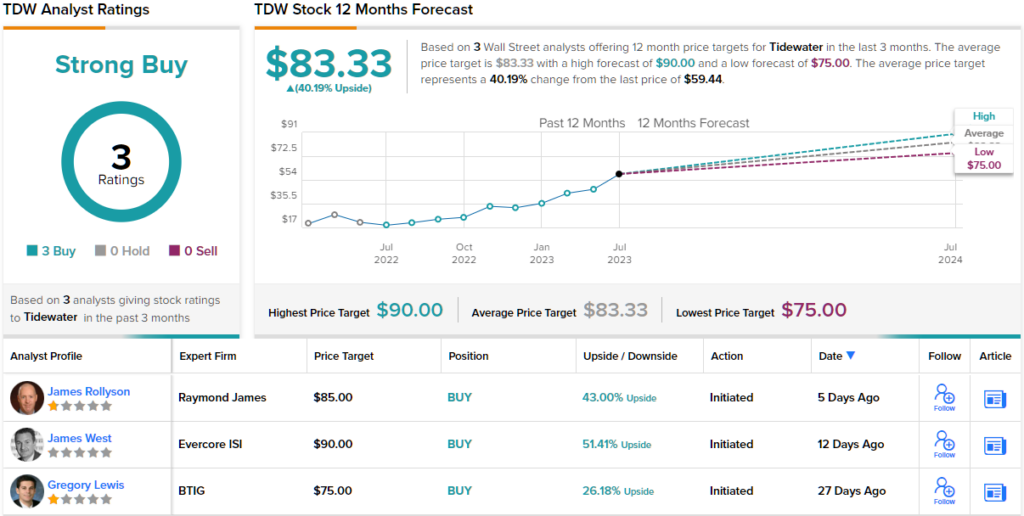

These comments underpin Rollyson’s Strong Buy rating on TDW, and his $85 price target suggests the shares will climb 43% higher over the coming months. (To watch Rollyson’s track record, click here)

What does the rest of the Street think? With 3 ‘Buys’ and no ‘Holds’ or ‘Sells,’ the verdict is that TWD is a ‘Strong Buy.’ Additionally, the $83.33 average price target indicates an upside potential of 40%. (See TWD stock forecast)

Integral Ad Science (IAS)

For our next RJ-backed stock, we’ll turn to a completely different industry. Integral Ad Science is a global tech company that specializes in digital ad verification and optimization solutions. That is, it essentially analyzes for companies the value of digital advertising placements.

Since founding in 2009, IAS has established itself as a partner for advertisers, agencies, and publishers seeking to ensure the quality and effectiveness of their digital advertising campaigns. The company’s advanced suite of products makes use of cutting-edge machine learning and data science capabilities to assess the viewability, brand safety, ad fraud, and overall media quality across various digital platforms. By providing real-time insights and actionable data, clients can make informed decisions that maximize the impact of their ad spend, enhance the brand’s reputation, and create a safer, more transparent digital advertising ecosystem.

It’s a value proposition that served the company well in its most recent quarterly readout, for 1Q23. Revenue hit $106.1 million, amounting to a 19% year-over-year increase, whilst beating the Street’s forecast by $3.14 million. EPS came in at $0.02, $0.01 ahead of expectations. Looking ahead, for Q2, the company sees revenue hitting the range between $111 million and $113 million, above consensus at $111.68 million at the midpoint.

That performance has helped the shares completely outpace the market in 2023, with the stock up by 125% year-to-date. However, there are further gains coming, believes Raymond James analyst Andrew Marok, who sees the company’s “multi-faceted growth outlook addressing large and growing TAMs.”

“In addition to the company’s established core business in Optimization and Social, the growth strategy is formed of multiple legs including CTV, International, Mid Market, Social Live Feeds, Retail Media, and Emerging Channels,” Marok explained. “While these various opportunities will be attacked over varying time frames (some long-term in nature), they should all help IAS further penetrate the company’s TAM – digital advertising ex-Search, which we estimate at ~$270B of spend in FY23E.”

To this end, Marok rates the stock a Strong Buy, backed by a $23 price target. The implication for investors? Further upside of 16% from current levels. (To watch Marok’s track record, click here)

Elsewhere on the Street, the stock garners an additional 7 Buys and 2 Holds, all culminating in a Strong Buy consensus rating. Going by the $22.19 average target, the shares will appreciate by ~12% in the months ahead. (See IAS stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.