Everyone invests with the goal of generating big returns but it’s easy to get distracted by all the short-term noise generated on Wall Street. The key to investing success, according to Raymond James CIO Larry Adam, is to follow a few simple rules.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

One is to realize past performance does not necessarily guarantee future success. “History has shown that no single asset class has been a consistent winner year after year,” says Adam, “just as no single asset class remains at the bottom.”

Secondly, it’s important to make portfolio adjustments as necessary and strike a healthy balance between offense and defense.

Last but not least, it’s imperative to focus on the long-term. “Having the fortitude to look through market volatility, stick to your well thought out financial plan and to stay invested for the long term remains critical to achieving investment success,” Adam explains.

Meanwhile, putting all this invaluable advice into action, Adam’s analyst colleagues at Raymond James have pinpointed an opportunity in 2 stocks they consider right now as Strong Buys. We ran these tickers through the TipRanks database to see whether other market experts agree with these choices. Let’s check the results.

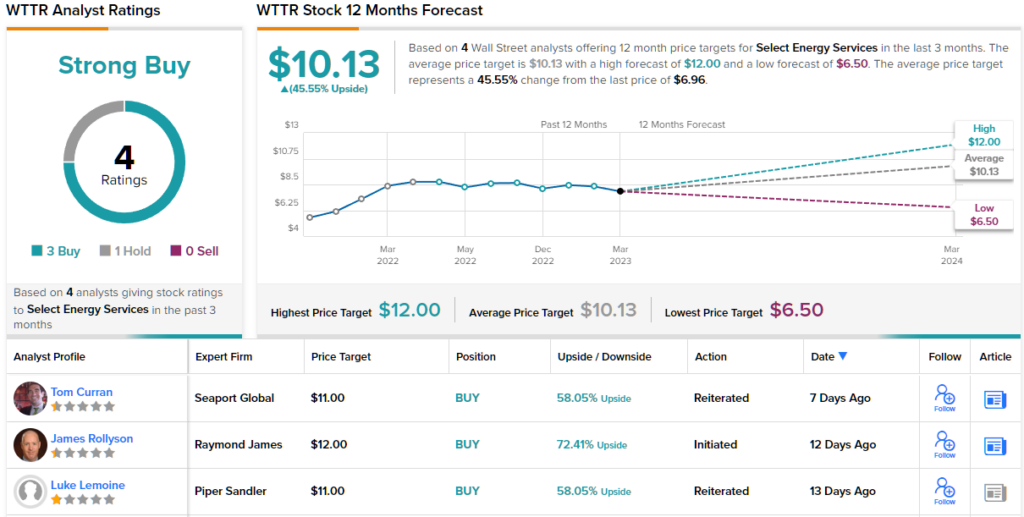

Select Energy Services (WTTR)

We’ll begin with Select Energy Services, a company that provides the oilfield industry with water management solutions. This involves the procurement, distribution, recycling, and disposal of water. The company offers a full range of oilfield chemicals in addition to flowback and well testing services, lodging, and rentals. Select Energy has over 1,500 miles of underground pipeline, almost 3.0 MMBpd of water recycling capacity (with corresponding storage), almost 2.7 MMBpd of disposal capacity, and other ancillary equipment/facilities to serve its different segments. The bulk of the company’s revenue is generated in the Permian, although it also boasts operations in South Texas, the Rockies, and other regions.

While Select Energy posted some robust growth in its most recent quarterly update, it missed both top-and bottom-line expectations. In Q4, revenue grew by 49.6% year-over-year to $381.68 million, yet fell short of the forecasts by $6.21 million. Gross profit reached $41.6 million vs. the $17.9 million generated in the same period a year ago, although at $0.07, EPS missed the $0.23 consensus estimate.

Meanwhile, Select Energy has been extremely busy on the M&A front and during December 2022 and January 2023, concluded a succession of transactions in the Midland Basin region of the Permian Basin for a total of ~$44 million. That followed the November 2022 completion of the acquisition of Breakwater Energy Partners, and the acquisition from Cypress Environmental Services of a portfolio of water gathering pipeline and disposal assets in the Bakken Shale.

Looking ahead, Raymond James analyst James Rollyson sees plenty to be buoyed about.

“The company’s strong position as a leader in water sourcing, transfer, disposal, and especially recycling positions it well under the growing water needs of the oil patch,” Rollyson explained. “Select’s focus on the management of water and water logistics in the energy industry, including being the leader in water recycling that is also tied to a sustainability-linked credit facility demonstrate the company’s commitment to meeting ESG goals.”

In the eyes of Rollyson, the current share price is an opportunity for investors. He writes, “Select is trading at a pretty meaningful discount to all its peers despite having the best balance sheet and highest EBITDA growth rate of the group. As a result, we think shares of WTTR are attractively valued at current levels.”

Accordingly, Rollyson gives WTTR shares a Strong Buy rating, while his $12 price target suggests investors could be pocketing returns of 72% a year from now. (To watch Rollyson’s track record, click here)

Overall, WTTR gets a Strong Buy rating from the Wall Street consensus, too, based on 4 analyst reviews, comprising of 3 Buys and 1 Hold. With the shares currently trading at $6.96, the average price target of $10.13 suggests a potential upside of ~46%. (See WTTR stock forecast)

Ciena Corporation (CIEN)

The second pick from Raymond James brings us to Ciena, a top-tier supplier of networking systems, services, and software, specializing in optical transport and switching systems. With over 2,000 patents to its name, the company offers these solutions to more than 1,600 global customers. Moreover, Ciena stands out in the industry with its first coherent optical solution.

It’s a business proposition that served the company well in its most recent quarterly readout, for the fiscal first quarter of 2023 (January quarter). Revenue climbed by 25.5% year-over-year to $1.06 billion, coming in ahead of expectations by $100.96 million. Adjusted net income reached $95.6 million, which compared well to the $72.6 million generated in the same period a year ago. That led to adj. EPS of $0.64, improving both on last year’s $0.47 and the $0.36 anticipated on Wall Street.

But for Raymond James analyst Simon Leopold, it’s the prospect of a new market opening up for Ciena that fuels the bull-case. According to industry checks, Ciena is about to enter the edge router market, with its own platform called WaveRouter, and this offers a catalyst ahead.

“We consider WaveRouter Ciena’s counter-punch to routers absorbing elements of the optical transport market. We believe the platform allows Ciena to address SP edge router use-cases and will feature subscriber management features for enterprise, consumer and mobile network support. The platform converges optical and routing capabilities. Dell’Oro forecasts the SP Edge Router market reaches $8B in 2023 and grows with a 2% CAGR 2022-2027. Ciena has no share, so routing is all upside. We expect Verizon will be among the early adopters deploying the platform in a portion of the network currently served by Ciena’s 6500,” Leopold opined.

To this end, Leopold upgraded CIEN’s rating from Outperform to Strong Buy and increased the price target from $58 to $70. The implication for investors? 33% upside potential from current levels. (To watch Leopold’s track record, click here)

Overall, CIEN shares have a Strong Buy rating from the analyst consensus, as well, showing that Wall Street agrees with Leopold’s assessment. The rating is based on 9 Buys and 2 Holds set in the past 3 months. Shares are selling for $52.52, and the average price target, at $66, implies ~27% upside potential. (See CIEN stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.